PATNA HIGH COURT

HONOURABLE MR. CHANDRA SHEKHAR JHA, J

AMITABH KUMAR – Appellant

Versus

THE STATE OF BIHAR THROUGH ECONOMIC OFFENCE UNIT, PATNA BIHAR – Respondent

CRIMINAL MISCELLANEOUS No.49461 of 2023 | Special Case No. 353 of 2017 | EOU P.S. Case No. 17 of 2017

| Table of Content |

|---|

| 1. presentation of case and background facts. (Para 1 , 2 , 3) |

| 2. arguments by petitioner highlighting flaws in prosecution. (Para 4 , 5 , 6 , 7 , 8 , 9 , 10 , 11 , 12) |

| 3. arguments by e.o.u. regarding basis for arrest. (Para 13 , 14 , 15 , 16 , 17 , 18) |

| 4. counterarguments and case law regarding the validity of prosecution. (Para 19 , 20 , 21 , 22) |

| 5. judicial determination of issues surrounding exoneration. (Para 23 , 24 , 25 , 26 , 27 , 28 , 29 , 30 , 31 , 32 , 34) |

| 6. analysis of departmental proceedings concerning criminal prosecution. (Para 35 , 36 , 37 , 38) |

| 7. final decision on the petition for quashing. (Para 39 , 40 , 41) |

CAV JUDGMENT

Date : 14-07-2025

Heard learned senior counsel for the petitioner and learned counsel for the respondents.

2. The present petition has been preferred under Section 482 of the Code of Criminal Procedure (in short Cr.P.C.) to quash the order dated 17.03.2023 passed in Special Case No. 353 of 2017, arising out of EOU P.S. Case No. 17 of 2017, where learned Special Judge Vigilance, Patna, took cognizance for the offence punishable under Section 13 (1)(e) of the Prevention of Corruption Act, 1988 .

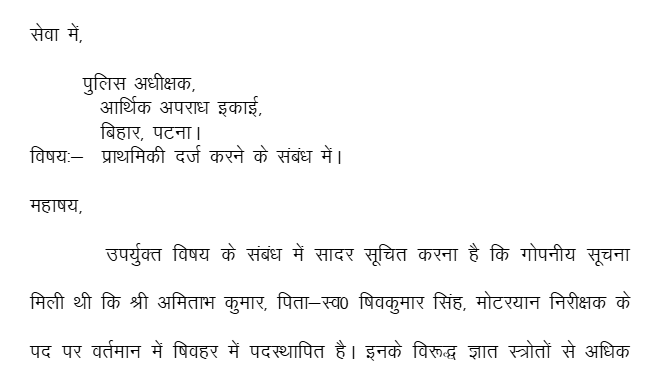

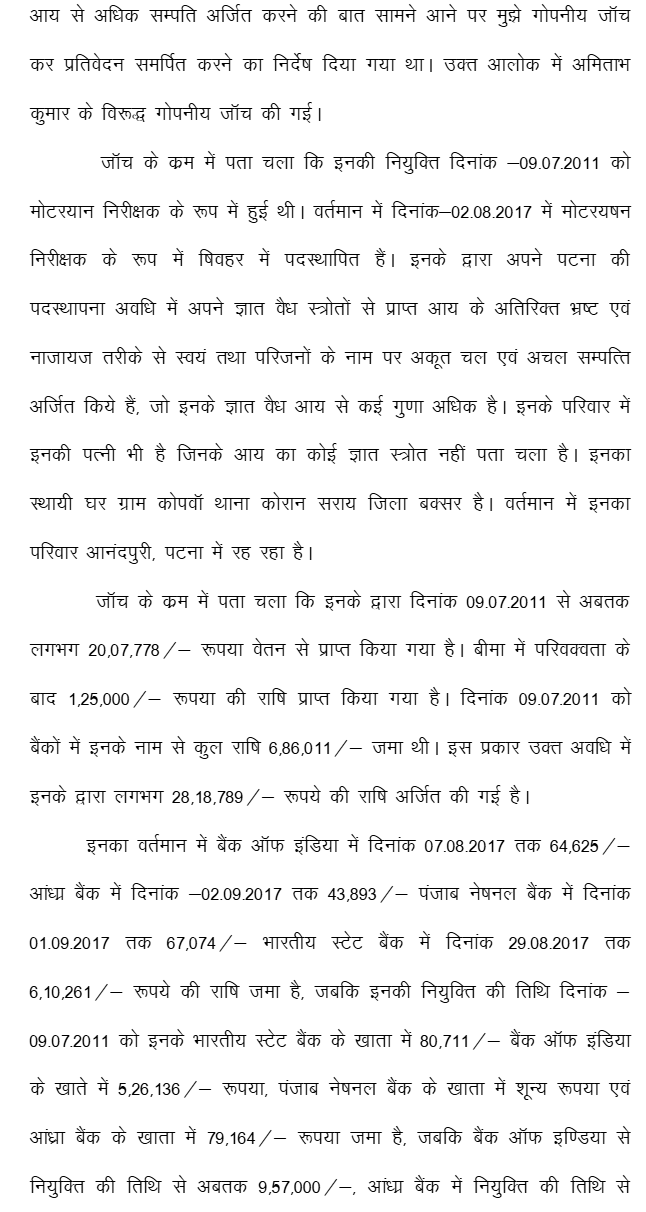

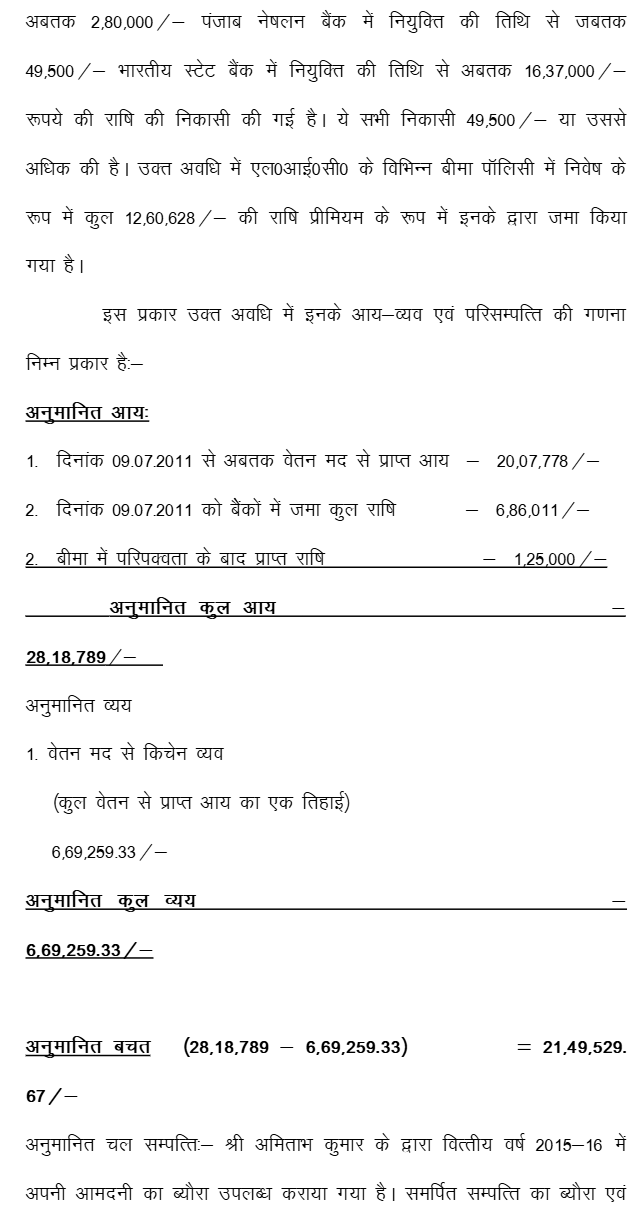

3. The prosecution story as it appears from the written report of Dy.S.P cum Investigating Officer, Economic Offence Unit, Patna, is that upon secret information received by the informant, it came to light that petitioner Amitabh Kumar, who is at present a Motor Vehicle Inspector (in short MVI) and posted at Shoehar, has embezzled huge amounts of money and assets illegally by misusing his post and power, when he was posted as MVI in Patna. The investigating period (check period) of this case is from 09.07.2011 to 17.11.2017. It is further alleged that, during the course of prima-facie investigation, the informant discovered that the total legitimate income of the petitioner, Amitabh Kumar, amounted to Rs. 28,18,789/-, whereas his total expenditure was assessed at Rs. 6,69,259/-. It has also been alleged in the FIR that the cumulative value of his movable and immovable assets stood at Rs. 49,69,981/-. It was further alleged in the FIR that during the tenure of his services from 09.07.2011 to 17.11.2017, he was involved in illegal means and practices to acquire assets disproportionately to their valid sources of income to the tune of Rs. 28,20,451/-. Consequently, the present case was instituted.

Argument on behalf of petitioner

4. Mr. Y.V. Giri, learned senior counsel, appearing on behalf of the petitioner submitted that the prosecution filed the FIR without conducting any preliminary inquiry, and if the Economic Offences Unit (EOU) had conducted such an inquiry, it would have been evident that no Disproportionate Assets (DA) case was made out against the petitioner. It is also submitted that the FIR appears to be lodged falsely to justify the prosecution's actions and to shield their misconduct, resulting in charge-sheet submission without material evidence. It is also submitted that the petitioner was unnecessarily implicated, and the investigation was not conducted properly. The Investigating Officer (I.O.) ignored several key facts that would have established the petitioner’s innocence. It is submitted that income from valid sources, including the petitioner’s and his wife’s earnings, was also not adequately considered.

5. Mr. Giri, further submitted that I.O. incorrectly calculated the petitioner’s income as only Rs. 33,15,293/-, whereas the petitioner had earned Rs. 46,10,409/- from salary, rental, and agricultural sources, as evident from his income tax returns. Similarly, the I.O. deliberately excluded the documented income of the petitioner’s wife. It is further submitted that the prosecution wrongly considered household goods and ancestral ornaments from the petitioner’s house as self-acquired property. However, no immovable property was acquired by the petitioner or his wife during the check period, and all assets were ancestral and jointly held by family. It is submitted that the pe

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :