IN THE HIGH COURT OF KARNATAKA AT BENGALURU

S.R.KRISHNA KUMAR

Bhandary Gas Agency, Represented By Proprietor, Manjunath Bhandary – Appellant

Versus

Joint Commissioner Of Commercial Taxes, DGSTO, Malnad Division, Shivamogga – Respondent

| Table of Content |

|---|

| 1. petitioner seeks relief against gst assessment. (Para 1 , 2) |

| 2. arguments regarding residential dwelling definition. (Para 6 , 7) |

ORDER :

S.R. KRISHNA KUMAR, J.

In this petition, petitioner seeks for the following reliefs:-

“a) Issue a Writ of Certiorari or any direction to quash and set aside the order bearing No.ZD2901240163160 dated: 10.01.2024 under S.107 of the KARNATAKA GOODS AND SERVICES TAX ACT , vide Annexure-A as it is without jurisdiction , arbitrary , void and illegal.

b) Issue a Writ of mandamus or any direction allowing the application dated: 26.09.2022 vide Annexure-G.

c) Issue a Writ of Mandamus or direction to the Respondent No.2 refund the amount of Rs.62,50,716/- along with interest paid by the petitioner under protest.

d) Declare the act of Respondent Authorities of issuing the impugned order vide Annexure-A is arbitrary and bad in the eyes of law.

e) Any other relief/s as this Hon’ble Court deems fit in the interest of justice and equity.”

2. A perusal of the material on record will indicate that on 02.08.2022, the 2nd respondent conducted an audit and prepared a report under Section 65(6) of the GST Act, 2017 and included the rent received from the

The court held that leasing residential premises for student accommodation qualifies for GST exemption, underpinning strict interpretation of exemption notifications in favor of the taxpayer.

Hostel services provided for residential purposes qualify for GST exemption under relevant notifications, emphasizing the interpretation of exemption notifications should favor the taxpayer.

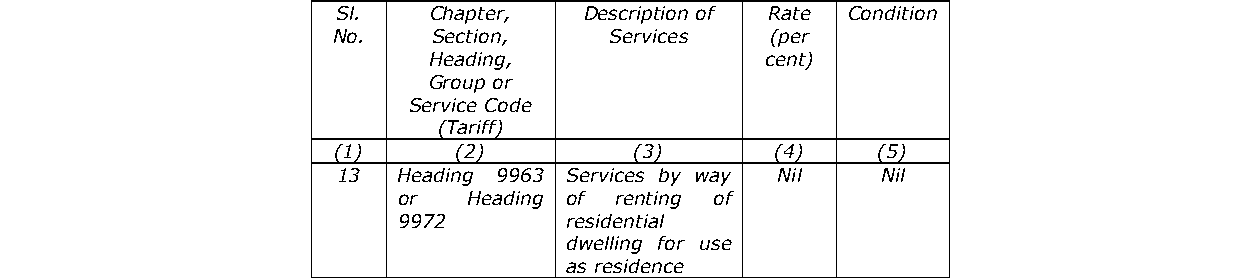

Point of Law : Benefit of exemption notification cannot be denied to the petitioner on the ground that the lessee is not using the premises.

The court affirmed that leasing of premises as a hostel for students constitutes a residential dwelling under GST law, qualifying for tax exemption regardless of the lessee's use.

It is well settled that rights of parties will have to be determined on basis of rights available to them on date of suit.

The court ruled that acknowledgment of rent exceeding statutory thresholds affirms jurisdiction under the Transfer of Property Act, negating claims under the Karnataka Rent Act.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :