K. R. SHRIRAM, JITENDRA JAIN

Film & Television Producers Guild of India (Fpgi) G-1 – Appellant

Versus

State of Maharashtra – Respondent

ORAL JUDGMENT

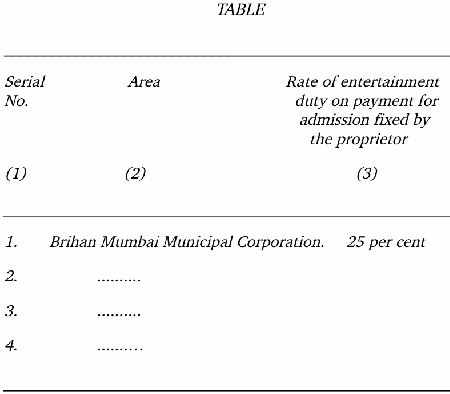

Jitendra Jain, J. - By this petition under Article 226 of the Constitution of India, petitioner seeks to challenge an order dated 28th September 2007 by which the Appellate Authority has confirmed the demand of entertainment duty of Rs. 71,87,500/- and reduced the penalty from Rs.1,43,75,000/- to Rs. 71,87,500/-.

:Brief facts:

2. Petitioner is a company incorporated under Section 25 of the Companies Act, 1956 and engaged in the activities of promoting Indian Cinema and Television in India and Worldwide.

3. On 21st January 2006, petitioner organised 'APSARA' award function at Jamshedji Bhabha Auditorium for felicitating distinctive achievements in cinema and television. The said function was organised in association with Speed Bright, Sony TV, NDTV, Hungama Events, and Reliance Communications etc.

4. Reliance Communications, vide letter dated 29th December 2005, informed Respondents that they had entered into an agreement with petitioner for sponsorship containing details of offer and monetary value in relation to the said award function. The total monetary value worked out to Rs. 4.90 crores which was attributable to Free Commercial Time on NDTV channels, Press Advertiseme

The definitions of 'entertainment' and 'payment for admission' under the Maharashtra Entertainments Duty Act are broad enough to encompass award functions and sponsorship amounts, while penalties mus....

The judgment established the applicability of entertainment tax based on the nature of the activities and the public's access to them, as interpreted in various decisions.

The charge for admission must be uniformly and mandatorily applicable to all attendees to constitute 'payment for admission' under the relevant legal provisions.

The main legal point established in the judgment is that the petitioners' water sports activities were liable for entertainment duty under the Bombay Entertainment Duty Act, and their claim for refun....

The court upheld the constitutionality of the cess levied on cinema tickets, affirming the State's legislative competence under Entry 62 of List II, Schedule VII of the Constitution, linking it to th....

Entertainment tax subsidies granted as incentives for constructing cinema infrastructure are capital receipts and do not reduce the cost of assets for depreciation purposess, provided they are not li....

Local authorities must comply with government exemption orders under the Kerala Local Authorities Entertainments Tax Act, and cannot impose additional conditions for tax refunds.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :