IN THE HIGH COURT OF ORISSA AT CUTTACK

HARISH TANDON, CJ, MURAHARI SRI RAMAN, J.

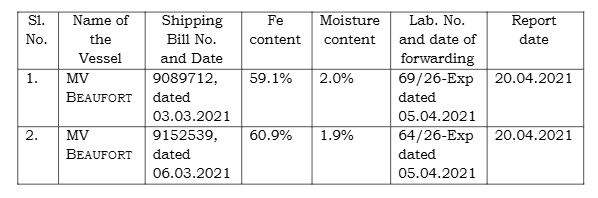

Commissioner of Customs (Preventive) Odisha – Appellant

Versus

M/s. Essel Mining and Industries Ltd. – Respondent

OTAPL No. 50 of 2025

Decided On : 15-01-2026

| Table of Content |

|---|

| 1. jurisdiction over customs act appeal. (Para 1) |

| 2. facts surrounding the export of iron ore. (Para 2) |

| 3. court's examination of evidence and finding. (Para 3 , 6 , 7) |

| 4. arguments by the appellant regarding test report reliability. (Para 4) |

| 5. defense arguments pertaining to test samples. (Para 5) |

| 6. analysis of customs duty implications. (Para 8) |

| 7. finding and valuation based on wmt. (Para 9) |

| 8. consideration of substantial questions of law. (Para 10) |

| 9. final decision and dismissal of the appeal. (Para 11 , 12) |

JUDGMENT :

MURAHARI SRI RAMAN, J.

1. This appeal under Section 130 of the CUSTOMS ACT , 1962 (for short, “the Act”) filed by Commissioner of Customs (Preventive) is directed against Final Order No.77815/2024, dated 04.12.2024 in Customs Appeal No.75881 of 2023 passed by the Customs, Excise and Service Tax Appellate Tribunal, Eastern Zonal Bench, Kolkata (be referred to as “the CESTAT”) arising out of Order-in-Appeal No.72/CUS/CCP/2023, dated 08.06.2023 passed by the Commissioner (Appeals), GST, CX and Customs, Central Revenue Building, Rajaswa Vihar, Bhubaneswar–751007, Odisha, where the following question(s) of law for adjudication are suggested for formulation:

"(i) Whether on the facts and circumstance of the case, the learned Tribunal is correct as per law and facts in dismissing the appeal filed by Department against the Order-in-Appeal No.72/CUS/CCP/2023, dated 09.06.2023 passed by the Commissioner (Appeal), Bhubaneswar ignoring the errors in the said Order-in-Appeal dated 09.06.2023?

(ii) Whether on the facts and circumstances of the case, the NABL Accredited Private Testing Agency‘s test report, where the test simple is not a representative one as it is solely drawn by the exporter themselves without the presence of Customs (which is meant for smooth business transactions between the buyer and seller as per the contract between them) can be accepted in this case for payment of Government duty, when the CRCL report, where the sample is drawn in the presence of both the Customs (Government) and the exporter/representatives of the exporter as per the guidelines issued under CBIC Circular No.12/2014-Cus, dated 17.11.2014 is also available?

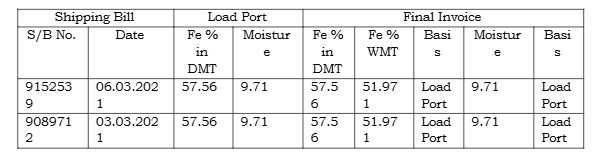

(iii) Whether on the basis of the facts and circumstances of the case, the learned Tribunal is correct in discarding the test report of Chemical Examiner, CRCL, Kolkata and considering the test report of NABL Accredited Private Testing Agencies for determining the levy of export duty holding that the Final invoice and Bank Realisation Certificate has been issued on the basis of such test reports as per the terms and condition of the contract between the buyer and seller, when the said reports of the NABL Accredited Private Testing Agencies are not relevant for the Government for payment of duty on the export consignments as the test samples used by such Private Testing Agencies are not representative one as the same has been solely drawn by the exporter without the presence of the Government (Customs Officer) in terms of Circular No.12/2014-Cus, dated 17.11.2014, whereas the CRCL test report is based on the sample drawn in presence of both the Government (Customs Officer) and the exporter?

(iv) Whether on the basis of the facts and circumstances of the case, the Ld. Tribunal is justified in discarding the test report of CRCL, Govt. of India, Kolkata which is based on the representative test samples in terms of CBIC Circular dated 17.11.2014, holding that the test reports of the NABL Accredited Testing Agencies are more accurate being nearer to the sampling date, when there is no time limit prescribed under the act or rules made there under for testing of samples and also when the said test reports of the Private Testing Labs are not based on the representative samples as the same has been drawn solely by the exporter without the presence of the Customs in terms of CBIC Circular dated17.11.2014?

(v) Whether on the basis of the facts and circumstances of the case, the finding

The court upheld that customs duty assessment is determined based on contractual valuation methods, favoring test results from NABL Accredited agencies over CRCL reports due to compliance with export....

Determination of iron ore content for customs duty purposes must be based on Wet Metric Ton (WMT), not Dry Metric Ton (DMT).

Determination of iron ore fines' FE content for customs duty is based on WMT, not DMT.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :