THE GAUHATI HIGH COURT, (HIGH COURT OF ASSAM, NAGALAND, MIZORAM AND ARUNACHAL PRADESH)

N. UNNI KRISHNAN NAIR, J.

M/S. Om Telecom Logistics Pvt. Ltd Rep. By Sri Binod Kumar Sarma – Appellant

Versus

The State Of Assam, Rep. By The Commissioner And Secy. To The Govt. Of Assam, Min Of Financetaxation Depptt, And Ors. Respondent

WP(C) 3469 Of 2017

Decided On : 06-01-2026

| Table of Content |

|---|

| 1. petitioner's challenge to tax compounding (Para 2 , 3) |

| 2. arguments regarding jurisdiction for compounding (Para 4 , 5) |

| 3. details of notice against the petitioner (Para 6 , 7) |

| 4. jurisdiction to compound the offence (Para 10 , 11 , 12) |

| 5. rejection of petitioner's claims and validation of compounding (Para 13 , 14) |

| 6. writ petition dismissed due to lack of merit (Para 15 , 16) |

JUDGMENT :

N. UNNI KRISHNAN NAIR, J.

1. Heard Ms. N. Hawelia, learned counsel for the petitioner. Also heard Mr. B. Gogoi, learned Addl. AG, Assam appearing for all the respondents.

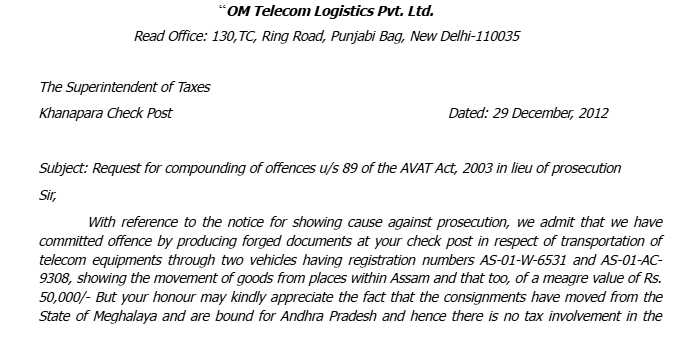

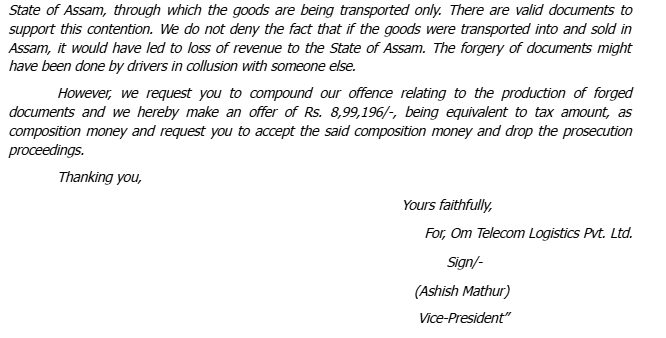

2. The challenge in the present writ petition is to an order dated 27-12-2012 passed by the Superintendent of Taxes, Khanapara Check Post, Guwahati, Assam, compounding the offence involved under Section 85 (1)(n) of the Assam Value Added Tax Act, 2003 (in short the Act of 2003), exercising the delegated power under Section 89 of the Act of 2003 and requiring the petitioner to deposit an amount of Rs. 8,99,196/- (Rupees Eight Lakhs Ninety Nine Thousand One Hundred Ninety Six) by way of composition of the said offence as alleged against the it. The challenge primarily is on the ground that under the provision of of the Act of 2003, the Superintendent of Taxes is not empowered to compound an offence under the Act.

3. The petitioner/ Company is a transporter and had entered into an agreement with the Bharti Hexacom Ltd., for transportation of its goods within the Northeastern region and also outside the region. In connection with transportation agreement entered into by the petitioner/ Company with the Bharati Hexacom Ltd., two trucks bearing No. AS-01W- 6531 and AS-01AC-9308 were loaded with goods of the Bharti Airtel Ltd. purportedly for transportation to Andhra Pradesh on stock transfer basis. The loading of the said truck was made at Meghalaya. While crossing the Khanapara Check Post, the said trucks were come to be detained and the drivers were issued with notices requiring production of supporting documents in connection with the transportation of goods by the said trucks. The authorized representative of the petitioner/ Company submitted a representation before the Superintendent of Taxes, Khanapara Check Post, Guwahati, Assam, i.e. the respondent No. 3 clarifying the nature of the goods being transported and praying for issue of transit pass. The respondent authorities not being satisfied with the clarification given by the petitioner/ Company, proceeded to issue a show-cause notice to the petitioner/ Company on 19-12-2002, demanding an amount of Rs. 35,96,783/- (Rupees Thirty Five Lakhs Ninety Six Thousand Seven Hundred Eighty Three) being the tax and penalty applicable. The said notice was replied to by the authorized representative of the Company. Thereafter, vide notice dated 28-12-2012, the Superintendent of Taxes, Khanapara Check Post, Guwahati, Assam, by projecting that the two trucks involved coming from the Byrnihat on being intercepted had produced computer printout of “Non- Returnable Gate Pass-cum- Delivery Challan” bearing No. 1245 dated 12-12-2012 showing transportation of equipment involved valued at Rs. 50,000/- (Rupees Fifty Thousand) only (for both trucks) within Assam by Bharti Airtel Ltd., held that the consignment involved was not supported by any tax clearance certificate as required under the provision of Rule 41(9) of the ASSAM VALUE ADDED TAX RULES , 2005 (in short the Rules of 2005). It was further projected that the Bharti Hexacom Ltd. as well as Bharti Airtel Ltd. had given a statement to the effect that the “Non-Returnable Gate Pass-cum-Delivery Challan” produced at the Check Post were not generated by them. It was also projected that the goods under seizure, were dispatched by Bharti Hexacom Ltd. from Meghalaya to Bharti Airtel Ltd. at Andhra Pradesh pursuant to inter-State sale and such transaction was supported by an invoice dated 06-11-2012 for an amount of Rs. 1,79,83,912/- (Rupees One Crore Seventy Nine Lakhs Eighty Three

The Superintendent of Taxes had jurisdiction to compound an offence under the Assam VAT Act based on proper delegations, and the admission of offence by the petitioner affirmed the validity of the co....

The Superintendent of Taxes was authorized to compound an offence under the Assam Value Added Tax Act, despite the petitioner's claims to the contrary.

The Excise Commissioner lacked jurisdiction to compound offences under Section 75 of the Odisha Excise Act, 2008, as authority is reserved for the Collector or specific Excise Officers.

Once a contravention has been compounded, no further proceedings can be initiated or continued against the person committing the contravention.

The application of new compounding guidelines for offences under the Income Tax Act cannot override previously established rights affirmed by judicial orders, maintaining the principle of legal final....

A circular cannot override or restrict the application of specific provisions enacted by the legislature and cannot take away a statutory right with which an assessee has been clothed.

Delegation of authority in taxation must strictly adhere to statutory provisions, maintaining clear distinctions between audit, assessment, and collection roles.

Officials are not liable for corruption charges regarding compounding offences if actions were taken under regulations prior to the fixed minimum fee introduction. Notifications under repealed Acts r....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :