IN THE HIGH COURT OF BOMBAY AT GOA

BHARATI DANGRE, NIVEDITA P. MEHTA, JJ.

M/s. Colorcon Asia Pvt. Ltd., Through Authorized Representative Mr. Vinay Potdar – Appellant

Versus

The Joint Commissioner of Income Tax, Special Range Aayakar Bhawan, Patto, Panji and Ors. – Respondents

Tax Appeal No.5 of 2024

Decided On : 28-11-2025

JUDGMENT :

BHARATI DANGRE, J.

1 M/s. Colorcon Asia Pvt. Limited, a Private Limited Company, incorporated under the Companies Act, 1956 and wholly owned subsidiary of Colorcon Limited, United Kingdom (Colorcon UK) , engaged in the business of manufacturing, supply and technical support of formulated film, coating systems, modified release technologies, and functional excipients for the pharmaceutical industry, has filed the present Appeal under Section 245(w) of the INCOME TAX ACT , 1961 (for short “Act”), to assail the ruling dated 27/06/2024 (impugned ruling) passed by the Board for Advanced Rulings - I, New Delhi ( in short “BFAR”) in Unique No. of the case : AAACC2281Q/2019/0020/0306 (Old No.L AAR/446/2019). The impugned ruling according to the Appellant has erroneously decided against the questions raised by it seeking an advance ruling to restrict the rate of Dividend Distribution Tax (DDT) to the extent of withholding tax rate on Dividend Income as prescribed under Article 11 of India - UK Tax Treary ( DTAA).

A : THE CHALLENGE IN THE APPEAL

2 The brief background in which the challenge is raised is set out in the Appeal and is also presented before us by the learned Senior Advocate Mr. Porus Kaka, assisted by Mr. Manish Kanth, and in a brief manner, we would refer to the same.

a) Colorcon UK is a foreign company formed and registered under the laws of United Kingdom, having its registered office at Flagship House, Victory Way Crossways, Dartford Kent, DA2 6QD, United Kingdom and it is not an Indian company within the meaning of section 2(26) of the Act. It is a tax resident of United Kingdom with a valid Tax Residency Certificate issued by the Government of United Kingdom.

b) During AYs 2016-17, 2017-18, and 2018-19, the Appellant has paid dividend to Colorcon UK and also paid DDT thereon at the rate specified under Section 115-O of the Act. The Appellant also paid interim dividend for AY 2019-20.

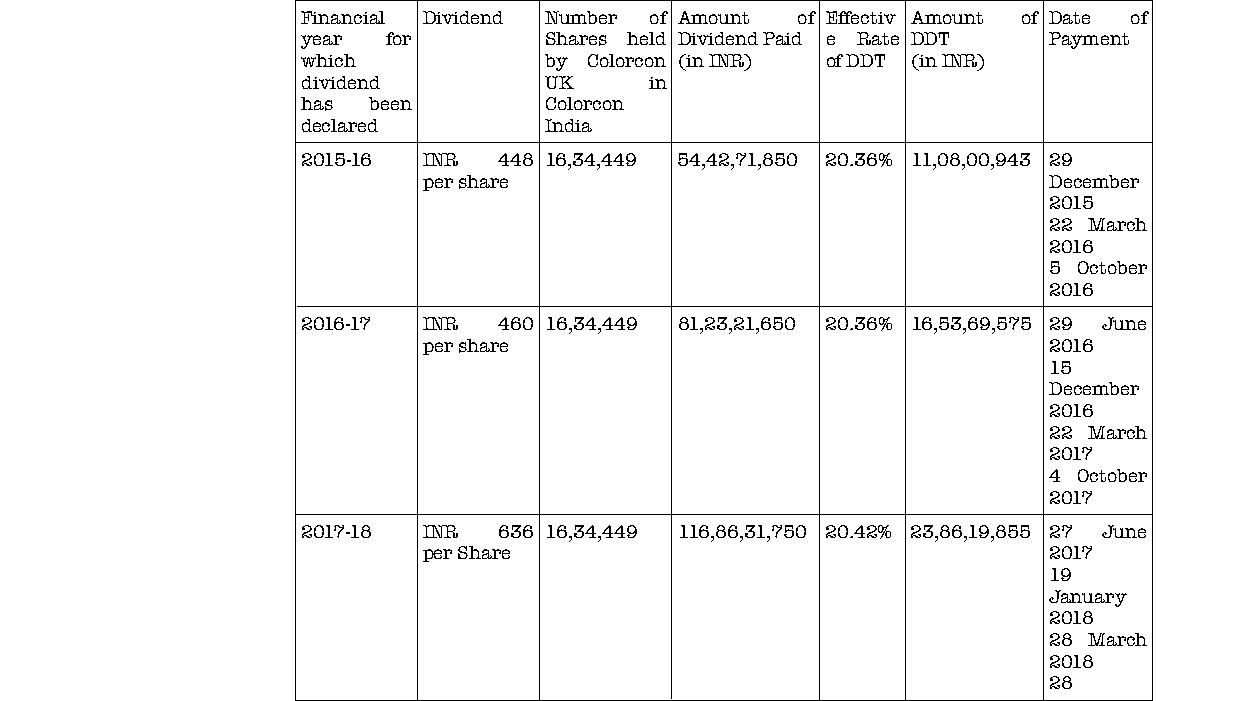

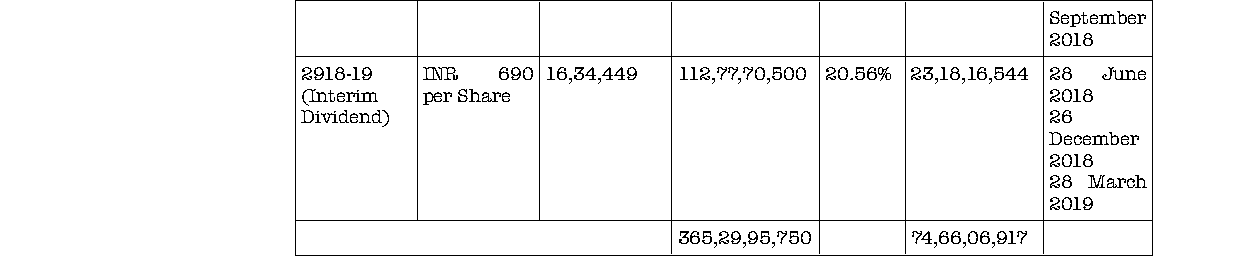

c) The Appeal has set out the details of the dividend paid by the Appellant and the effective rate of DDT to the following effect :

d) The Appellant having made the cumulative dividend pay out in excess of INR 100 crores, filed an application under Section 245Q of the Act on 20/05/2019 seeking an advance ruling on the following questions before BFAR :

1) On the facts and circumstances of the case and in law, whether Colorcon Asia Private Limited (‘Colorcon India’ or ‘the Applicant’ or ‘Company’) would be entitled to restrict the tax rate on dividends distributed or distributable by it to Colorcon Limited, United Kingdom UK), at 10 per cent under Article 11 (Dividends) of the India-UK Tax Treaty (“Tax Treaty”).

2) If answer to question no.(1) is in the affirmative, whether in the facts and circumstances of the case and in law, the tax rate of 10 per cent under the Tax Treaty needs to be further grossed-up.

The above application for advance ruling was admitted under section 245R(2) of the Act, vide its order dated 18/11/2019.

3 The hearing was scheduled before the BFAR and the Appellant was directed to file written submissions incorporating its propositions on question under consideration and the Appellant complied with the said direction. Similarly, the Respondent also filed its report under Section 245 R (4) of the Act on 16/01/2020, wherein it specifically pleaded that the Appellant did not satisfy the conditions of Paragraph 1 and 2 of Article 11 of India – UK DTAA and, therefore, it is not eligible to apply the rate of 10% to DDT on the amount of dividends paid to Colorcon, UK.

The Appellant clarified that the dividend as provided in application is on the basis of the financial year for which the dividend was declared irrespective of the time when such dividend was declared by the Appellant and it also furnished the updated data of dividend declared and DDT paid basis as against the financial year in which the dividend was declared to align the amounts of dividends declared and paid with the Income Tax Returns (ITRS). The following detai

Dividend Distribution Tax is a tax on dividend income and is covered by the DTAA, allowing a maximum tax rate of 10% on such dividends.

DDT is tax on shareholders' dividend income collected from company; DTAA lower rates cap DDT liability under section 90(2), enabling refund of excess to paying company.

Division Bench refers to Larger Bench whether DDT on dividends to non-residents is capped by DTAA Article 11 or remains company's additional tax on profits per Section 115-O, due to conflict with pri....

DDT on dividends to non-resident shareholders under India-UK DTAA restricted to 10%; excess refundable as it constitutes tax on dividend income. No interest u/s 234B/C on unforeseeable APA incrementa....

DDT on dividends to non-residents restricted to DTAA rate (10%) as it is tax on shareholder's dividend income; prevails over domestic law. Management fees ALP restored for fresh consideration of evid....

The protocol in the DTAA allows for the automatic applicability of lower withholding tax rates based on other treaties, requiring consistent interpretation for equitable tax allocation between contra....

Point of Law : Taxation - Issuance of a certificate at a lower withholding tax rate – While interpreting international treaties including Tax treaties rules of interpretation that apply to domestic o....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :