IN THE HIGH COURT OF JUDICATURE AT MADRAS

G. Jayachandran, Shamim Ahmed, JJ.

Commissioner of Income Tax I, Chennai. - Appellant

Versus

M/s.The India Cements Ltd. - Respondent

Tax Case (Appeal).Nos.53 & 54 of 2010

Decided On : 09-04-2026

JUDGMENT :

The respondent herein is a company primarily involved in the manufacturing of cements. The assessment of tax for the Assessment Years 2003-04 and 2004-05 were challenged by the respondent and the same was partly allowed by the Appellate authority. The appeal by the Revenue before the Tribunal was dismissed through a common order. These two Tax Case Appeals filed under Section 260 A of the Income Tax Act by the Revenue against the common order dated 15.07.2009 passed by the ITAT in ITA No:778/Mds/08 and ITA No:779/Mds/08, confirming the order of the Appellate Authority.

2. Brief facts leading to the appeals:

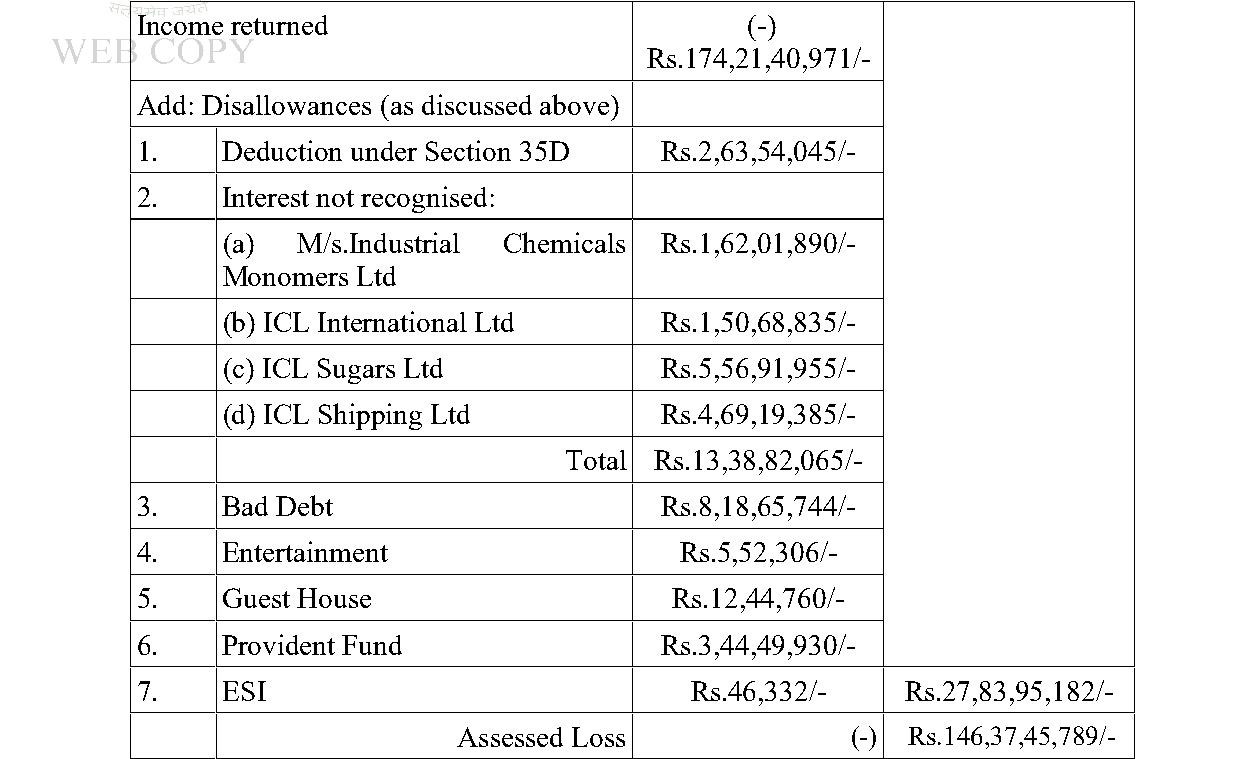

M/s.India Cements Ltd, filed return of income for the Assessment Year 2003-2004, admitting a loss of Rs.174,21,40,971/-. The return was processed under Section 143(1) of the Act. Later, it was taken up for scrutiny after causing notice under Section 143(2). On hearing the assessee, the Assessing Officer passed order on 31.03.2006 computing the income as below:-

Computation of Income

3. Against the above Assessment, the assessee went on appeal before the Commissioner of Income Tax (Appeals), challenging:

(a) The addition of interest accrued on the advances to the subsidiary/associates and charging it to the Profit and Loss Account to an extent of Rs.25,854.20 Lakhs.

(b) The disallowance of the assessee’s claim towards bad debts to an extent of Rs.8,18,65,744/- and;

(c) The disallowance of deduction under Section 35D of a sum of Rs.2,63,54,045/- as debt incurred in respect of debt restructuring exercise.

4. Upon considering the grounds of appeal and hearing the assessee, the Appellate Authority, vide order in ITA No:194/06-07/A-III dated 31.01.2008, partly allowed the assessee’s appeal on the following terms:-

a) Directed the Assessing Officer to delete the additions made on account of interest on the advances to subsidiary/associates, holding that these advances or debit balances are basically the result of commercially expedient action on the part of the assessee and hence, the interest disallowance made by the Assessing Officer are not justified.

b) Directed the Assessing Officer to delete the addition Rs.8,18,65,744/- claimed by the assessee as bad debt. The Appellate Authority held that what is required under the Act is that the assessee, should write off as the bad debt in its books of accounts. In this case, the assessee has done so in consolidated manner during the year under consideration. The write-off is given effect in the account of each individual debtor in subsequent year. When the assessee has debited the amount to the Profit and Loss Account and the contra entry is passed crediting the sundry debtors account in a consolidated manner in the books of accounts of the assessee, the conditions of Section 36(1) (vii) is fulfilled.

c) The claim of deduction of Rs.2,63,54,045/- as expenditure incurred in respect of debt restructuring exercise under Section 35 D disallowed by the Assessing Officer upheld.

5. The Department, being aggrieved by the above order of the Appellate Authority, preferred an Appeal before the ITAT in ITA No:778/Mds/2008 on the ground that, the Appellate Authority had factually erred in holding that the assessee had not made any fresh advances and not charged interest for the reasons of commercial expediency. In fact, the assessee had actually made fresh advances and the subsidiaries were also performing well, as their goodwill had increased substantially. The assessee, in the earlier years, following the Mercantile System of Accounting and Charging Interest on advances to its subsidiaries/associates.

Therefore, the addition made on the interest on advances is correct.

6. The Tribunal, after considering the material available got satisfied that the assessee had commercial angle in its favour behind such advances. Relying on the dictum laid in S.A.Builders Ltd vs. Commissioner of Income-Tax (Appeals), Chandigarh reported in [2007] 288 ITR 1 (SC), it decided in favour of the assessee saying, financial

The Tribunal erred in misapplying legal principles concerning accrued interest on subsidiaries' advances and bad debts, necessitating fresh consideration of the assessment orders as past accounting p....

Notional/hypothetical income like interest on interest-free business advances not taxable; s.14A disallowance impermissible absent exempt income; expense disallowances require proof of non-business n....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :