INCOME TAX APPELLATE TRIBUNAL (MUMBAI BENCH)

Vikram Singh Yadav, Accountant Member, Rahul Chaudhary, Judicial Member

Umesh A. Mishra – Appellant

Versus

Income Tax Officer Ward 10(3)(1), Mumbai – Respondent

ITA No.5216/MUM/2025

| Table of Content |

|---|

| 1. appeal against nfac dismissal with 1414-day delay. (Para 1 , 2) |

| 2. condone delay for sufficient cause favoring substantial justice. (Para 3 , 4 , 5) |

| 3. admit additional ground on jurisdictional defect in 143(2) notice. (Para 6 , 7 , 8 , 9 , 10) |

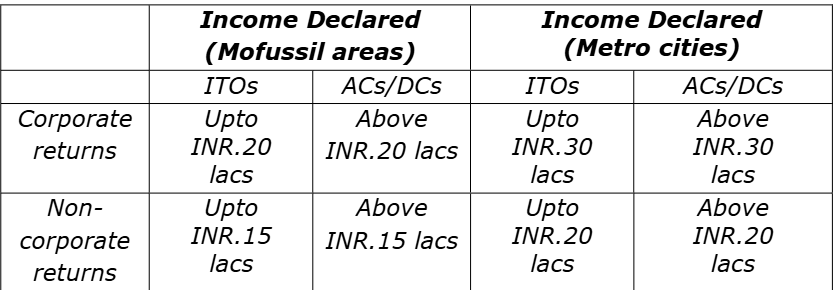

| 4. cbdt instruction no.1/2011 mandates dc/ac jurisdiction over inr 20l income. (Para 11 , 12 , 13 , 14) |

| 5. quash invalid 143(2) notice and assessment order. (Para 15 , 16) |

ORDER

Per Rahul Chaudhary, Judicial Member:

1. The present appeal preferred by the Assessee is directed against the Order, dated 12/08/2021, passed by the National Faceless Appeal Centre (NFAC), Delhi [hereinafter referred to as the ‘CIT(A)’ whereby Learned CIT(A) had dismissed the appeal against the Assessment Order, dated 16/12/2016, passed under Section 143(3) of the Income Tax Act, 1961 [hereinafter referred to as ‘the Act’], for the Assessment Year 2014-2015.

2. There was delay of 1414 days in filing the present appeal before the Tribunal. When the appeal was taken up for hearing Learned Authorized Representative for the Assessee appearing before us submitted that the delay in filing the present appeal be condoned and in this regard reliance was placed upon the affidavit filed by the Assessee along with application seeking condonation of delay in filing the appeal which reads as under:

“1. That, I have preferred an appeal before the Hon'ble ITAT against the order dated 12.08.2021 passed by the CIT(A) under section 250 of the Income Tax Act, 1961 [hereinafter referred to as "the Act"].

2. That, I had appointed Shri S L Jain, Chartered Accountant to handle my Income Tax matters and appear before the authorities.

3. That, the appeal before the Ld.CIT(A) was filed by Shri Jain against the assessment order for the A.Y. 2014-15 passed in my case. While filing the Form 35, Shri Jain had provided his Email address [i.e. sljain09@gmail.com] for the sake of receiving communication from NFAC.

4. That, before the Ld.CIT(A), Shri S L Jain made a submission on 01.02.2021 giving certain details. However, further notices dated 23.03.2021, 11.06.2021 and 08.07.2021 could not be responded by Mr Jain as he was not regularly attending the office due to ongoing phase of COVID-19 Pandemic.

5. That the Ld.CIT(A) vide order dated 12.08.2021 dismissed the appeal for he A.Y/2014-15. The said appeal order was sent to the E-mail ID of Shri S Jain as his E-mail ID was given in Form 35 and I had no knowledge of the same.

6. That, Shri S L Jain could not check his E-mail and take immediate action against the appeal order as he was going through some health issues. Subsequently, he was completely bed ridden and stopped attending the office. Thus, the order passed by the CIT(A) escaped attention and the appeal before the ITAT could not be filed within due date.

7. That, I was under the bonafide belief that the appeals for the A.Y. 2013-14 and 2014-15 are pending before the CIT(A). On 26.07.2025, I received a recovery notice dated 23.07.2025 from the Jurisdictional Assessing Officer wherein the outstanding demand for several assessment years was mentioned which included the demand of Rs.4,89,640/- for the A.Y. 2014-15.

8. That, immediately after receiving the recovery notices, I approached another tax consultant, who was recently appointed because of Mr. Jain's non-availability due to his health issues.

9. That, the tax consultant, in reply to the above recovery notices, filed response on 30.07.2025 wherein he has submitted year wise reply. In the said reply, he submitted that the demand for the A.Y. 2011-12 and 2012-13 would ould be substantially reduced in the set aside proceedings pursuant to the THARASHTR ITA Torder/The order giving effect to the ITAT order for the A.Y. 2011-12 and 2012-13 is awaited. With respect to the demands for the A.Y. 2013-14 and 2014-15, he submitted that the same are disputed in the appeal before the d.CIT(A).

10. That, while filing the response to the recovery notice dated 23.07.2025, my tax consultant discovered f

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :