IN THE HIGH COURT OF PUNJAB AND HARYANA AT CHANDIGARH

JAGMOHAN BANSAL, AMARINDER SINGH GREWAL, JJ.

Commissioner Of Income Tax - Appellant

Versus

M/S Glaxo Smithkline Consumer Healthcare Ltd. - Respondents

ITA-267-2009 (O&M)

Decided On : 04-02-2026

JUDGMENT :

JAGMOHAN BANSAL, J.

1. The appellant through instant appeal under Section 260A of the Income Tax Act, 1961 (for short ‘1961 Act’) is seeking setting aside of order dated 21.03.2007 passed by Income Tax Appellate Tribunal, Chandigarh (for short ‘ITAT’).

2. The appellant has raised following questions for adjudication by this Court:-

(i) Whether on facts and in the circumstances of the case, the ITAT is right in law in treating the expenditure incurred on promotional and trade marketing as revenue expenditure, when the purpose of the expenditure & its intended reality is to obtain benefit of enduring nature?

(ii) Whether on the facts and in the circumstances of the case, the ITAT was right in holding that Excise Duty and Sales Tax will not form part of "total turnover" while computing deduction u/s 80HHC?

(iii) Whether on the facts and in the circumstances of the case the ITAT was right in law in allowing the deduction u/s 80-I of the I.T. Act, 1961, in as much as the machinery had been installed in the same existing factory premises, which is an expansion of the existing factory?

3. Learned counsel for the parties are ad idem that questions No.2 and 3 stand answered against Revenue by this Court or Hon’ble Supreme Court, thus, may be answered against Revenue. Ordered accordingly.

4. Question No.1:- Whether on facts and in the circumstances of the case, the ITAT is right in law in treating the expenditure incurred on promotional and trade marketing as revenue expenditure, when the purpose of the expenditure & its intended reality is to obtain benefit of enduring nature?

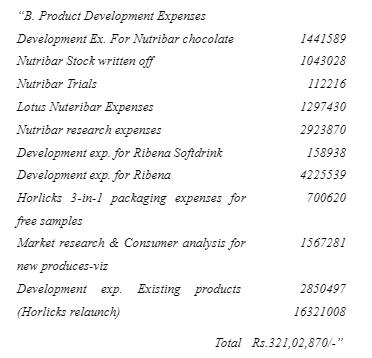

4.1 The respondent is engaged in the manufacture and sale of multiple consumer products. It is incurring expenses on promotion of its product. It besides other expenses incurred a sum of Rs.1.57 crore on promotional and trade marketing expenses and Rs.1.63 crore on product development expenses. The Assessing Officer formed an opinion that aforesaid expenses should be treated as capital expenses. The assessee preferred an appeal which came to be dismissed by CIT(Appeals). The assessee preferred second appeal which was allowed by ITAT. The Tribunal has held that promotional and trade marketing expenses as well as product development expenses should be treated as revenue expenses. From the perusal of nature of expenses incurred on promotional and trade marketing, it can be easily inferred that these expenses are recurring as well as revenue in nature. These expenses cannot be called capital expenses, however, matter needs to be examined with respect to product development expenses. The detail of expenses incurred on product development is as below:-

4.2 The Tribunal has held that in view of nature of the product and activities carried out by the assessee, these expenses should be treated as revenue expenses. The findings recorded by Tribunal read as:-

“10. Now we may examine the expenditure under the head "Product Development Expenses". The details of the expenditure show that the same has been incurred for introducing and developing new products. The assessee is engaged in the business of manufacture and sale of food and health care products under a well known brand. The expenses include development expenses for new products namely nutribar chocolate, Ribena soft drink, Horlicks re-launch expenses. Certainly such expenditure has the potential to improve the profitability of the assessee. However the issue to be considered is whether the expenditure seeks to enlarge the profit yielding capacity or it increases the efficiency of the business. This aspect, in our considered opinion, is to be decided in the light of the business realities under which the assessee is operating. The assessee is engaged in the business of manufacturing of fast moving consumer goods. The business of the assessee is subjected to volatility in consumer preferences, tastes and wants. The assessee is therefore required to perennially study the market and launch new varieties in its products l

Legitimacy of business expenses and their allowance as a deduction under Section 37 of the Income Tax Act, 1961.

The Tribunal correctly classified pre-operative and advertising expenses as legitimate business expenditures, reinforcing the distinction between the setting up and commencement of business.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :