INCOME TAX APPELLATE TRIBUNAL (BANGALORE BENCH)

Prashant Maharishi, Vice-President, Keshav Dubey, Judicial Member

Surekha – Appellant

Versus

ITO – Respondent

| Table of Content |

|---|

| 1. admission of additional legal grounds permissible (Para 1 , 2 , 3) |

| 2. agriculture income addition partially confirmed (Para 4 , 5 , 6) |

| 3. parties contend assessment validity post-death (Para 7 , 8) |

| 4. section 159(2)(b) mandates notice to legal heirs (Para 9) |

| 5. appeal allowed; assessment quashed (Para 10) |

ORDER

PER KESHAV DUBEY, JUDICIAL MEMBER:

This appeal at the instance of the assessee is directed against the order of ld. CIT(A)/NFAC dated 4.9.2025 vide DIN & Order No. ITBA/NFAC/S/250/2025-26/1080362875(1) passed u/s 250 of the Income Tax Act, 1961 (in short “The Act”) for the assessment year 2018-19.

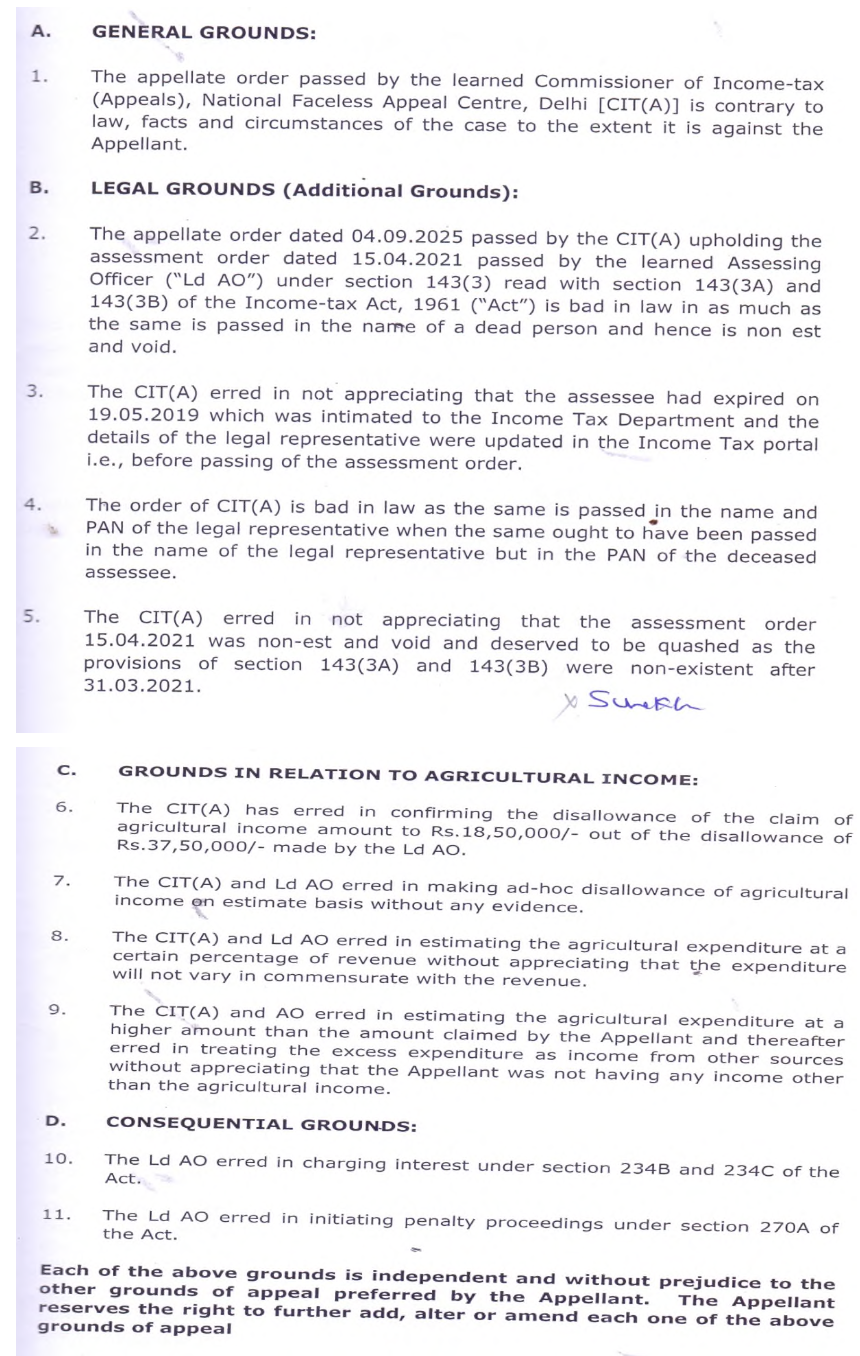

2. The assessee has raised the following grounds of appeal:

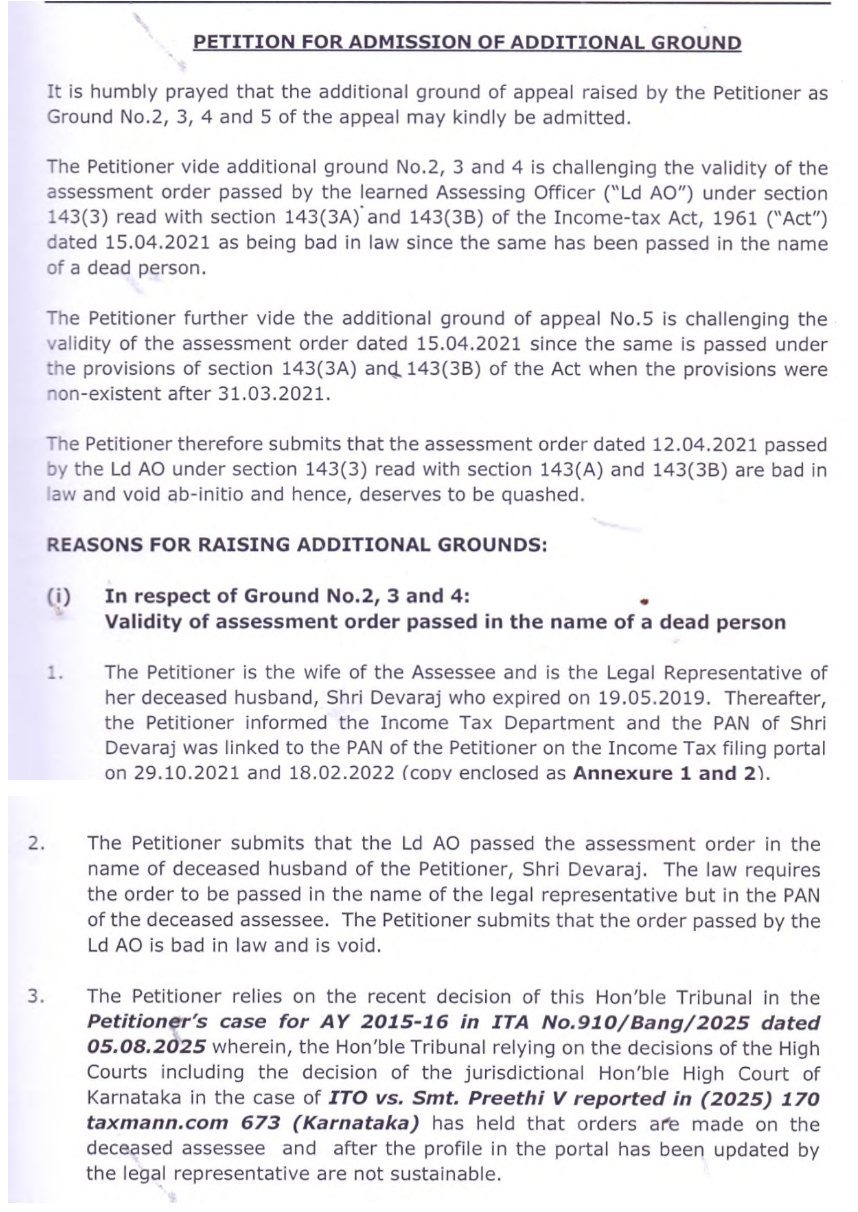

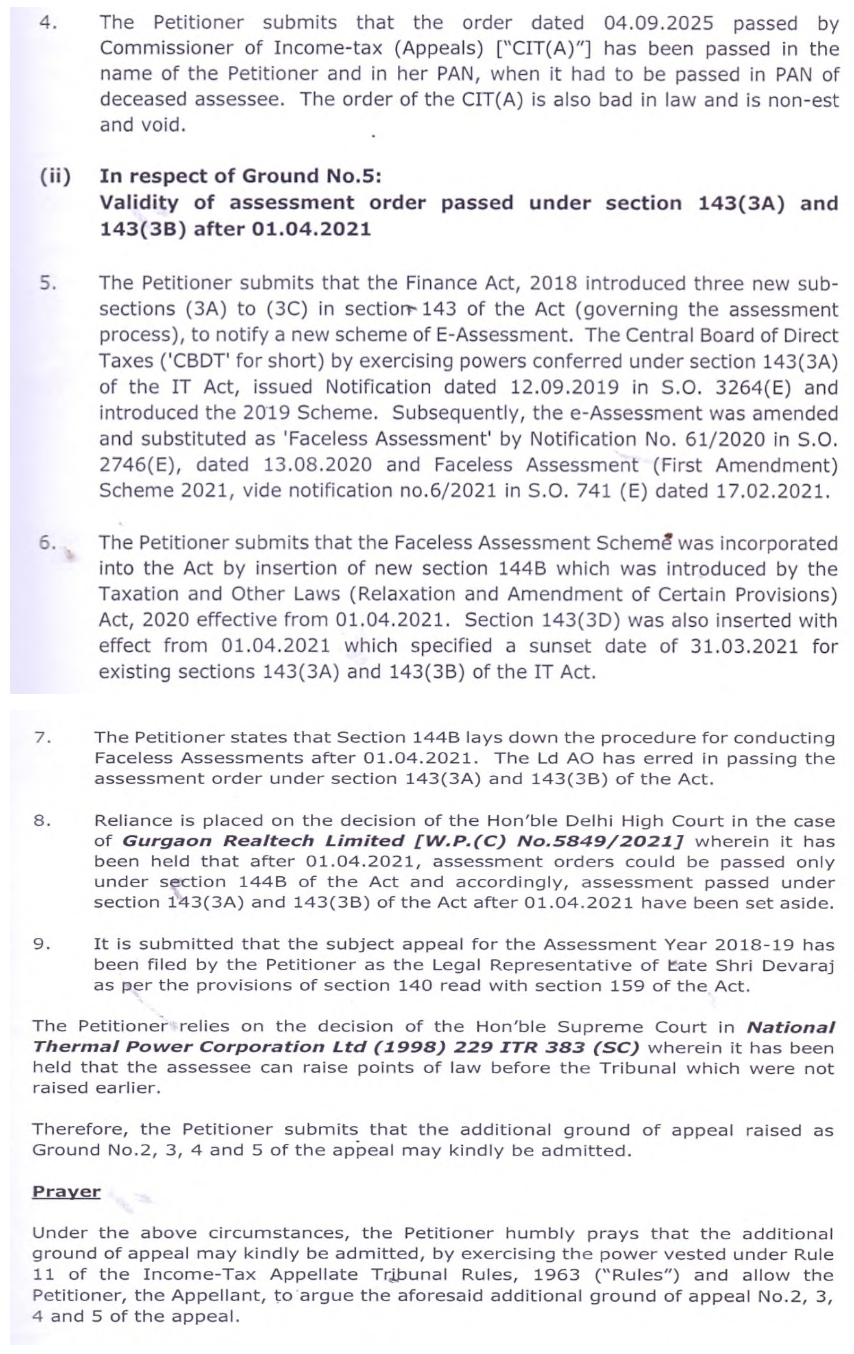

3. The assessee has raised the following additional grounds of appeal:-

3.1 We have heard both the parties on admission of additional grounds. The Lucknow bench of the Hon’ble Allahabad High Court in the case of CIT Vs. Sahara India (2012) 347 ITR 331 held that a legal issue can be raised at any stage but there shall be good reason for admitting the additional ground.In our Opinion all the facts are already on record and there is no necessity of investigation of any fresh facts for the purpose of the adjudication

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :