BEFORE THE MADURAI BENCH OF MADRAS HIGH COURT

D. BHARATHA CHAKRAVARTHY, J.

M/s. Dhanalakshmi Srinivasan Sugars Private Limited, Represented by its Managing Director S. Jagatheesan - Petitioner

Versus

Deputy Commissioner of Income Tax, Central Circle 2, Madurai, Tamil Nadu – Respondent

W.P.(MD)Nos.10711 to 10716, 5709, 5710 and 11470 to 11478 of 2025 and W.M.P.(MD) Nos.4171, 4173, 8529 and 8530 of 2025

Decided On : 01-06-2026

| Table of Content |

|---|

| 1. procedural history of search, settlement applications, interim court orders, and subsequent assessment and recovery notices. (Para 1 , 2) |

| 2. claim that assessment orders were void due to lack of jurisdiction and failure to comply with statutory limitation periods upon abatement of settlement proceedings. (Para 3) |

| 3. revenue's contention that assessment orders were validly passed under court-granted liberty and that petitioners are barred by estoppel and failure to exhaust alternative remedies. (Para 4) |

| 4. court finds assessment orders valid under specific interim protections; jurisdiction was not divested; parties are bound by the court's earlier orders regarding limitation. (Para 5) |

| 5. writ petitions challenging the assessment orders are dismissed. (Para 6) |

ORDER :

D. BHARATHA CHAKRAVARTHY, J.

A. The Petitions :

M/s. Dhanalakshmi Srinivasan Sugars Private Limited (DSSPL), incorporated under the Companies Act, 2013, and represented by its Managing Director, S.Jegatheesan, and M/s. V.V.Mineral (VVM), a registered partnership firm represented by its partner, S.Jegatheesan, have filed these Writ Petitions. Both entities claim to be part of M/s. V.V. Group is a conglomerate operating across various sectors.

1.1 These Writ Petitions are connected to each other and, as such, are taken up and disposed of by this common order.

B. The Facts:

2. On 25.10.2018, the Income Tax Department conducted a search under Section 132 of the Income Tax Act, 1961 (in short, 'the Act') at the premises of DSSPL and VVM and yet another entity, and certain materials and documents were seized. Thereafter, on 28.11.2019, notices were issued to all three entities for the assessment years from 2013 – 2014 to 2018 – 2019. While the proceedings were pending, it is the case of DSSPL and VVM that they contemplated approaching the Income Tax Settlement Commission (ITSC) under Section 245(c) of the Act. During this period, the Government of India introduced a Finance Bill on 01.02.2021, proposing to discontinue the ITSC and constitute an Interim Board of Settlement (IBS) for pending cases. No new applications were filed with effect from 01.02.2021.

2.1. On 04.03.2021, feeling aggrieved by the proposal that no new applications shall be filed, the petitioners filed W.P.(MD) Nos. 4661, 4664, and 4668 of 2021 to direct the IBS to take the petitioners' applications on file. A common interim order was passed on the petitioners’ interim prayer, on the submission that mere receipt of the petitioners’ applications would not confer any right on them, and the ITSC was directed to receive the petitioners’ applications.

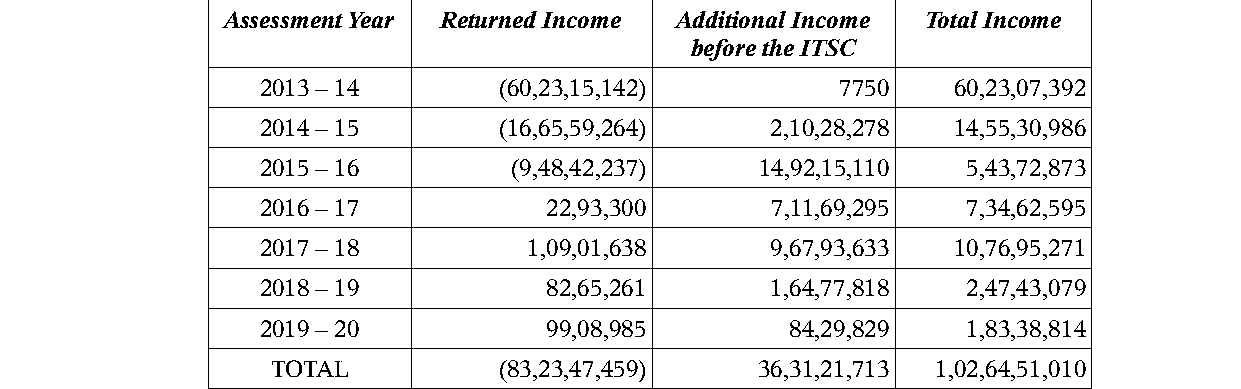

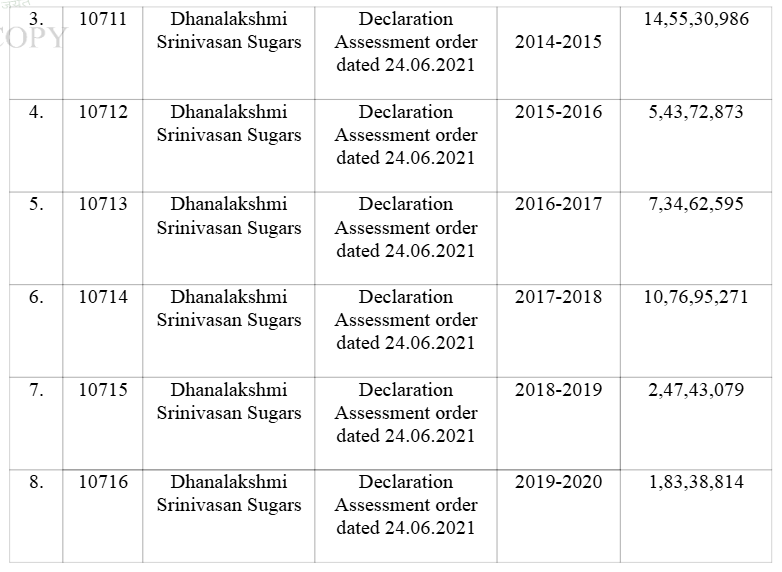

2.2. On 09.03.2021, DSSPL and VVM filed applications before the IBS seeking additional income. The following table contains the particulars of the assessment years, the original income disclosed by DSSPL in the returns, the additional income offered in the applications for settlement, and the total income:-

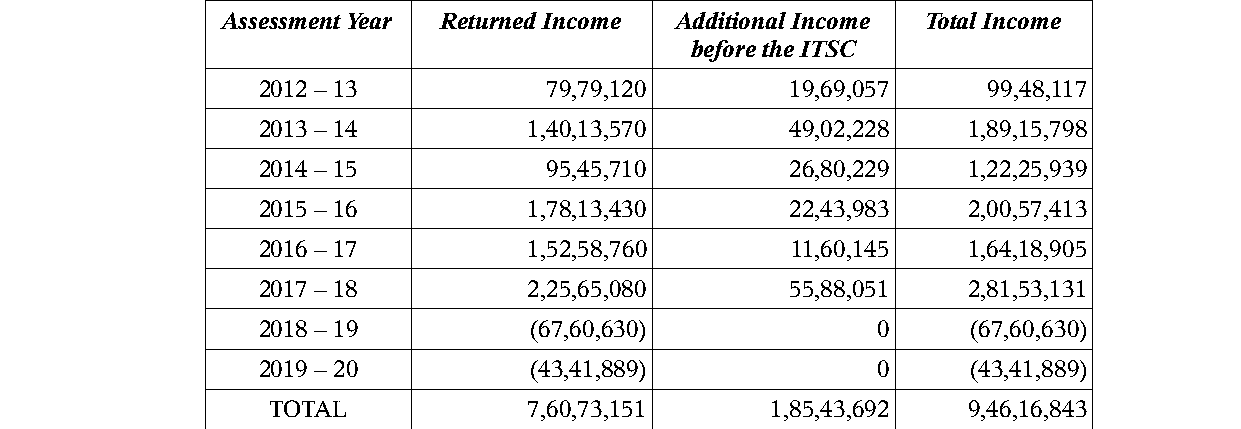

2.3. Thus, it is seen that, as against the already disclosed income of Rs.83,23,47,459/-, DSSPL offered a total income of Rs.1,02,64,51,010/-. Similarly, the following table reflects the data with respect of VVM :

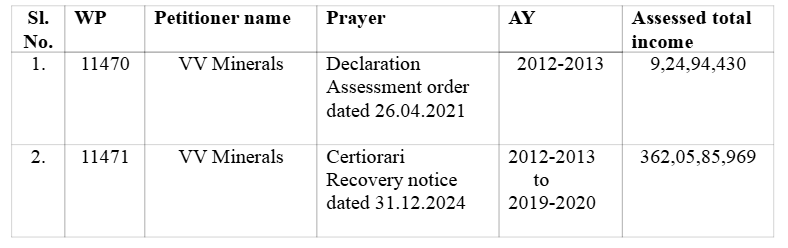

2.4. Thus, it is seen that, as against the original income of Rs.7,60,73,151/-, additional income was offered, totalling Rs.9,46,16,843/-.

2.5. On 29.03.2021, the Finance Bill, 2021 received the assent of the Hon'ble President and came into force on 01.04.2021, whereby the IBS was constituted to hear all applications pending before the ITSC as on 01.02.2021. Under these circumstances, when the Writ Petitions filed by DSSPL and VVM came for further hearing on 30.04.2021, particularly regarding the extension of interim orders, the following interim order was passed after considering the interim order passed by the Principal Bench of this Court. Paragraph Nos. 2, 3 and 4 of the said order dated 30.04.2021 are extracted hereunder for ready reference:-

“2.Today when the matter is taken up for hearing, the learned Special Government Pleader has produce

Assessment orders passed during the pendency of settlement proceedings under court-sanctioned interim liberty are not void ab initio, and the enforcement of such orders is permissible upon the reject....

The court emphasized the exclusive jurisdiction of the Interim Board over settlement applications filed after 31.01.2021 and the impact of circulars issued by the CBDT in determining the validity of ....

The main legal point established in the judgment is the admissibility of a writ petition challenging Assessment Orders under the CST Act, considering grounds of limitation, lack of opportunity for he....

:PRACTICE AND PROCEDURE - When the cases are not listed on a particular day more specifically on the day of expiry of an interim order, then the parties cannot be penalised or blamed for non-listing ....

The main legal point established in the judgment is that the remedy under taxing law is a statutory remedy and not an alternative remedy.

The assessment order was invalid as it was issued beyond the limitation period prescribed under Section 153 of the Income Tax Act, necessitating adherence to statutory timelines.

Limitation would arise under Section 29(6) of the Act, only in the event and at the stage of the application filed under Section 32 being allowed.

Retrospective amendments cannot affect vested rights, and valid applications filed before such amendments remain enforceable.

The court established that the CBDT cannot impose additional eligibility conditions for settlement applications beyond what is prescribed in the Income Tax Act.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :