IN THE HIGH COURT OF JUDICATURE AT MADRAS

G. JAYACHANDRAN, SHAMIM AHMED, JJ.

M/s. Grace Infrastructure Private Limited – Appellant

Versus

State of Tamil Nadu – Respondent

Tax Case (Revision) No. 9 of 2026, C.M.P. No. 7345 of 2026

Decided On : 21-04-2026

| Table of Content |

|---|

| 1. itc reversal for windmill parts used in exempt electricity generation (Para 1 , 9 , 10) |

| 2. high court quashed orders for natural justice violation (Para 2 , 3 , 12 , 13 , 14 , 15) |

| 3. fresh orders defective without considering replies or proper scn (Para 4 , 16 , 18) |

| 4. tribunal remitted for re-appreciation of assessee's replies (Para 5 , 6 , 17) |

| 5. revision allowed; fresh scn barred by limitation (Para 7 , 19 , 23 , 24) |

| 6. itc adjustment valid for old windmill sales, not electricity (Para 20 , 21 , 22) |

ORDER :

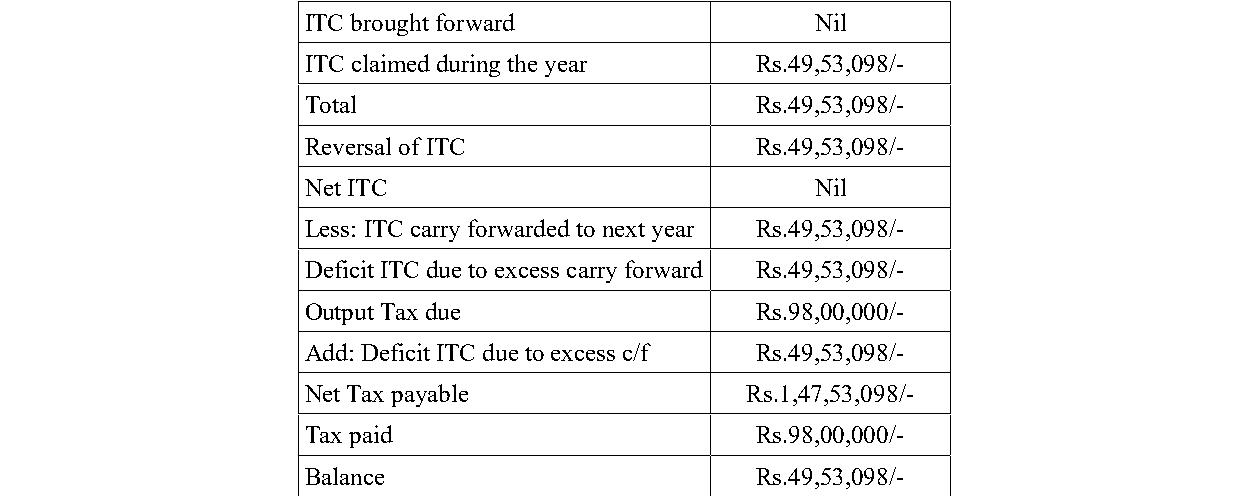

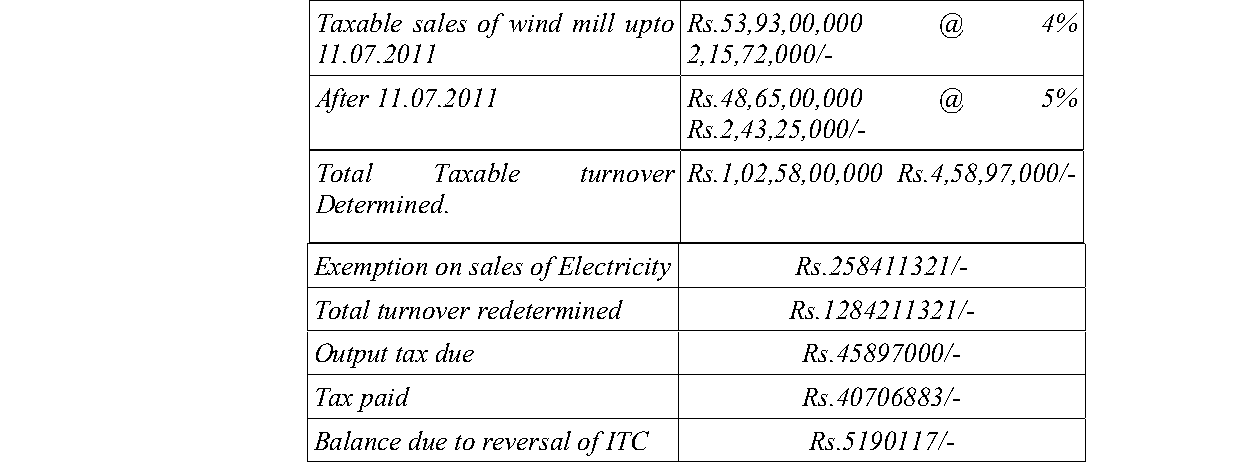

1. The Petitioner herein is a private limited company engaged in the manufacture of wind electric generators and the generation of electricity. It is a ‘dealer’ registered under the TNVAT Act. During the assessment years 2010-2011 and 2011-2012, the Revision Petitioner purchased windmill parts and assembled eight windmills. It also sold ten (10) old windmills that had been purchased prior to the VAT regime. The Input Tax Credit (ITC) availed for purchase of spare parts for assembling windmills were adjusted against the VAT payable for the sale of old windmills. The said ITC claimed by the Revision Petitioner was reversed by the Assessing Officer on the ground that the inputs (spares for windmills) were used exclusively for generating electricity. Since electricity is a commodity exempted from tax, adjustment of ITC is not permissible. Therefore, the State Tax Officer levied tax of Rs.51,90,117/- under Section 27(2) of the Act, along with an equal amount as penalty under Section 27(4)(ii).

2. The reversal of input tax credit was challenged by the Revision Petitioner in W.P.No.8505 of 2017. The writ petition was allowed with a direction to the Assessing Authority for fresh consideration and pass speaking order within a period of three months. The petitioner was given liberty to file an additional representation and participate in the personal hearing.

3. The Assessing Officer completed the assessment and passed fresh assessment order, reiterating the earlier assessment by recording, ‘the dealer (Revision Petitioner) failed to respond in spite of repeated opportunities. The input tax credit claimed by the dealer has to be reversed since the output being electricity, which is exempted under Section 15, being a commodity (Code No:725) covered under Part B/25 of the Fourth Schedule to the TNVAT Act. Accordingly, the input tax credit on purchases relating to windmill machinery is not admissible as per Sections 19(5)(a), 19(6) and 19(12) of the TNVAT Act and the Circular No.41598/2007 (VCC No:1113) dated 28.03.2007. In the fresh assessment order (2011-12) dated 16.08.2024, in addition to the tax and penalty, interest at the rate of 2% per month was levied under Section 42(3) of the Act.

4. Aggrieved by the assessment order dated 16.08.2024, the dealer filed first appeal filed before the Appellate Deputy Commissioner (ST), Cuddalore. The Appellate Authority confirmed the assessment order and dismissed the appeal. The dealer, being aggrieved, challenged the appellate authority’s order before the TNSTAT in T.A.No.10/2025 on the ground that the High Court, in W.P.No.8505 of 2017 by order dated 24.03.2021, remitted the matter to the Assessing Officer with direction to make a fresh assessment after affording an opportunity to the dealer and to pass speaking order within three months. However, the assessment order passed on 16.08.2024 was not a speaking order as directed by the High Court. The fresh assessment order is only a reproduction of the earlier order. The order was conspicuously silent about the reply given by the Trader. Further, the reason stated in assessment order for the reversal of ITC claimed by the dealer is different from the reason stated in the show cause notice for the proposal to reverse the ITC claimed. Without issuing fresh show cause notice, on an entirely new ground, the assessment order was passed in gross violation of natural justice principle. The assessee contended that the observation of the appe

ITC reversal invalid without fresh show cause notice on new grounds; defective notice ignoring nexus to taxable sale cannot sustain assessment; fresh proceedings barred by limitation.

Electricity is not goods taxable under the Kerala Value Added Tax Act. The procedures for rejection of returns and providing an opportunity to produce documents and accounts should be exhausted befor....

Point of law: A reasonable opportunity is liable to be granted to the dealer to enable him to appear before the authority concerned and show cause against the proposal to complete the assessment on b....

Rule 6(3A) CENVAT reversal limited to common credit; excludes exclusive dutiable credit; no extended period or penalty for interpretational disputes.

The entitlement to Cenvat credit for service tax on installation and maintenance of windmills is upheld, emphasizing that location does not negate its admissibility as an input service in manufacturi....

The main legal point established in the judgment is the distinction between exempted goods and exempted transactions under the Tamil Nadu Value Added Tax Act, 2006, and the inapplicability of Section....

The court affirmed that a timely application under Section 84 of the TNVAT Act, 2006 can be considered despite prior delays in appeals, especially when merits are supported by established legal prece....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :