IN THE HIGH COURT OF JUDICATURE AT MADRAS

ANITA SUMANTH, G. ARUL MURUGAN, JJ.

D.K. Sadasivam - Petitioner

Versus

The Commercial Tax Officer, Commercial Tax Department, Dharmapuri & Ors. - Respondents

W.P.Nos.2061 & 2062 of 2012 and M.P.Nos.1 & 1 of 2012

Decided On : 21-01-2025

| Table of Content |

|---|

| 1. identification of parties and property in dispute. (Para 1 , 2) |

| 2. background on financial arrangements and property charges. (Para 4 , 5 , 6 , 10) |

| 3. competing claims between creditors and government. (Para 7 , 11 , 12 , 17 , 21) |

| 4. financial institution's role and priority. (Para 8) |

| 5. priority of secured creditors' claims. (Para 18 , 22 , 26 , 36) |

| 6. procedural due diligence in auction purchases. (Para 29 , 30 , 32 , 39) |

| 7. determining priority based on timing of registered charges. (Para 34 , 38 , 42) |

| 8. determination of encumbrance priority through registration dates. (Para 40) |

| 9. final decision regarding the allowed writ petitions. (Para 44 , 45) |

ORDER :

ANITA SUMANTH, J.

These two Writ Petitions have been filed by an individual, the successful purchaser of the property at S.Nos. 7/10, 7/11 and 13/1 in Sigarahalli Village, Pennagaram Taluk, Dharmapuri District (subject property). The prayer in W.P.No.2061 of 2012 is for a Certiorari calling for and quashing demand notice dated 12.01.2012 issued by the Commercial Taxes Officer, Dharmapuri District/R1, in respect of the subject property.

2. The prayer in W.P.No.2062 of 2012 is for a mandamus forbearing R1 as well as the Assistant Commissioner of the Commercial Taxes Department, Dharmapuri District/R2 from in any way attaching or alienating the subject property. The District Collector is arrayed as R3. The Tamil Nadu Industrial Investment Corporation at Chennai and Dharmapuri is arrayed as R4/R5 (hereinafter referred to either as TIIC or as R4/R5) and one Jayam Food Processing Industries is arrayed as R6 (hereinafter referred to either as R6 or assessee).

3. R3 to R6 are unrepresented before us and we have heard the detailed submissions of Mr.P.Valliappan, learned Senior Counsel appearing for Mr.T.Deeraj, learned counsel for the petitioner and Mr.Nanmaran, learned Special Government Pleader for R1 and R2. Counters have been filed on behalf of R1/R2 as well as R4/R5.

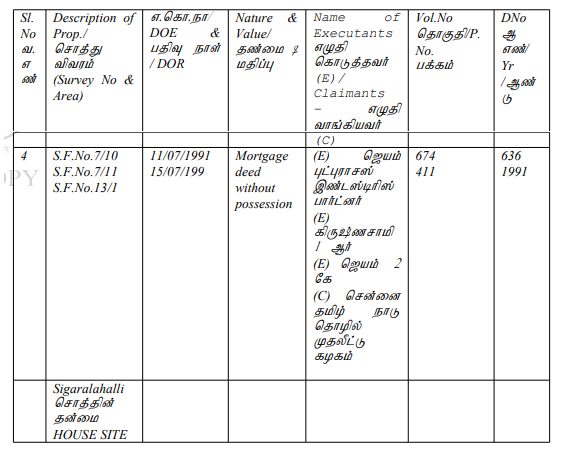

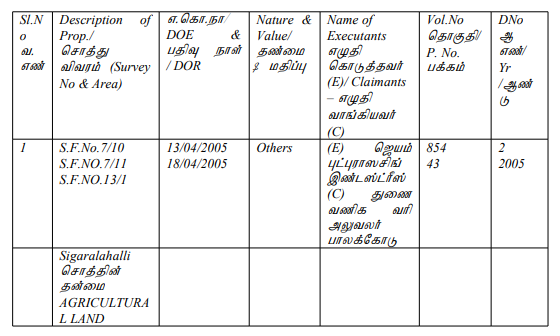

4. From the pleadings as well as the submissions made by learned counsel, the following facts emerge. R4/R5 had provided financial assistance to R6 for setting up of a manufacturing project for fried gram. The deed of hypothecation-cum-mortgage was executed qua R6 and R4 on 11.07.1991 in respect of the subject property admeasuring a total extent of 4.13 acres by way of security for the financial assistance extended. Out of the total extent of 4.13 acres, 11 cents had been acquired by the Government for widening of the road.

5. The Encumbrance Certificate that has been placed on record reflects the creation of the charge on the subject property even as early as on 11.07.1991/15.07.1991. There appears to have been defaults by R6 in repayment of the financial facilities to TIIC and hence TIIC, invoking its power under Section 29 of the State Financial Corporations Act, 1951 (in short ‘SFC Act’), took possession of the subject property exercising the power to sell.

6. Auction sale notice was issued on 24.09.2003 by TIIC offering various units held by TIIC for public auction through sealed tender. Item 3 thereof refers to the subject property and reads thus:

| Name of the Branch | Location | Activity | Details of Assets |

Dharmapuri Branch 3. Jayam Food Processing Unit | Sigralahalli Village Konangihalli, Near Thalapallam Village, Pennagaram TK | Mfr. of Fried Grams | Land 4.13 acres & Building 21419 Sq.ft. ACC Roof 477 Sq.ft. RCC roofing 2978 sq.ft. Aluminium sheet roof open well 8500 sq.ft. drying yard 822 sq.ft. MTR Security shed & compound wall with Machinery |

7. Our attention is specifically drawn by the learned Special Government Pleader to the conditions in that auction sale notice to the effect that ‘the assets of the following industrial units are offered for sale ‘AS IS WHERE IS CONDITIONS’ through public auction/sealed tender at our branch offices’. Thus, according to him, the incident of auction sale carried with it the liability to sales tax arrears as well.

8. This would brings us to the rival claim of the Commercial Taxes Dep

The court affirmed that earlier registered charges of financial corporations take precedence over later sales tax claims, emphasizing the significance of prior registration dates in determining legal....

The financial institution's charge takes precedence over tax claims due to earlier registration, establishing the priority of charges in property disputes.

The banking institution's lien on fixed deposits for prior credit facilities takes precedence over subsequent tax demands under the Tamil Nadu General Sales Tax Act.

Auction purchasers under the SARFAESI Act cannot be held liable for the previous owner's tax liabilities unless explicitly stated in the sale notice.

A bona fide purchaser without notice of an encumbrance is protected under Section 24-A of the TNGST Act, 1959, reinforcing the importance of constructive notice criteria.

Bank is entitled only for a priority in payment alone, it can never be said to be a charge created over property against statutory charge contained under KGST Act, 1963 and KVAT Act, 2003 or any Cent....

The provisions of Section 26E of the SARFAESI Act 2002 and Section 31B of the Recovery of Debts and Bankruptcy Act, 1993 create "First Charge" by way of priority in favour of the Banks and Financial ....

The main legal point established in the judgment is that the charge of the Secured Creditor will precede over the charge of an Unsecured Creditor (Crowns Date) based on the provisions of the SARFAESI....

The main legal point established in the judgment is that under the SARFAESI Act, the petitioner was not liable to pay any additional differential premium and the Sales Tax Department could not claim ....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :