INCOME TAX APPELLATE TRIBUNAL (CHENNAI BENCH)

Manu Kumar Giri, Judicial Member, S. R. Raghunatha, Accountant Member

Paul System Technologies Private Limited – Appellant

Versus

Income Tax Officer – Respondent

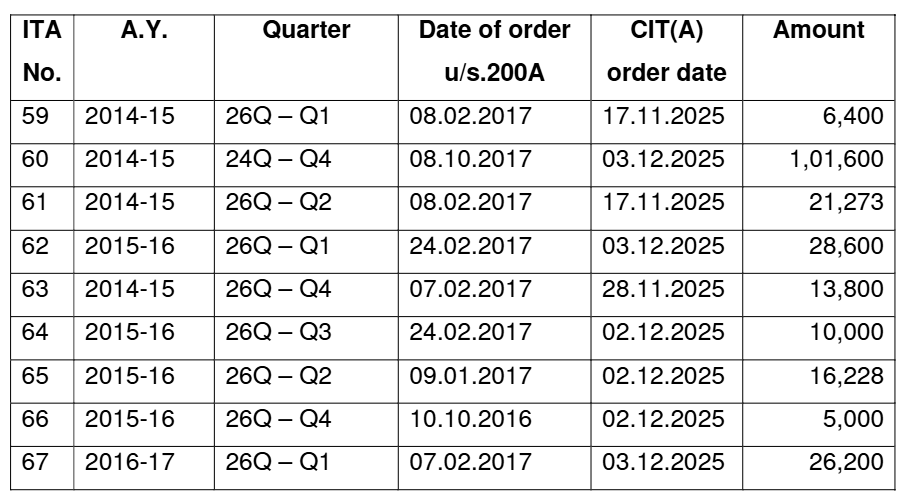

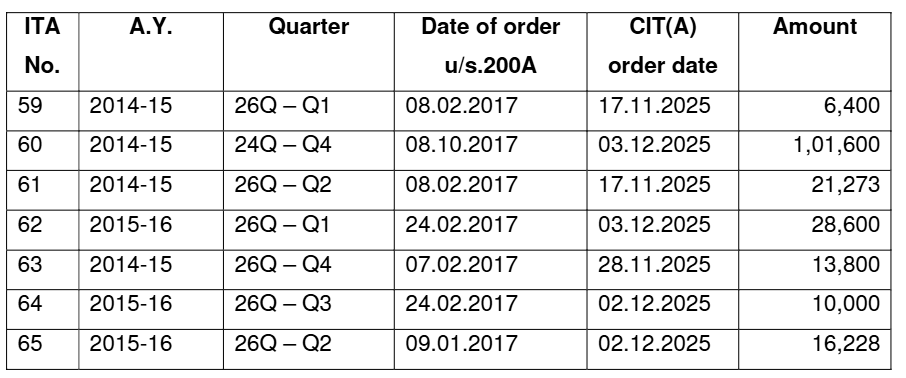

ITA Nos.: 59, 60, 61, 62, 63, 64, 65, 66 & 67/CHNY/2026

| Table of Content |

|---|

| 1. belated tds returns processed with late fee levy pre-amendment. (Para 2 , 3 , 4) |

| 2. assessee contests delay and invalid pre-2015 levy. (Para 6 , 7 , 8 , 9) |

| 3. delay condoned for bona fide reasons. (Para 10 , 11) |

| 4. no s.200a power for s.234e levy before 01.06.2015. (Para 12 , 13 , 14 , 15) |

| 5. pre-2015 levies deleted; post-amendment upheld. (Para 16 , 17) |

आदेश/ORDER

PER BENCH:

These bunch of 9 (Nine) appeals of the assessee are filed against the order of the learned Commissioner of Income Tax (Appeals), ADDL/JCIT (A)-4, (NFAC), Delhi, (in short “ld.CIT(A)”) for the assessment year (A.Y.) 2014-15 ( 26Q – Q1, Q2, Q4 and 24Q – Q4), 2015-16 ( 26Q – Q1, Q2, Q3 and Q4) and 2016-17 (26Q – Q1) vide orders in respect of the intimation u/s.200A of the Act passed by the TDS CPC as detailed below :

2. The solitary issue raised by the assessee in all the above appeals is that the levy of late fees u/s.234E of the Act in relation to the quarterly TDS returns for the A.Y.2014-15, 2015-16 & the first quarter of A.Y. 2016-17 is unlawful as the enabling provision u/s.200A of the Act has been introduced only from 01.06.2015.

3. Brief facts of the case emanating from the records are that the assessee is a Company, had belatedly filed its quarterly returns of TDS for A.Y.2014-15 (26Q – Q1, Q2, Q4 and 24Q – Q4), 2015-16 ( 26Q – Q1, Q2, Q3 and Q4) and 2016-17 (26Q – Q1). The CPC – TDS, has processed all the impugned TDS quarterly returns and generated the demand for late fee u/s.234E of the Act, which are prior to 01.06.2015 by passing an order u/s.200A of the Act as detailed supra. Aggrieved, the assessee preferred an appeal before the Ld.CIT(A).

4. At the outset, we observed that the Ld.CIT(A) has dismissed in limine, all the nine appeals filed by the assessee observing that the assessee had filed all these appeals with a huge delay of 8 to 10 years by passing separate orders as per the table given above. Form 26Q for all the 4 quarters of the F.Y.2014-15 have been filed after 01.06.2015 i.e. 27.10.2015 and hence the levy of late fees u/s.234E after processing of the returns by the TDS CPC is in order as per the provisions of section 200A of the Act.

5. Aggrieved by the impugned order of the Ld.CIT(A), the assessee is in appeal before us.

6. The ld.AR submitted that The CPC – TDS, has processed all the impugned TDS quarterly returns and generated the demand for late fee u/s.234E of the Act, which are prior to 01.06.2015 by passing an order u/s.200A of the Act by raising a demand. The ld.AR further submitted that the TDS liabilities have been remitted in full by the assessee. Further, the ld.AR submitted that the late fees has been levied u/s.234E of the Act for belated filing of quarterly returns pertains to the F.Y. 2014-15, 2015-16 & 2016-17 which is leviable only from 01.06.2015 as per the provisions of section 200A r.w.s 234E of the Act.

7. The ld.AR further submitted that the ld.CIT(A) has dismissed all the appeals in limine without condoning the delay in filing the appeal of the assessee. The ld.AR stated that the assessee had given the cause for delay in filing the appeal in form No.35 filed before the ld.CIT(A). The ld.AR explained that, firstly the orders passed u/s.200A were never communicated to the assessee. All the TDS returns of the company had been filed by the Tax consultant and who was maintaining the records and details of updates also. Since these provisions were introduced newly and also the TDS records maintenance and filing were outsourced, the levy of late fees u/s.234E of the Act was not brought to the notice of the company management. The assessee became aware only when the jurisdictional TDS – Assessing Officer served notice of recovery. Immediately, the assessee collected and downloaded all the details of the demand and took action to file the appeals of before the ld.CIT(A). Therefore, the ld.AR submitted that in the interest of substantive justice, the delay may please be condoned and the levy of late fees for bel

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :