IN THE INCOME TAX APPELLATE TRIBUNAL “F” BENCH, MUMBAI BEFORE SHRI SANDEEP SINGH KARHAIL, JUDICIAL MEMBER SHRI BIJAYANANDA PRUSETH, ACCOUNTANT MEMBER ITA No. 1084/Mum./2026 ITA No. 1085/Mum./2026 (Assessment Year : 2013-14) (Assessment Year : 2014-15)

Shankar Rajaram Neelam, Ground Floor, Shop No.12, 160-A Banker Building, Ali Bhai Premji Marg, Grant Road, Mumbai - 400007 ……………. Appellant PAN : ADGPN4469F v/s Income Tax Officer, Ward – 19(3)(1)

Room No.405, Piramal Chambers, Lalbaug, ……………. Respondent Mumbai – 400012 Assessee by : Shri Ravi Sawana Ms. Neha Sharma Ms. Prativa Agarwal Revenue by : Shri Rajesh Sakhardande, SR. DR Date of Hearing – 16/04/2026 Date of Order – 04/05/2026

ORDER

PER SANDEEP SINGH KARHAIL, J.M.

The assessee has filed the present appeals against the separate impugned order of even date 25/11/2025, passed under section 250 of the Income Tax Act, 1961 (“the Act”) by the learned Commissioner of Income Tax (Appeals), National Faceless Appeal Centre, Delhi, [“learned CIT(A)”], inter- alia, for the assessment years 2013-14 and 2014-15.

2. Since in both the appeals the assessee has raised similar issues which arise out of a similar factual matrix, therefore, these appeals were heard together as a matter of convenience, and are being decided by way of this consolidated order. With the consent of the parties, the assessee’s appeal for the assessment year 2013-14 is considered as a lead case, and the decision rendered therein shall apply mutatis mutandis to the other appeal of the assessee before us.

3. In its appeal for the assessment year 2013-14, the assessee has raised the following grounds: –

“Being aggrieved by the order dated 25.11.2025 passed by the Commissioner of Income-lax (Appeals), National Faceless Appeal Centre, Delhi ("CIT(A)"), the Appellant begs to prefer the present appeal on the following grounds which are without prejudice to each other:

1. That in the facts and circumstances of the case and in law, the CIT(A) erred in upholding the addition of Rs. 58,76,810/- made by the Faceless Assessing Officer under Section 69A of the Act, on the ground that the said cash deposits made by the Appellant in its own bank account remained unexplained.

2. That in the facts and circumstances of the case and in law, the CIT(A) erred in upholding the validity of reassessment proceedings, when the same were illegal, invalid, void ab initio and without jurisdiction.

3. That in the facts and circumstances of the case and in law, the notice dated 18.05.2022 deemed to be the show-cause notice under Section 148A(b), the order dated 22.07.2022 under Section 148A(d) and the notice dated 25.07.2022 under Section 148 of the Act, have been issued/passed by the Jurisdictional Assessing Officer and are therefore without jurisdiction in view of Section 151A of the Act read with e-Assessment of Income Escaping Assessment Scheme, 2022.

4. That in the facts and circumstances of the case and in law, the CIT(A) erred in upholding the re-assessment which has been concluded pursuant to the manually issued notice under Section 148 of the Act without any DIN, as the same is contrary to CBDT Circular No. 19 dated 14.08.2019.

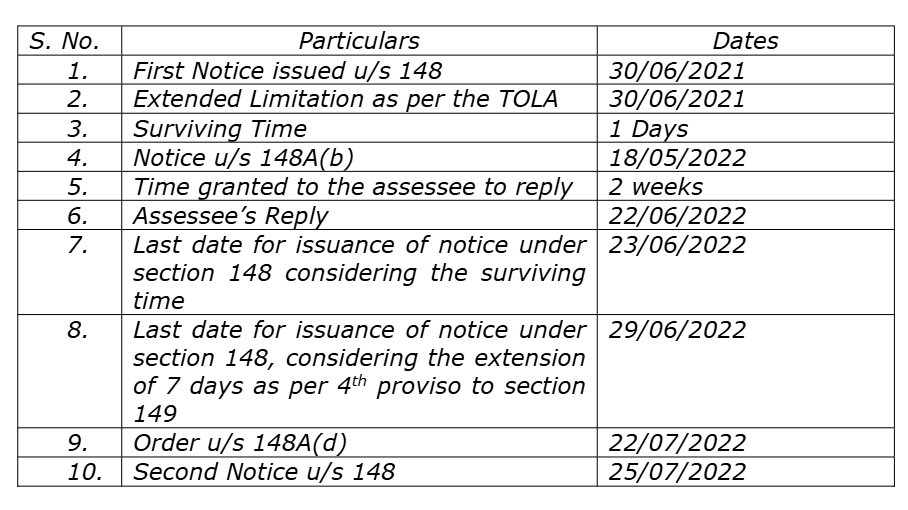

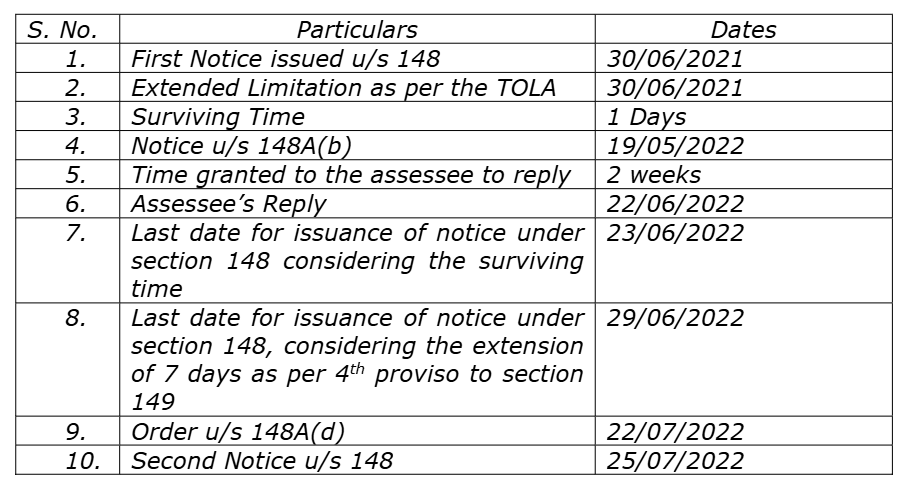

5. That in the facts and circumstances of the case and in law, the CIT(A) erred in holding the re-opening and the re-assessment proceedings to be within limitation, when infact the same are barred by limitation in terms of the first proviso to Section 149(1) (as amended by Finance Act, 2021] read with Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Act, 2020, and much after the surviving period as also held in Hitesh Ramniklal Shah (2025] 180 taxmann.com 642 (Bombay).

6. That in the facts and circumstances of the case and in law, the Jurisdictional Assessing Officer erred in issuing the notice dated 25.07.2022 under Section 148 of the Act basis the "information", being information requiring action in consequence of Ashish Agarwal (SC). which is not an information as per the definition of the same in Explanation 1 to Section 148 of the Act.

7. That in the facts and circumstances of the case and in law, the CIT(A) erred in not adjudicating the ground of appeal raised by the Appellant that the present proceedings could not have been undertaken by way of re- opening since the information was handed over to the Jurisdictional Assessing Officer prior to 01.04.2021.

8. That in the facts and circumstances of the case and in law, the CIT(A) failed to appreciate that the Jurisdictional Assessing Officer deemed the case as fit for re-opening on the ground that the certain sums were credited from society's bank account to the Appellant's bank account, however, there was no credit of funds in

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :