IN THE HIGH COURT OF JUDICATURE AT BOMBAY

S.M.Modak

Vilas Babanrao Kalokhe – Appellant

Versus

Principal Commissioner of Income Tax (Central) Pune – Respondent

| Table of Content |

|---|

| 1. issue of invoking writ jurisdiction. (Para 1) |

| 2. details of tax payment and complaint. (Para 2 , 3 , 4 , 5 , 7) |

| 3. submissions of parties regarding willful default. (Para 8 , 9) |

| 4. acknowledgment of tax liability and return submission. (Para 10 , 11) |

| 5. nature of offenses under income tax act. (Para 12 , 13 , 14) |

| 6. differentiation between failure and evasion of tax. (Para 15 , 16 , 18 , 19) |

| 7. conclusion regarding prosecution and quashing of order. (Para 20 , 21 , 22) |

JUDGMENT :

S. M. Modak, J.

1. The only issue arisen in this Petition is whether ingredients of Section 276 C (2) of Income Tax Act are made out and whether Writ Jurisdiction under Article 227 of the Constitution can be invoked.

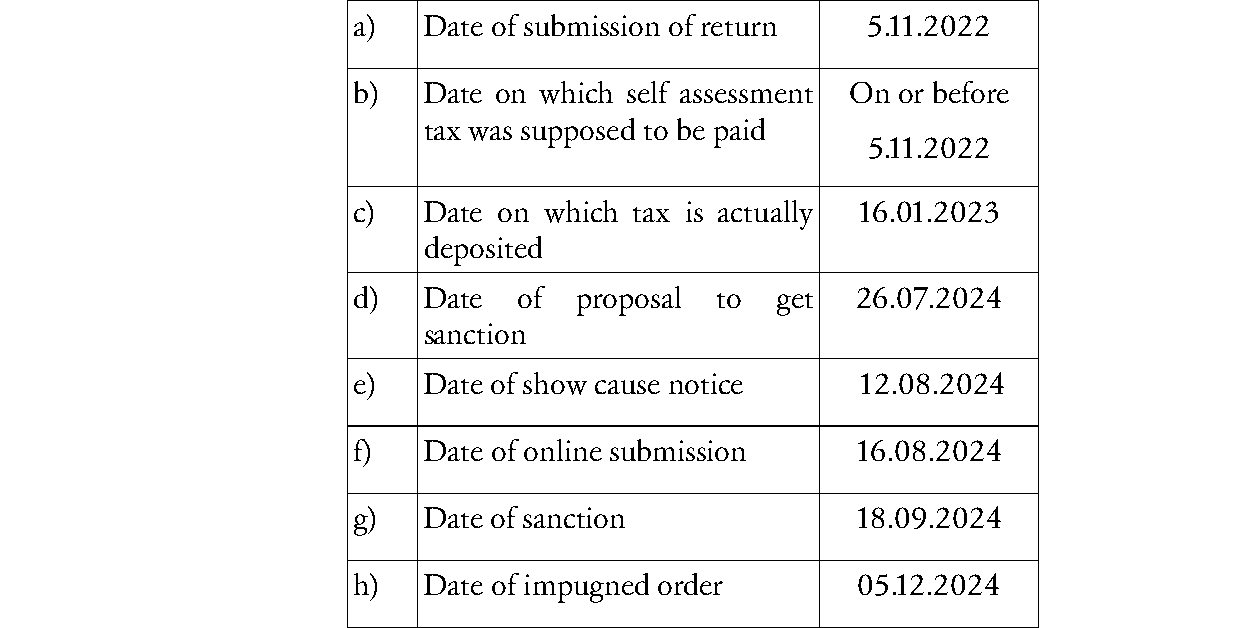

2. The Complainant Income Tax Department contends that, along with the Return of Income / at the time of submitting Return of Income, the assessee / accused / petitioner has not deposited the amount of Income Tax which is due as per his calculation. They further contend that, even subsequently, he has not deposited it.

3. That is why, not only there is a default but also there is a willful default as contemplated as per the provision of 276 C (2) of the said Act.

4. As against this, it

Willful default in tax payment under Section 276 C (2) requires proof of intentional evasion; mere delay, along with demonstrated financial difficulties, does not suffice for prosecution.

object of launching criminal prosecution for wilful default in complying with the provisions of the Income Tax Act is to prevent evasion of tax

The main legal point established is that the failure to remit tax, without evidence of a wilful attempt to evade tax, does not constitute an offence under Section 276 C (2) of the Income Tax Act.

Delayed payment of income tax does not constitute tax evasion under Section 276C of the Income Tax Act, requiring evidence of willful intent to evade tax for prosecution.

It is not the case of the Income Tax department that the self assessment tax returns which were filed had an element of concealment on any factual aspects and tried to evade tax, which is liable to p....

The main legal point established in the judgment is the significance of timely filing of the Return of Income, the consequences of wilful attempt to evade tax, penalty, and interest chargeable, and t....

The rule of evidence under Section 278 E of the Act regarding rebuttable presumption as to existence of culpable mental state on the part of accused would come into play. As such there is no scope fo....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :