IN THE HIGH COURT OF JUDICATURE AT MADRAS

G. Jayachandran, Shamim Ahmed, JJ

Cholamandalam Investment & Finance Co., Ltd. – Appellant

Versus

The State of Tamil Nadu, Represented by the Commercial Tax Officer – Respondent

| Table of Content |

|---|

| 1. factual background of assessee's returns and assessments (Para 1 , 2 , 3 , 4 , 5 , 6 , 7 , 8 , 9 , 12 , 18) |

| 2. substantial questions of law admitted (Para 10 , 11) |

| 3. transit sales not exempt under section 6(2) cst (Para 13 , 14 , 15 , 19) |

| 4. high sea sales ineligible under section 5(2) cst (Para 16 , 17 , 40 , 41) |

| 5. state taxing power valid despite constitutional limits (Para 20 , 21 , 22 , 23) |

| 6. definitions of 'sale' include hire-purchase (Para 24 , 25 , 26) |

| 7. constitutional provisions restrict state taxation (Para 27 , 28 , 29 , 30 , 31) |

| 8. dual invoices reveal tax evasion attempt (Para 32 , 33 , 34 , 35 , 38) |

| 9. hire-purchase taxable as first sale in state (Para 36 , 37) |

| 10. revisions dismissed; tribunal findings upheld (Para 39 , 42 , 44 , 45) |

COMMON ORDER

1.M/s.Cholamandalam Investment & Finance Company Limited (hereinafter referred as ‘assessee’) is the revision petitioner in both the Tax Case (Revision) petitions filed under Section 38 of the Tamil Nadu General Sales Tax Act, 1959.

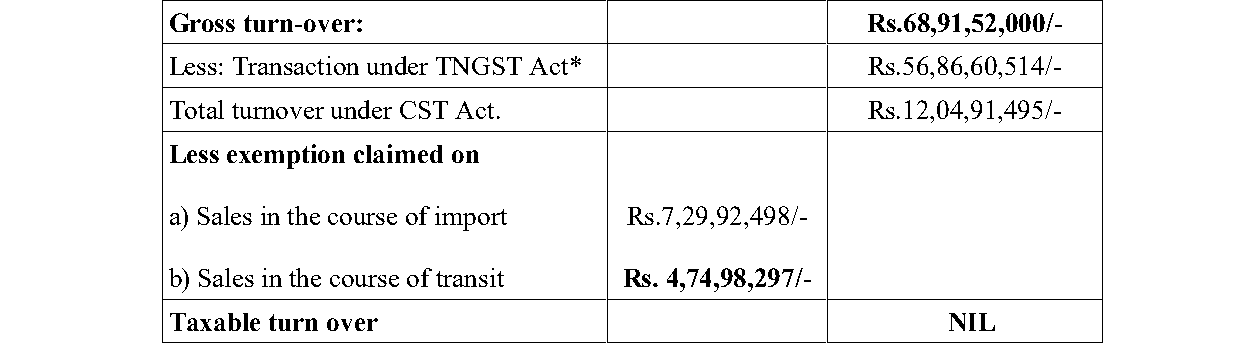

2. The assessee herein filed returns in Form-I filed under GST Act for the year 1995-96 declaring the total turnover as Rs.68,91,52,009/- and its taxable turnover as ‘NIL’ as under:-

*

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :