IN THE HIGH COURT AT CALCUTTA

SHAMPA SARKAR, J.

SK. Abdul Sabir & Associates - Petitioner

Versus

The State Of West Bengal & Ors. – Respondents

W.P.A No. 2966 of 2024

Decided On : 09-02-2026

JUDGMENT :

Shampa Sarkar, J.

1. The question before this court is whether the instrument which has been styled as the Memorandum of Understanding (MOU) and which was tendered as an exhibit by the writ petitioner in Title Suit No. 70 of 2011, also dealt with transfer of landed property and whether the stamp duty assessed by the respondents was correct.

2. The order dated July 31, 2023, bearing number 1297-FT/O/IN-05/20 issued by the Additional Chief Secretary to the Government of West Bengal and Chief Controlling Revenue Authority Government of West Bengal, passed in a reference under Section 56 of the Indian Stamp Act 1899 and the consequent order dated September 7, 2023, passed by the District Magistrate Hooghly, are under challenge before this court.

3. The facts narrated in the writ petition are discussed in a nutshell:-

(a) The petitioner is a partnership firm constituted under the Partnership Act 1932. One M/s Nirmal and Navin Private Limited (hereinafter referred to as the ‘company’) had availed of credit facilities for the purpose of its cold storage business to the tune of Rs 6.10 crores from Hooghly District Central Co-operative Bank. The company approached the petitioner for financial help as it was allegedly struggling to repay the loan.

(b) The petitioner agreed to take care of the financial liability of the company and the personal guarantee of its directors. Pursuant thereto, the MOU was executed on January 27, 2009. The petitioner was represented by Sheikh Abdul Sabir and one Mr. Gopal Agarwal represented the company. The MOU was executed with the objective of transferring control of the company and the right to manage and operate the cold storage. Clauses 2 and 4 of the MOU would indicate that a sum of Rs 5 lakhs was paid by the petitioner to Gopal Agarwal and his wife (both directors) as a consideration for transfer of the entire shareholding in the company. Consequently, the petitioner was inducted as a director in the company. On and from January 28, 2009, the petitioner had been looking after the management and operation of the cold storage unit and also clearing the loans obtained by the company from the bank. On July 18, 2011, Gopal Agarwal refused to act in terms of the MOU and Title Suit No. 70 of 2011 was filed before the Learned Civil Judge, Junior Division, 2nd Court, Arambagh, Hooghly. The petitioner as plaintiff prayed for an order of injunction restraining Mr. Gopal Agarwal from entering into the premises of the cold storage without permission and for a permanent injunction restraining Gopal Agarwal from interfering with the running of the cold storage.

(c) The application for temporary injunction was disposed of by the learned Civil Court, restraining the defendant from entering into the property without permission of the petitioner. The said order was challenged in a Misc. appeal which was registered as Misc. appeal No.13 of 2011 by Gopal. The appellate court was of the view that Gopal should not be restrained by an order of injunction from entering into the property, and as such, the order of injunction was modified by passing an order of status quo in respect of the property, till the disposal of the suit. The said order was challenged before the High Court in CO No.- 55 of 2011.The order of the learned appellate court was not interfered with by the High Court.

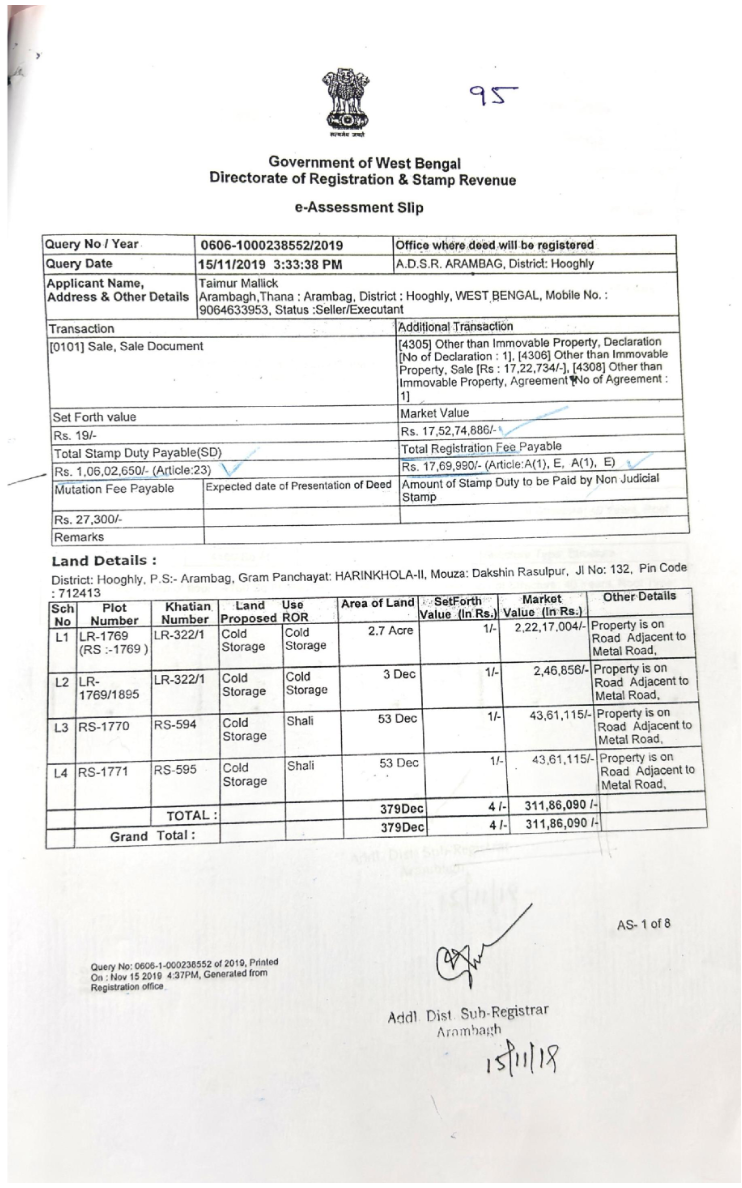

(d) The MOU was impounded by the Civil Court and was forwarded to the Additional District Sub-Register Arambag for appropriate steps. The trial court had passed the order when the PW 1 wanted to mark the MOU as an exhibit. The report of the ADSR, that is the Respondent No. 5, dated September 13, 2019, was forwarded to the court and the same is quoted below:-

“GOVERNMENT OF WEST BENGAL

OFFICE OF THE ADDITIONAL DISTRICT SUB-REGISTRAR,

ARAMBAGH

PO+PS- ARAMBAGH, DIST- HOOGHLY

PIN- 712601

| Memo No- 174 | Dated- 13th September, 2019 |

To

The Sheristader,

Civil Judge (Jr. Divn.), 2nd Cout, Arambagh,

Arambagh, Hooghly

Sub: Submission of Valuation Report in connection

Agreement to sell – If instead of separate instruments, distinct matters are made subject matter of one instrument, liability to pay duty would be still found within four walls of Section 5 of Stamp ....

The main legal point established in the judgment is the distinction between lease and license as per the Indian Stamp Act, 1899, and the treatment of lease renewal and security deposit for stamp duty....

Suit for Specific Performance – Liability to pay stamp duty – Stamp duty is on instrument and not on transaction – It is immaterial, whether possession of property has been handed over at the time of....

In Court-ordered sales, stamp duty applies only to the sale consideration, not to market value, as established by the Transfer of Property Act.

A scheme of arrangement involving amalgamation or demerger qualifies as an instrument under the Indian Stamp Act, subject to applicable stamp duties.

The court affirmed that all components of the sale, including outstanding mortgage obligations, must be considered for stamp duty valuation, adhering strictly to statutory definitions.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :