INCOME TAX APPELLATE TRIBUNAL (DELHI BENCH)

Anubhav Sharma, Judicial Member, Manish Agarwal, Accountant Member

Kaushalya Gupta – Appellant

Versus

Income Tax Department – Respondent

ITA No.6447/Del/2025|ITA No.6448/Del/2025

| Table of Content |

|---|

| 1. assessee challenges reassessment on limitation grounds for ay 2013-14. (Para 1 , 2 , 3) |

| 2. s.148 notice time-barred beyond surviving 22 tola days post-reply. (Para 4 , 7) |

| 3. high court precedents affirm truncation of s.148a timelines. (Para 5 , 6) |

| 4. reassessment facts and ay 2015-16 reopening challenged. (Para 10 , 11 , 12) |

| 5. revenue concedes dropping ay 2015-16 notices post-april 2021. (Para 13 , 14 , 15) |

| 6. both appeals allowed; reassessments quashed as invalid. (Para 16 , 17 , 18 , 19 , 20) |

ORDER

PER MANISH AGARWAL, AM:

These two appeals are filed by the assessee against the order of Ld. Commissioner of Income Tax (Appeals) National Faceless Appeal Centre (NFAC), Delhi [“CIT(A)”, in short] in Appeal No. NFAC/2012-13/10290290 and NFAC/2014-15/10290307, both dated 12.08.2025 u/s 250 of the Income Tax Act, 1961 (“the Act”) arising out of the orders passed u/s 147 of the Act dated 18.05.2023 and 24.05.2023 for Assessment Years 2013-14 and 2015-16 respectively.

ITA No. 6447/Del/2025 [AY 2013-14]

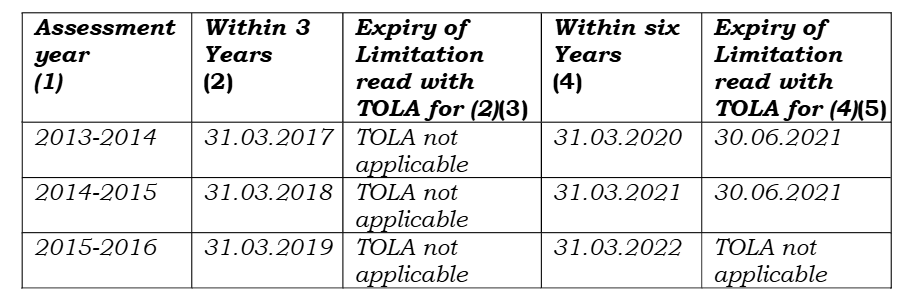

2. First we take appeal filed by the assessee for AY 2013-14 in ITA No. 6447/Del/2025 wherein Ground of appeal No. 1, the assessee has raised legal issue of limitations on account of issue of notice u/s 148 of the Act on 27.07.2022.

3. Heard the parties and perused the material available on record. It is observed that first notice u/s 148 was issued on 08.06.2021. Thereafter, the notice u/s 148A(b) of the Act was issued on 26.05.2022 asking the assessee to file the objections, if any, within a period of two weeks, which expires on 13.06.2022. The assessee had filed reply on 13.06.2022 and the order u/s 148A(d) was passed on 27.07.2022 and thereafter, the notice u/s 148 of the Act was issued on 27.07.2022. The surviving period available with the AO was of 22 days i.e. from 08.06.2021 to 30.06.2021 when the extended time limit under TOLA was expired.

4. The Hon’ble Supreme Court in the case of Union of India & others Vs. Rajeev Bansal reported in (2024) 469 ITR 46, in cases where earlier notice issued u/s 148 were treated as notice u/s 148A(b) of the Act in terms of the order of Hon’ble Supreme Court in the case of Union of India Vs. Ashish Agarwal reported in 444 ITR 1 (SC), has framed a time line for the issue of fresh notice u/s 148 of the Act. The relevant observations are as under:

105. “A direction issued by this Court in the exercise of its jurisdiction under Article 142 is an order of a court. The third proviso to Section 149 of the new regime provides that the period during which the proceedings under Section 148A are stayed by an order or injunction of any court shall be excluded for computation of limitation. During the period from the date of issuance of the deemed notice under Section 148A(b) and the date of the decision of this Court in Ashish Agarwal (supra), the assessing officers were deemed to have been prohibited from passing a reassessment order. Resultantly, the show cause notices were deemed to have been stayed by order of this Court from the date of their issuance (somewhere from 1 April 2021 till 30 June 2021) till the date of decision in Ashish Agarwal (supra), that is, 4 May 2022.

106. In Ashish Agarwal (supra), this Court directed the assessing officers to provide relevant information and materials relied upon by the Revenue to the assesses within thirty days from the date of the judgment. A show cause notice is effectively issued in terms of Section 148A(b) only if it is supplied along with the relevant information and material by the assessing officer. Due to the legal fiction, the assessing officers were deemed to have been inhibited from acting in pursuance of the Section 148A(b) notice till the relevant material was supplied to the assesses. Therefore, the show cause notices were deemed to have been stayed until the assessing officers provided the relevant information or material to the assesses in terms of the direction issued in Ashish Agarwal (supra). To summarize, the combined effect of the legal

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :