INCOME TAX APPELLATE TRIBUNAL (CHENNAI BENCH)

George George K, Vice President, Padmavathy S, Accountant Member

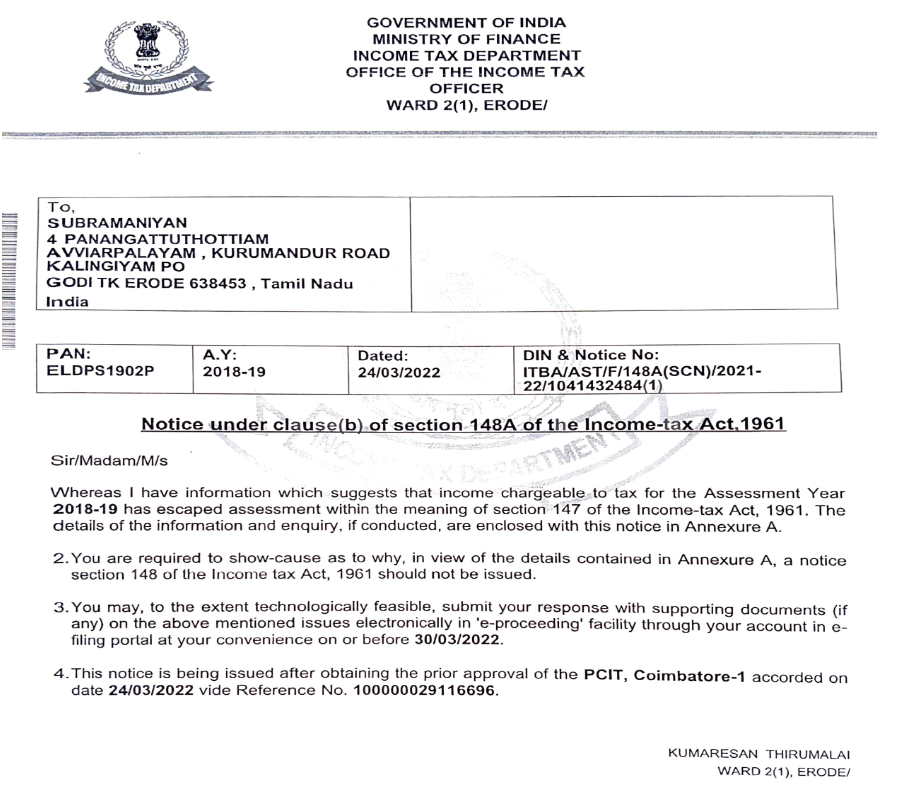

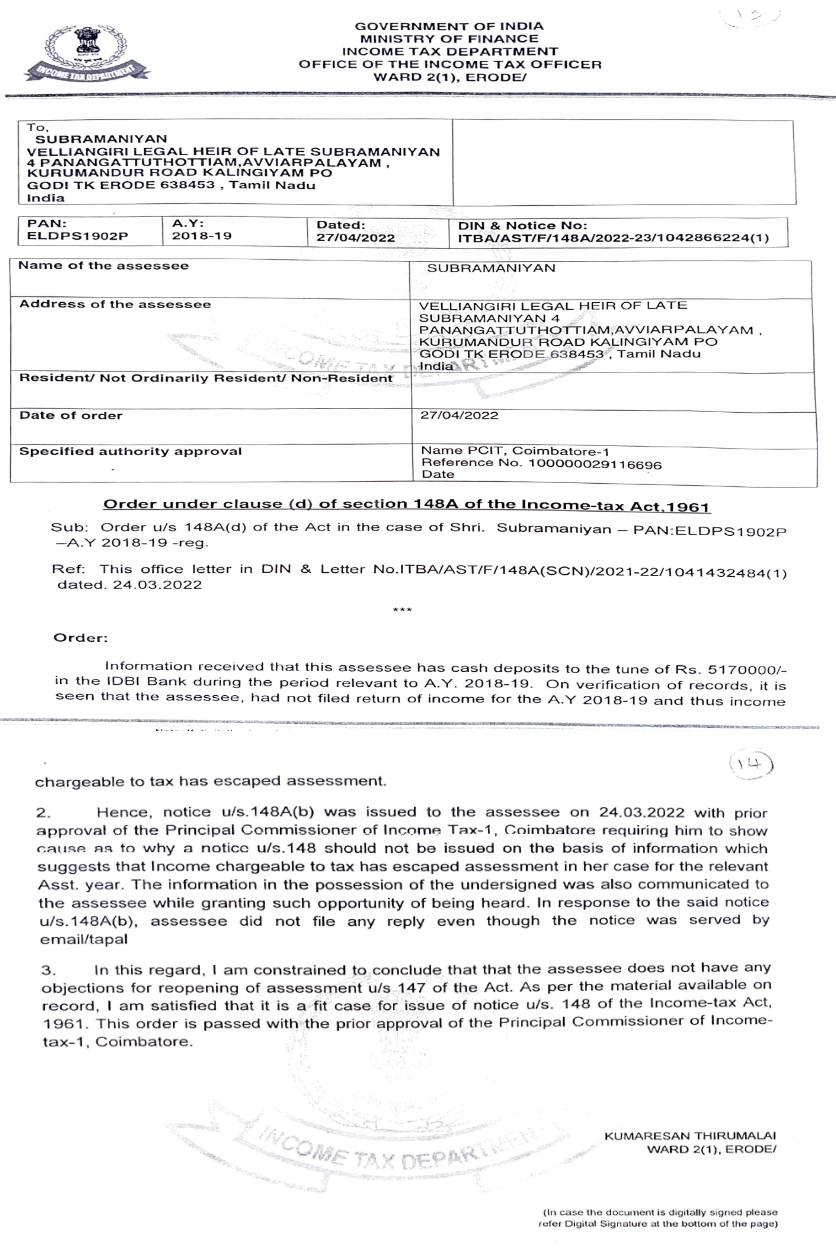

Subramaniyan – Appellant

Versus

Income Tax Officer – Respondent

| Table of Content |

|---|

| 1. reassessment initiated via notice to deceased assessee invalid. (Para 2 , 5 , 6) |

| 2. delays in appeals condoned for reasonable cause. (Para 3 , 4) |

| 3. no jurisdiction without fresh notice to legal heir; proceedings quashed. (Para 7 , 8) |

| 4. assessee's appeal allowed. (Para 9) |

आदेश/ORDER

PER PADMAVATHY.S, A.M:

This appeal by the assessee represented by legal heir is against the order of the Commissioner of Income Tax (Appeals)/National Faceless Appeal Centre (NFAC), Delhi, (in short "CIT(A)") passed u/s. 250 of the Income Tax Act, 1961 (in short "the Act") dated 30.09.2025 for Assessment Year (AY) 2018-19.

2. The assessee is an individual and passed away on 06.07.2020. The A.O based on information received that there was cash deposits maintained in the IDBI Bank to the tune of Rs. 51,70,000/-, reopened the assessment by issue of notice u/s. 148A(b) of the Act on the legal heir of the assessee. The A.O concluded the assessment by treating the entire amount as unexplained u/s. 69A of the Act. Aggrieved, further appeal before the CIT(A) was filed by the assessee represented by the legal heir. There was a delay of 360 days in filing the appeal before the CIT(A). The CIT(A) dism

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :