INCOME TAX APPELLATE TRIBUNAL (CHENNAI BENCH)

ABY T VARKEY, Judicial Member, S. R. RAGHUNATHA, Accountant Member

Valar and Co. – Appellant

Versus

Income Tax Officer – Respondent

| Table of Content |

|---|

| 1. facts: assessment set aside; penalties initiated in original order. (Para 2 , 3 , 4 , 5) |

| 2. arguments: assessee claims penalties invalid sans fresh satisfaction. (Para 6 , 7 , 8) |

| 3. set-aside obliterates prior satisfaction; fresh order governs. (Para 9) |

| 4. supreme court precedents apply to s.271da/271e. (Para 10) |

| 5. appeals allowed; penalties deleted. (Para 11) |

आदेश /ORDER

PER S.R.RAGHUNATHA, AM:

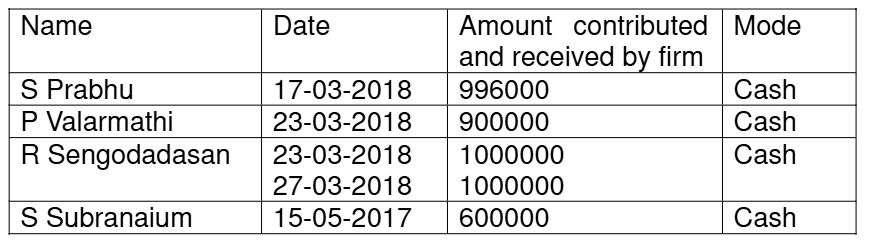

These appeals by the assessee are filed against the separate orders of the learned Commissioner of Income Tax (Appeals), National Faceless Appeal Centre (NFAC), Delhi,(in short “ld.CIT(A)) for the assessment year 2018-19, both dated 24.09.2025 against the penalty orders of the NaFAC, Delhi u/s.271DA and 271E of the Act dated 23.02.2022 and 10.01.2022 respectively. Both these appeals were heard together and disposed of by this consolidated order for the sake of convenience.

2. The legal issue raised by the assessee in both the appeals is that

"Whether the Impugned Penalty Orders u/s.271DA and 271E of the Act survive in the eyes of law, when the underlying Assessment Order in which the satisfaction was recorded was set aside for de novo adjudication and when no such satisfaction wa

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :