INCOME TAX APPELLATE TRIBUNAL (CHENNAI BENCH)

ABY T. VARKEY, Judicial Member, PADMAVATHY.S, Accountant Member

Joyson Anand Abhishek Safety Systems Pvt. Ltd. – Appellant

Versus

Dy. Commissioner of Income Tax – Respondent

| Table of Content |

|---|

| 1. cross appeals on tp adjustments from cit(a) order (Para 1 , 2 , 3) |

| 2. remit forex loss treatment for consistent non-operating classification (Para 4 , 5 , 6 , 7 , 11) |

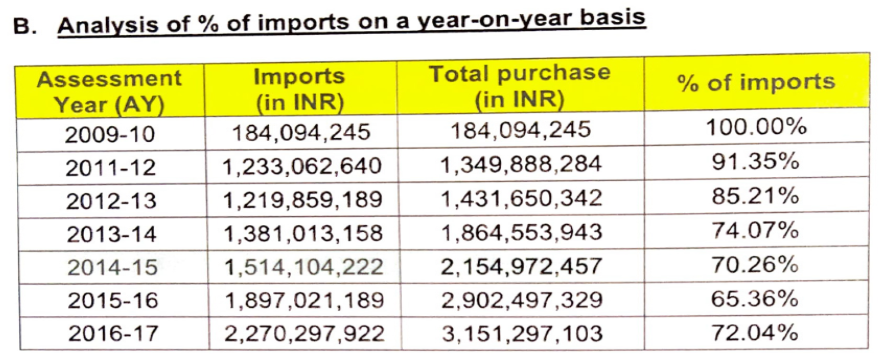

| 3. remit customs duty adjustment for cost impact verification (Para 8 , 9 , 12) |

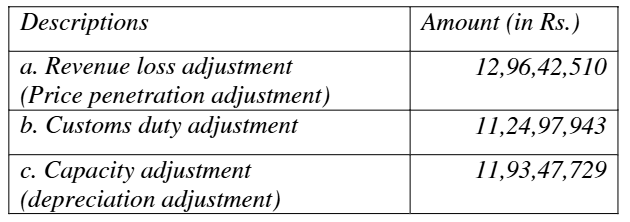

| 4. remit price penetration adjustment for quantitative details (Para 13) |

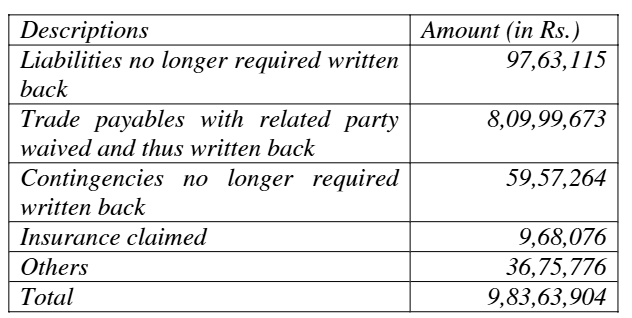

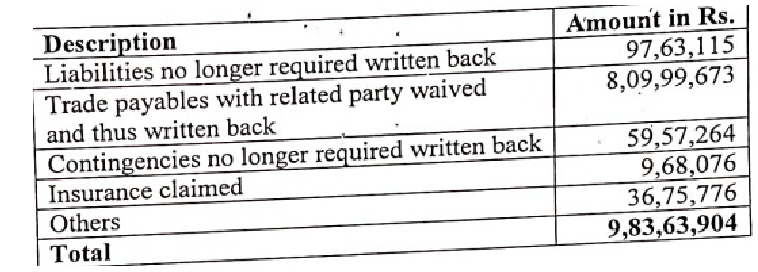

| 5. uphold trade payables write-back as operating; remit others (Para 14 , 15 , 16 , 17) |

| 6. direct cash pli computation excluding depreciation (Para 18 , 19 , 20) |

| 7. appeals allowed statistically; co dismissed (Para 21 , 22) |

आदेश/ORDER

PER PADMAVATHY.S, A.M:

These cross appeals by the assessee and the Revenue and the Cross Objections (COs) of the assessee are against the order of Commissioner of Income Tax (Appeals), Chennai-16 (in short "the CIT(A)") passed u/s. 250 r.w.s 254 of the Income Tax Act, 1961 (in short "the Act") dated 28.06.2024 for Assessment Year (AY) 2014-15. The grounds raised by the assessee are as given below:

“Issue no. 1-Prejudicial to the interest of the Appellant:

The Ld. TPO, the Ld. AO and Ld. CIT(A) have erred, in facts and in circumstances of the case and in law by rejecting the analysis undertaken by the Appellant to determine the ar

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :