IN THE HIGH COURT OF KERALA AT ERNAKULAM

Harisankar V.Menon, A.Muhamed Mustaque

K.G.Rejimon – Appellant

Versus

State Of Kerala, Represented By Its Secretary, Taxes Department – Respondent

ORDER :

Harisankar V.Menon, J.

This Other Tax Revision Petition, at the instance of an assessee under the provisions of the Kerala Value Added Tax Act, 2003 (hereinafter referred to as the ‘Act’), seeks to challenge the suo motu steps initiated under Section 56 of the Act, cancelling an assessment completed in his favour, as confirmed by the Commissioner of Commercial Taxes.

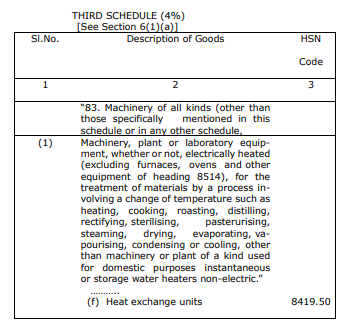

2. The assessee is stated to be engaged in the trading of “thermic fluid heater”, which, according to him, attracts tax at 4% under Entry 83(1)(f) of Schedule III to the Act. The assessment was of the year 2009-10 by an order dated 11.11.2013, imposing tax at the rate of 12.5% on the afore item, placing reliance on a clarification dated 12.08.2006 of the Commissioner of Commercial Taxes, as per which, the tax payable was at 12.5%. The assessment was challenged before the first appellate authority by filing KVATA No.99 of 2014 and by the appellate order dated 31.01.2014, the first appellate authority noticed that the clarification relied on while finalizing the assessment has been set aside by this Court in the judgment dated 15.02.2008 in OTA No.3 of 2008, since there was no proper consideration of the issue by th

The Deputy Commissioner has the authority to exercise suo motu revisional powers when previous assessments do not reflect accurate tax classification, with clarificatory orders applied prospectively ....

Suo motu revisions under the KVAT Act cannot proceed while an appeal on the same issue is pending, emphasizing adherence to statutory provisions.

Invalid delegation of powers and lack of jurisdiction of the Addl. CST under the OVAT Act.

Section 56 of the VAT Act would reveal that the section has wide power, but seeking of permission by the assessing authority for making reassessment of the dealer is not conferred under the said prov....

Availability of an alternative remedy does not operate as an absolute bar to maintainability of writ petition.

The court established that the authority to review and revise assessment orders under the JVAT Act is limited and must adhere to procedural requirements, particularly regarding the initiation of revi....

A Deputy Commissioner can order reopening of assessments under CST Act Section 9(2A), without invalidating prior assessment orders, ensuring due process is followed.

The main legal point established is that assessment proceedings must adhere to the prescribed limitation periods under Sections 25(1) and 56(2)(c).

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :