INCOME TAX APPELLATE TRIBUNAL (PUNE BENCH)

MANISH BORAD, Accountant Member, ASTHA CHANDRA, Judicial Member

Ajay Abasaheb Khamkar – Appellant

Versus

Income Tax Officer – Respondent

ITA No.2662/PUN/2025

| Table of Content |

|---|

| 1. factual background of search and seized material (Para 1 , 6 , 7) |

| 2. assessee's grounds challenging reassessment validity (Para 2) |

| 3. parties' arguments on s.153c vs s.148 applicability (Para 3 , 4) |

| 4. section 153c mandatory for pre-2021 third-party search material (Para 5 , 8 , 9 , 10) |

| 5. appeal allowed; reassessment quashed for lack of jurisdiction (Para 11 , 12) |

ORDER

PER DR. MANISH BORAD, ACCOUNTANT MEMBER :

The captioned appeal at the instance of assessee pertaining to A.Y.2019-20 is directed against the order dated 27.10.2025 framed by National Faceless Appeal Centre, Delhi arising out of Assessment Order dated 27.12.2024 passed u/s. 147 r.w.s.144B of the Income Tax Act, 1961 (in short ‘the Act’).

2. Assessee has raised following grounds of appeal :

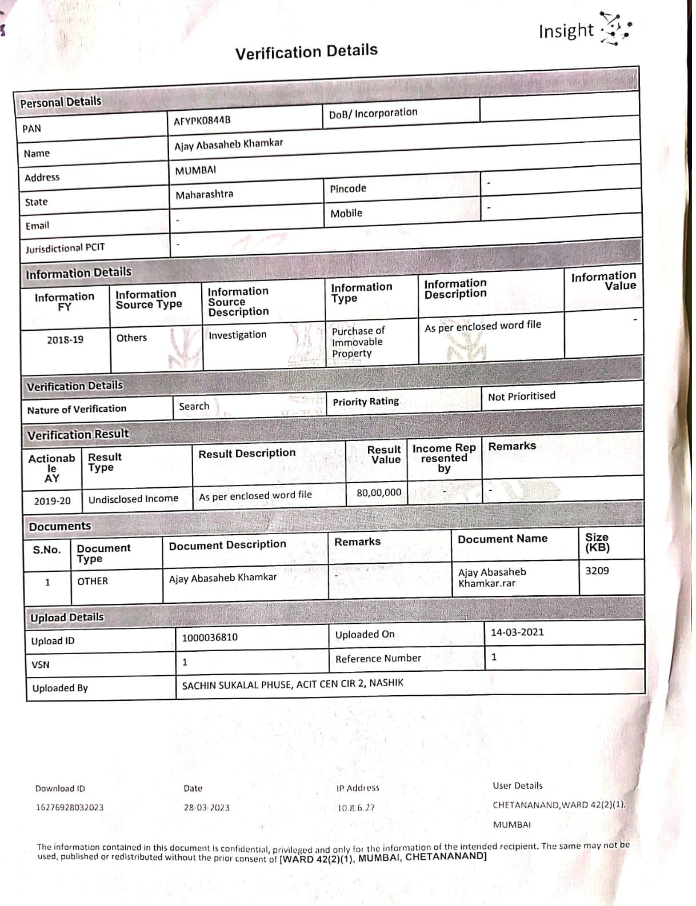

“1]. The learned CIT(A) erred in upholding the validity of notice u/s 148 without appreciating that the reasst. proceedings in the instant case were initiated on the basis of certain documents allegedly relating to the assessee which were found in the course of search action conducted on Mr. Rajendra Abhale on 20.02.2019 i.e. prior to 01.04.2021 and hence, action, if any, ought to have been initiated under the special provisions of section 153C which were applicable in the above scenario and therefore, the reasst. proceedings initiated by resorting to the general provisions of section 148 in the present case, may be declared as null and void in law.

2] The learned CIT(A) erred in upholding the validity of notice u/s 148 without appreciating that the notice u/s 148 dated 21.04.2023 issued by the Jurisdictional A.O. was contrary to the mandate of section 151A read with CBDT Notification dated 29.03.2022 and hence, the said notice issued by ITO, Ward 42(2)(1), Mumbai, ought to have been declared as null and void in law.

3] The learned CIT(A) erred in upholding the validity of notice u/s 148 and the asst. order u/s 147 without appreciating that till the completion of the asst. proceedings, the A.O. has not confronted the approval u/s 151 obtained from the higher authority before issuing the notice u/s 148 and hence, the notice u/s 148 as well as the consequential asst. order passed u/s 147 without following the directions of Honorable Jurisdictional Bombay High Court in case of Tata Capital Financial Services Ltd. 443 ITR 127, and various other Honorable Courts, may be declared as null and void in law.

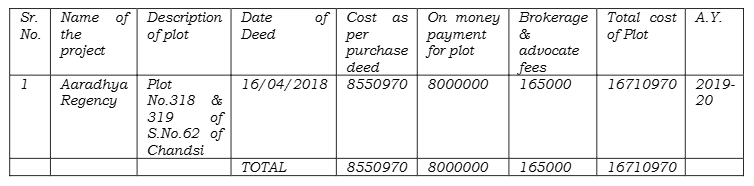

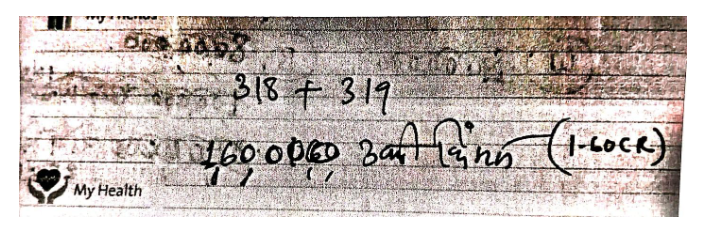

4] The learned CIT(A) erred in confirming the addition of Rs.80,00,000 made by the A.O. towards alleged on-money received on sale of plots on the basis of handwritten loose paper seized during search action u/s 132 conducted on the premises of Mr. Abhale on 20.02.2019 and letter dated 19.06.2019 filed by Mr. Abhale before Inv. Wing, without appreciating that the said addition was not justified on facts and in law.

5] The learned CIT(A) failed to appreciate that the impugned loose paper was neither authored nor signed by the assessee and the same did not contain details of any accounted transactions therein which could be corroborated with any actual transactions and therefore, the said loose paper found with third party could not be relied upon to make any addition in hands of the assessee since the presumption u/s 132(4A) was not attracted in this case.

6] The learned CIT(A) erred in not appreciating that the admission made by Mr. Abhale in the letter dated 19.06.2019 filed before Inv. Wing to suit his own requirements of availing tax benefit etc. could not be used to make any addition in hands of the appellant in the absence of any corroborative material brought on record by the A.O. especially when the opportunity of cross examination of Mr. Abhale was denied to the assessee.

7] The learned CIT(A) ought to have appreciated that the presumption drawn by the A.O. that the FMV of the impugned land was Rs.1.60 Crs. i.e. around three times of its Govt. Valuation of Rs.58 lakhs was highly improbable and the A.O. had not brought any material in support of this apparently unjustifie

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :