INCOME TAX APPELLATE TRIBUNAL (RAJKOT BENCH)

Arjun Lal Saini, Accountant Member

Akolvadi Seva Sahkari Mandali Ltd. – Appellant

Versus

Income Tax Officer, wd-4 – Respondent

ITA No. 871/RJT/2025|ITA No. 902/RJT/2025|ITA No. 873/RJT/2025

| Table of Content |

|---|

| 1. consolidated appeals on reassessment proceedings (Para 1 , 2) |

| 2. condonation of delay in filing appeal (Para 3) |

| 3. grounds challenging cit(a) dismissal and reassessment (Para 4) |

| 4. facts of cash deposits and ao's rejection (Para 5 , 6 , 7 , 8 , 9) |

| 5. disallowance of 80p deduction due to non-filing (Para 10 , 11) |

| 6. cit(a) confirms non-est return and disallowance (Para 12) |

| 7. assessee argues addition on different footing (Para 13 , 14 , 15) |

| 8. revenue defends valid notice under new regime (Para 16) |

| 9. reassessment quashed per jet airways precedent (Para 17 , 18) |

| 10. all appeals allowed, other issues infructuous (Para 19 , 20 , 21) |

आदेश/ORDER

Per, Dr. Arjun Lal Saini, AM ;

Captioned three appeals filed by the different assessees, pertaining to different Assessment Years 2018-19 & 2019-20, are directed against the separate orders passed under section 250 of the Income Tax Act, 1961 (hereinafter referred to as “the Act”) by National Faceless Appeal Centre (NFAC), Delhi/Commissioner of Income-tax (Appeals), which in turn arise out of separate orders passed by the Assessing Officer, u/s 147 r.w.s. 144 of the Income Tax Act, 1961.

2. Since, the issue involved in these three appeals are identical and similar, therefore, these appeals have been heard together and a consolidated order is being passed for the sake of convenience and brevity. The facts as well as grounds narrated in ITA 871/Rjt/2025 for AY 2018-19 have been taken into consideration for deciding these three appeals en masse.

3. When the matter was called for hearing, the learned AR for the assessee at the outset submitted that the appeal in ITA No.873/RJT/2025, for assessment year 2019-20, has been filed by the assessee belatedly. The learned AR adverted my attention to the affidavit filed in this regard citing reasons for condonation of delay and urged for a benign view and sought condonation of delay of 100 days in filing the appeal before the Tribunal. A perusal of the affidavit gives me an impression of existence of mitigating circumstances to enable me to exercise my discretion in favour of the assessee. Accordingly, the delay is condoned

4. Grounds of appeal raised by the assessee in lead case in ITA 871/Rjt/2025 for AY 2018-19, are as follows:

1. The Commissioner of Income Tax (Appeals) erred in dismissing the appeal. The CIT(A) erred in holding that since the Appellant had not filed their return of income in time, the delayed return is Non Est return & no cognizance can be take on the return.

2. Without prejudice to ground no 1, the CIT(A) erred in not disposing the following grounds of the appellant.

1. The learned Assessing Officer erred in reopening the assessment under section 148 of the Income tax Act. The reopening of the assessment is neither justified on facts nor justified in law.

2. Without prejudice to ground no.1, the learned Assessing Officer erred in passing the order under section 144 of the Income tax Act.

3. Without prejudice to ground no.1 and 2, addition of other income is not justified in law where no addition is made on the basis of which the assessment has been reopened under section 148 of the Act.

4. Without prejudice to ground no.1,2 and 3, the assessment of the co-operative society at the total income of Rs.20,72,127/- and computation of tax at Rs. 13,86,518/- is unwarranted and unjustified.

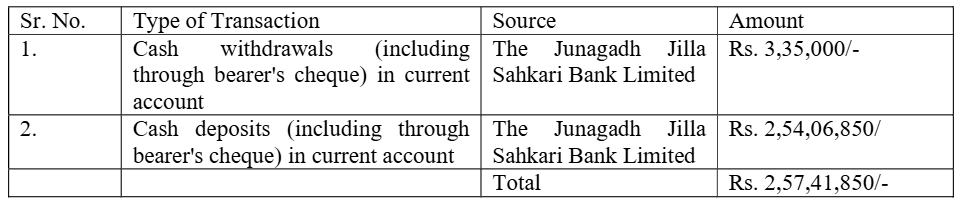

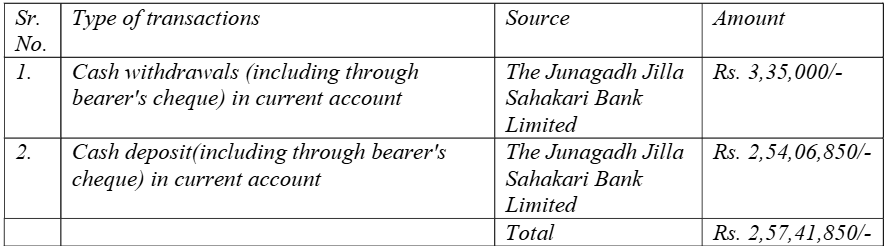

5. The relevant material facts, as culled out from the material on record, are as follows. An information has been received in category of non -filer management system (NMS) on insight portal that during the period under review, the assessee had entered into significant financial transaction with the Junagadh Jilla Sahkari Bank Limited as per following details:-

Further, as the assessee failed to furnish its return of income within the time allowed under section 139 of the Income tax Act, 1961, therefore, after following the procedure laid down under section 148 of the Income tax Act, 1961, a query letter cum show cause notice under clause (b) of section 1

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :