INCOME TAX APPELLATE TRIBUNAL (HYDERABAD BENCH)

SURENDER KUMAR BHOJWANI HYDERABAD – Appellant

Versus

ITO INTL. TAXTION -1 HYDERABAD – Respondent

ORDER

PER RAVISH SOOD, JM:

The present appeal filed by the assessee is directed against the order passed by the Commissioner of Income Tax (Appeals)-10, Hyderabad, dated 09/09/2025, which in turn arises from the order passed by the Assessing Officer (for short, “AO”) under section 143(3) r.w.s 147 of the Income Tax Act, 1961 (for short, “the Act”), dated 21/11/2019 for the Assessment Year (AY) 2013-14. The assessee has assailed the impugned order of the CIT(A) on the following grounds of appeal:

“1. On the facts and in the circumstances of the case, the order of the Id. CIT(A) is erroneous both on facts and in law.

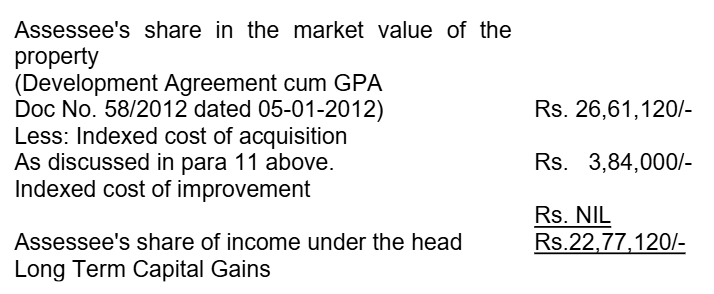

2. The Id. CIT(A) erred in sustaining the addition made by the AO of Rs.22,77,120 as undisclosed income under the head Long Term Capital Gains' on entering into development agreement.

3. The Id. CIT(A) erred in denying the deduction u/s.54F of Act on the alleged ground that the appellant has not claimed any deduction in the return of income filed in response to notice issued u/s.148 of the Act and further has not filed any evidence in support of investment of sale consideration in the residential unit within the time frame as prescribed by the Act for claiming exemption u/s.5

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :