INCOME TAX APPELLATE TRIBUNAL (CHENNAI BENCH)

ABY T. VARKEY, Judicial Member, S.R.RAGHUNATHA, Accountant Member

Vasanthi Ragunathan – Appellant

Versus

ITO – Respondent

ITA No.2896/Chny/2025

| Table of Content |

|---|

| 1. background of appeal and reassessment proceedings (Para 1 , 2) |

| 2. assessee challenges s.148 notice validity due to improper sanction authority (Para 3 , 4) |

| 3. notice u/s 148 invalid; reassessment quashed for lack of pccit approval (Para 6 , 7 , 8) |

| 4. appeal allowed; other grounds academic (Para 9 , 10) |

आदशे/ORDER

PER ABY T. VARKEY, JM:

This is an appeal preferred by the assessee against the order of the Learned Commissioner of Income Tax (Appeal), (hereinafter referred to as ‘Ld.CIT(A)‘), Delhi, dated 12.09.2025 for the Assessment Year (hereinafter referred to as ‘AY’) 2018-19.

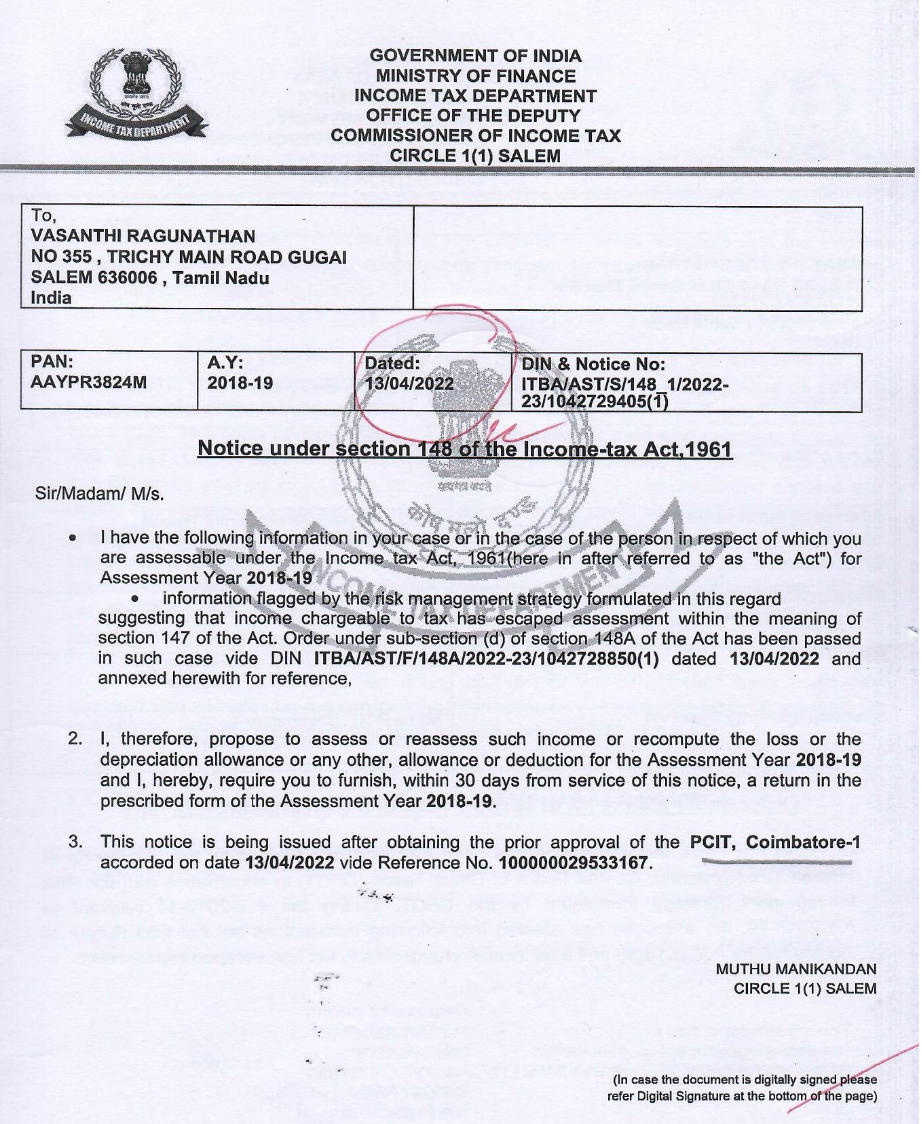

2. The assessee is an individual and didn’t file the return of income (RoI) for A.Y 2018-19, despite the assessee has time-deposit other than interest on securities of ₹20 lakhs and that she had sold immovable property at ₹1.80 Crs. Based on this facts/information, the A.O issued notice u/s. 148A(b) of the Income Tax Act, 1961 (hereinafter referred to as ‘the Act’) proposing to reopen; and subsequently the AO passed an order u/s.148A(d) of the Act on 13.04.2022 and issued notice u/s. 148 of the Act on the same date, conveying his desire to reopen the assessment for AY 2018-19. Pursuant to which, assessee filed RoI on 25.01.2024 declaring ₹3,32,650/-. The AO completed the assessment u/s. 147 of the Act assessing the income of the assessee total income at Rs.56,71,398/-. Aggrieved, the assessee filed further appeal before the CIT(A), who dismissed the appeal. The assessee is in appeal before this Tribunal against the order of the Ld CIT(A).

3. The Ld. Authorized Representative (AR) of the assessee submitted that through ground No.3, the assessee is challenging the validity of notice u/s. 148 of the Act issued after expiry of three years with the approval of Principle Commissioner of Income Tax (PCIT), instead of Principle Chief Commissioner of Income Tax (PCCIT). The Ld. AR further submitted that if the said ground is adjudicated in favour of the assessee, the other grounds on legal as well as on merits would become academic. Accordingly, we will first proceed to consider the said legal contention.

4. In this regard, the Ld. AR submitted that the notice under section 148 is dated 13.04.2022, which event is undisputedly beyond the period of 3 years from the end of the relevant AY; and therefore as per the provisions of Section 151 of the Act, the AO should have obtained the approval from Principle Chief Commissioner of Income Tax (PCCIT), instead, in the present case the AO has obtained approval from Principle Commissioner of Income Tax (PCIT), Coimbatore, while issuing notice under section 148 and therefore the notice is invalid. For such a proposition, he relied on the decision of this Tribunal in the case of Meganapuram Primary Agricultural cooperative Credit Society vs PCIT (ITA No.895/Chny/2025 dated 19.09.2025 wherein similar issue cropped up, and the Tribunal allowed the ibid legal issue in favor of assessee, by holding as under;-

“40. We find that the Show Cause Notice u/s.148A(b) of the Act came to be issued on 23.03.2022 in proposing to issue notice u/s.148 of the Act and as a consequence proposing to assumption of jurisdiction in terms of Section 147 of the Act. The assessee had filed its response to the said notice on 29.03.2022 and the AO had issued a letter dated 04.04.2022 in seeking further details in support of the submissions of the assessee and ultimately the order u/s.148A(d) of the Act came to be passed on 19.04.2022 by the AO, wherein the AO deemed it fit to issue notice u/s.148 of the Act. Thus, the notice u/s.148 of the Act came to be issued on 19.04.2022 for the A.Y. 2018-19.

41. The provisions of Section 151 defines the sanctioning authority and the relevant provisions as it stood at that point in time reads as under:

“151. Specified authority for the purposes of section 148 and section 148A be,—

(i) Principal Commissioner or Principal Director or Commissioner or Director, if three years or less than three years have elapsed

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :