IN THE HIGH COURT OF JUDICATURE AT BOMBAY

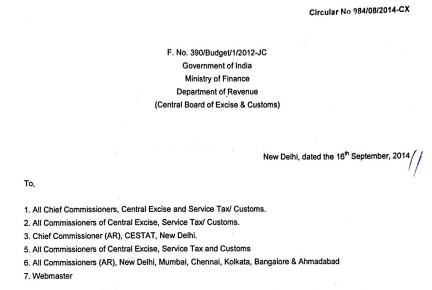

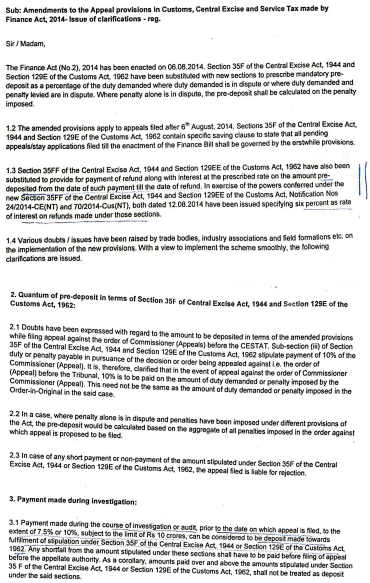

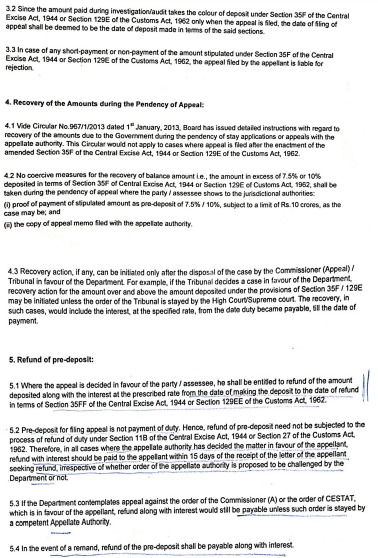

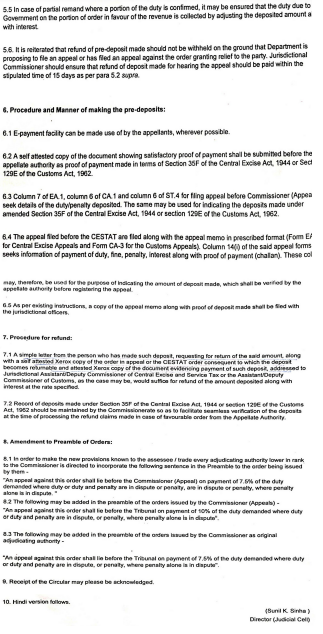

K.R. SHRIRAM, JITENDRA JAIN, JJ.

Ramkaran Karwa – Petitioner

Versus

Union of India, through the Secretary, New Delhi – Respondent

Writ Petition No. 12299 of 2024, Writ Petition (Stamp) No. 26523 of 2024

Decided On : 20-09-2024

Interest - Refund of Seized Cash - Central Excise Act, 1944, Section 35FF - Customs Act, Section 129EE - The court interpreted the applicability of interest rates on refunds, emphasizing that the Respondents unjustly enriched themselves by retaining interest earned on seized cash, which was held in trust.

Fact of the Case:

The Petitioner sought to quash an order granting interest at 6% on refunded seized cash, arguing for 18% based on the cash's fixed deposit earnings. The cash was seized during an investigation against a company where the Petitioner was a director.

Finding of the Court:

The court found that the Respondents' reliance on a circular to justify 6% interest was misplaced, as the cash was not a pre-deposit for appeal but held in trust. The Petitioner was entitled to the actual interest earned on the fixed deposit.

Issues: Whether the Respondents were justified in granting interest at 6% per annum on the refund of seized cash, despite the cash being placed in a fixed deposit earning a higher interest rate.

Ratio Decidendi: The court held that the Respondents, as trustees of the seized cash, could not unjustly enrich themselves by retaining interest earned on the cash, which was held in trust for the Petitioner.

Result: The court quashed the impugned order and directed the Respondents to refund the Petitioner the excess interest earned on the fixed deposit.

JUDGMENT :

JITENDRA JAIN, J.

1. Rule. By consent of the parties heard finally since the pleadings were completed.

2. Writ Petition (Stamp) No. 26523 of 2024 not on board, but by consent of the parties is taken up for hearing alongwith the present writ petition since the issue involved is common. However, in the present order, facts relating to Writ Petition No. 12299 of 2024 are narrated for sake of convenience.

3. By this petition under Article 226 of the Constitution of India, Petitioner is seeking for quashing of Order-in-Original (O-I-O) dated 5th July 2024 whereby Respondents have granted interest @ 6% per annum on the amount refunded to Petitioner by rejecting the claim of Petitioner to grant interest @ 18% per annum.

Brief undisputed and admitted facts are as under:

4. On 29th August 2011, an investigation was initiated by Respondent No. 4 against one Perfect Containers Pvt. Ltd. In the course of the investigation, Petitioner’s residence premises were searched and a sum of Rs.2,06,33,000/- was seized on the allegation that same constitutes unaccounted receipts arising out of sales made by Perfect Containers Pvt. Ltd. In the course of said investigation Rs.15,94,000/- was also seized from the residence of Petitioner’s son. The aggregate cash seized was Rs.2,22,27,008/-. The seized amount was deposited by Respondent No. 4 in fixed deposit with Punjab & Sind Bank.

5. On 19th May 2016, O-I-O was passed against Perfect Containers Pvt. Ltd., Petitioner and others whereby it was held that cash seized was towards sale proceeds of clandestinely removed goods and therefore the said cash was liable for confiscation. Penalty of Rs.21,25,199/- under Rule 26 of the Central Excise Rules was also imposed on Petitioner. Against the said O-I-O Petitioner and Respondents filed cross-appeals before Commissioner of Central Excise (Appeals).

6. On 31st March 2017, the first appellate authority set aside the order of confiscation of cash seized and penalty imposed on Petitioner. The said order was challenged by Respondents by filing an appeal with the Tribunal. The Tribunal, vide its order dated 18th October 2023, upheld the first appellate authority’s order of setting aside the confiscation of cash seized and penalty imposed on Petitioner. The said order of the Tribunal has attained finality. However, inspite of the order of both the appellate authorities being in favour of Petitioner and inspite of there being no stay on any of the appellate order and inspite of Petitioner’s request for refund vide various letters, Petitioner was not granted refund of the cash seized of Rs.2,06,33,000/-. So also Petitioner’s son was not given refund of Rs.15,94,000/-. Petitioner’s son has filed a separate writ petition being Writ Petition (Stamp) No. 26523 of 2024.

7. On 21st May 2018, Respondent No. 4 refused to grant the refund on the ground that the matter is pending before the Tribunal. The refusal was challenged by filing an appeal with the Commissioner GST & CX (Appeals) who, vide order dated 23rd January 2019, directed Respondents to process the claim of refund since there was no stay on the appellate order.

8. Meanwhile, on 2nd May 2019 Respondent No. 4 informed Respondent Nos. 2 and 3 that the seized currency was placed in fixed deposit with Punjab & Sind Bank. The said fact is also recorded in the impugned order dated 5th July 2024 and in the Affidavit in Reply of Respondent Nos. 1 to 3 affirmed by Manjula Arulselvan on 9th September 2023.

9. On 26th December 2023, 22nd February 2024 and 10th April 2024, Petitioner requested for refund of Rs.2,06,33,000/- along with interest @18% per annum.

10. Since Respondents were not granting refund of cash seized a Miscellaneous Application was filed before the Tribunal praying for refund of cash seized along with interest @18% per annum. Pending the Miscellaneous Application, impugned O-I-O dated 5th July 2024 came to be passed ordering return of seized cash of Rs.2,06,33,000/- along with interest @ 6% from the date of

Trustees cannot retain interest earned on funds held in trust; they must account for all earnings to the beneficiary.

The court established that interest on delayed refunds of pre-deposits can be claimed at 12% per annum based on judicial precedents, despite the absence of a specific statutory provision at the time.

Deposits made at departmental insistence during investigation under mistaken duty notion are not 'duty' under Section 11B; refundable with 12% interest from deposit to refund date.

Deposits made during investigation at department's insistence under mistaken duty notion are not 'duty'; Section 11B inapplicable; refundable with 12% interest from deposit to refund date.

Interest on delayed refunds under Section 11BB of the Central Excise Act is payable only after three months from the date of receipt of the refund application, not from the date of deposit.

There is always peril in treating the words of a speech or judgment as though they are words in a legislative enactment, and it is to be remembered that judicial utterances made in the setting of the....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :