INCOME TAX APPELLATE TRIBUNAL (CHANDIGARH BENCH)

LALIT KUMAR, JM, KRINWANT SAHAY, AM

The ITO – Appellant

Versus

Gulmohar Associates – Respondent

ITA No. 64/Chd/2025 | Cross Objection No. 32/Chd/2025

| Table of Content |

|---|

| 1. parties contest unexplained credits addition and reassessment validity. (Para 2 , 3 , 9 , 10) |

| 2. reassessment initiated on alleged bank credits; assessee explains as contributions. (Para 4) |

| 3. cit(a) deletes addition under s.69a for recorded, explained credits. (Para 6) |

| 4. tribunal upholds deletion; s.69a conditions unmet. (Para 11 , 12 , 13 , 14) |

| 5. reassessment invalid due to incorrect factual basis. (Para 16 , 17 , 18 , 20 , 21 , 22) |

आदेश/Order

PER KRINWANT SAHAY, A.M:

The present appeal by the Revenue and Cross Objection by the Assessee has been filed against the order passed by the Ld. CIT(A)/NFAC, Delhi dated 06.12.2024 pertaining to Assessment Year 2014-15.

2. Revenue has raised the following grounds in its appeal.

1. Whether on the facts and in the circumstances of the case, the CIT(A) was right in aw in allowing the appeal of the assessee by directing the AO to delete the addition made for Rs 8,44,25,000/- on account of unexplained credits.

2. Whether on the facts and in the circumstances of the case, the CIT(A) was right in law in deleting the addition made for Rs 8,44,23,000/- on account of unexplained credits by ignoring the fact that assessee had not furnished to the AO requisite details with respect to credit entries.

3. Whether on the facts and in the circumstances of the case, the CIT(A) was right in law in allowing the appeal of the assessee even when the assessee was specifically asked to provide the details with respect to credit entries received from various parties along with the relevant documentary evidence.

4. The Ld. CIT Appeal has erred in deleting the entire addition of Rs. 8,44,23,000/- made by A.O. u/s 69A of the Income-tax Act, 1961.

5. Whether on the facts and in the circumstances of the case, the CIT(A) was right in law in deleting the addition of Rs. 14,00,000/- on account of unexplained cash deposits without making any discussion regarding the same in their order.

6. The Appellant craves leave to add, demand or delete any of the grounds of appeal during the appellate proceedings.

3. Assessee has raised the sole ground in its Cross Objection which read as under:-

"That order passed u/s 250 of the Income-Tax Act, 1961 is against law and facts on the file in as much as the Learned Commissioner of Income Tax (Appeals) was not justified in not adjudicating the ground relating to initiation of proceedings u/s 147 of the Act"

4. The assessee, a Partnership Firm set up to carry on the business of real estate activities such as resale of properties, acting as builder and colonizers had not carried out any business during the year under appeal. For the Assessment Year under appeal the Assessee had not originally filed its return of income. On the basis of information available with the department, it was noticed that the assessee had substantial non-cash credits and cash deposits in its bank account during the financial year 2013-14, which remained unexplained.

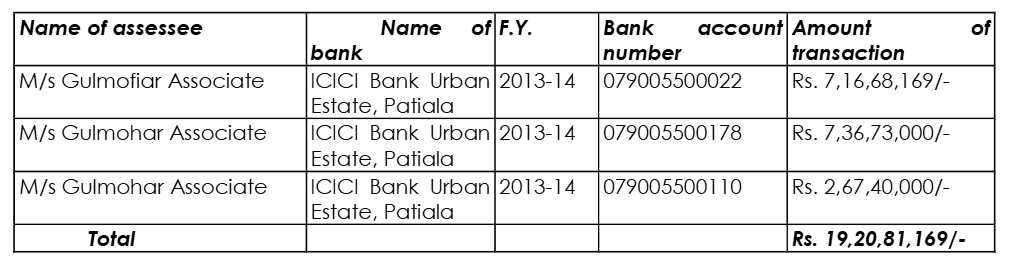

4.1 In particular, the reassessment proceedings were initiated on the basis of information received from the Insight Portal alleging that the assessee had maintained the following three bank accounts with ICICI Bank and had non- cash credits aggregating to Rs 19,20,81,169/- during the relevant previous year details of which read as under:-

4.2 Accordingly, the case was reopened under section 147 of the Income- tax Act, 1961 after obtaining due approval from the competent authority and notice under section 148 dated 31.03.2021 was issued.

4.3 In response to the notice under section 148, the assessee filed it return of income on 30.12.2021 declaring total income at Nil. During the reassessment proceedings, statutory notices under sections 142(1) and 143(2) of the Act were issued electronically, calling upon the assessee to furnish details such as bank statements, sources of cash and non-cash credits, nature of transactions, and supporting documentary evidence. The assessee submitted bank statements, computation of income and balance sheet, and conte

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :