INCOME TAX APPELLATE TRIBUNAL (RAJKOT BENCH)

Arjun Lal Saini, Accountant Member, Dinesh Mohan Sinha, Judicial Member

Nathabhai Parsana (LR. Ganeshbhai Parsana) – Appellant

Versus

ACIT CIR-2(1) – Respondent

ITA No. 412/RJT/2023

| Table of Content |

|---|

| 1. appeal against recharacterization of inherited land sale from capital gain to business income. (Para 1 , 2 , 3 , 4 , 5 , 6) |

| 2. limited scrutiny violated without permission; inherited land sale is capital gain. (Para 7 , 8 , 9 , 10) |

| 3. revenue defends assessing officer's business income classification. (Para 11) |

| 4. inherited land conversion and sale without purchase intent is capital gain, not trade. (Para 12 , 13 , 14) |

| 5. assessee's appeal allowed; additions deleted as capital gains. (Para 15 , 16) |

आदेश /ORDER

Per, Dr. Arjun Lal Saini, AM:

Captioned appeal filed by the assessee, pertaining to Assessment Year 2016-17, is directed against the order passed under section 250 of the Income Tax Act, 1961 (hereinafter referred to as “the Act”) by National Faceless Appeal Centre (NFAC), Delhi / Commissioner of Income-tax (Appeals) (in short ‘Ld. CIT(A)’), dated 23.11.2025, which in turn arises out of an assessment order passed by the Assessing Officer u/s. 143(3) of the Act on 18.12.2018.

2. Although, this appeal filed by the assessee, for assessment year 2016-17, contains multiple ground of appeals. However, at the time of hearing we have carefully perused all the grounds raised by the Assessee. We find that most of the grounds raised by the assessee, are either academic in nature or contentious in nature. However, to meet the end of justice, we confine ourselves to the core of the controversy and main grievances of the asssessee. There are two main grievances of the assessee, which are as follows:

(i) Issue of limited scrutiny: The case of the assessee was selected for limited scrutiny to examine the long-term capital gain, however, the assessing officer made addition on different item under the head, “income from business and profession”, without converting limited scrutiny into full scrutiny, by taking the permission from higher income tax authority. Hence, assessment order should be quashed.

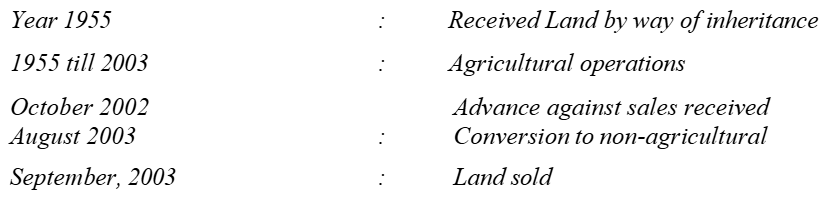

(ii) Long term capital gain Vs. Income from business. On merit, the grievance of the assessee, in this appeal is that the assessee sold the ancestor agricultural land and paid long-term capital gain. Some part of agricultural land was gifted to family members. Therefore, as per assessee, it should not be assessed under the head business income, as there is no motive to do the business, hence, it should be assessed under the head capital gain, and the assessee, accordingly, has shown the long-term capital gain in the return of income and paid the taxes there on. Hence, sale of ancestor agricultural land should be treated capital asset, therefore, assessing officer as well as ld CIT(A) both erred in treating the business income.

3. The facts of the case which can be stated quite shortly are as follows: the assessee filed return of income, declaring an income of Rs.15,38,290/-, on 30.08.2017. The case of the assessee was selected for limited scrutiny through CASS. Hence, a notice u/s 143(2) of the Act, was issued to the assessee, on 21- 09-2018, which was duly served upon the assessee through ITBA, portal. Various notices u/s 142(1) cum questionnaire were issued to the assessee. In compliance thereto, the assessee filed his written submission, before the assessing officer. The assesse derives income from capital gain and income from other sources, during the year, under consideration. During the assessment proceedings, it was noticed by the assessment officer that the assessee was involved in the activity of developing and selling of plots. Hence, a show cause notice was issued to the assessee on 15.12.2018, treating the sales consideration received on the selling of the sub-plots, as business income for the year under consideration instead of capital gain as claimed by the assessee. In compliance thereto, the assessee filed his written submission, before the assessing officer, stating that land was inherited from the grand fathers, hence there is no motive to do the business. The assessee has never purchased the land, however, whatever

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :