IN THE HIGH COURT OF ALLAHABAD

Saumitra Dayal Singh, J.

J.M. Housing Ltd. – Revisionist

Versus

Commissioner Commercial Tax - Respondent

Sales/Trade Tax Revision No. 333 of 2019

Decided On : 21-04-2023

JUDGMENT :

Saumitra Dayal Singh, J.

Hon'ble Saumitra Dayal Singh, J.-Heard Shri Rakesh Ranjan Agarwal, Senior Advocate, assisted by Shri Suyash Agarwal and Shri Nitin Kesharwani, learned counsel for assessee and Shri A.C. Tripathi, learned standing counsel for the revenue.

2. Present revision has been filed by the assessee under Section 58 of the UTTAR PRADESH VALUE ADDED TAX ACT 2008 (hereinafter referred to as the 'Act') against the order of the Commercial Tax Tribunal, Bench II, NOIDA, dated 29.6.2019 passed in Second Appeal No. 52 of 2019 for the A.Y. 2010-11 (U.P.). By that order, the Tribunal has partly allowed the assessee's appeal and granted partial reduction in the value 1of goods incorporated in 'works contract' executed by the assessee and thus reduced the tax assessed on 'works contract'. However, on the main issue, whether the constructions raised by the assessee were by way of execution of 'works contract', the finding has been returned in the affirmative i.e. against the assessee.

3. Similar position prevails in other revisions connected to the present revision. Some of those revisions have been filed by other assessees. However, learned Senior Counsel for the assessee stated, the issue involved in all cases is one and the same. Also, in certain other cases, the Tribunal has taken the opposite stand i.e. in favour of the assessee. Thus, Sales/Trade Tax Revision Nos. 671 of 2013, 207 of 2013, 208 of 2013, 209 of 2013, 210 of 2013 have been filed by the revenue, raising the same issue (from the other perspective). Learned Standing Counsel has pointed out, those revisions (filed by the State), had arisen prior to the decision of the Supreme Court in Larsen and Toubro Limited and another v. State of Karnataka and another , 2013 NTN (53) 65 (hereinafter referred to as the 'L&T case').

4. In such circumstance, all the revisions being decided today came to be tagged. Accordingly, they were heard on various dates interspersed with adjournments that became necessary owing to roster changes experienced by way of regular routine of the Court in its day-to-day functioning. The order itself took time to correct, finalize and upload on 31.5.2023, with prior oral intimation to learned counsel for the parties.

5. For the sake of convenience and as has been suggested by learned counsel for the parties, the submissions were first advanced in the present revision being Sales/Trade Tax Revision No. 333 of 2019 ( J.M.Housing Ltd. v. The Commissioner Commercial Tax ) for the A.Y. 2010-11 (U.P.). Accordingly, it is being decided first.

6. This revision was admitted on the following questions of law:

(ii) Whether in the alternative the Tribunal was right in sustaining the addition of 10% in purchase of value of goods for calculating the deemed sale, ignoring the value of goods at the time of incorporation of goods consumed in the construction even though the property in goods passes later on?''

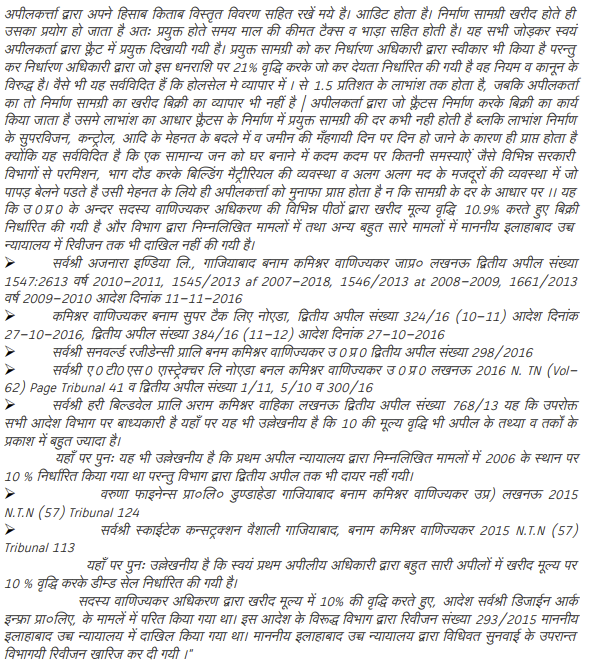

7. No other question has been pressed or stated to be arising in this batch of cases. Undisputedly, the assessee claims to be the lessee of land ad measuring 20900 sq.mtrs, at district Gautam Budh Nagar. It further claims to have decided to develop on that land, a residential housing scheme - 'J.M. Orchid', comprising of two and three bedroom flats, numbering about 684, in all. Without entering into any further agreement with any developer or any third party, the assessee then claims to have started construction of the above described 684 flats, from its own funds. The revenue authorities fo

![]()

The absence of a provision for deduction of the value of land from the total turnover did not render the machinery provision unworkable under the Kerala Value Added Tax Act and Rules.

The court affirmed that a Build, Operate, Transfer (BOT) contract constitutes a works contract under tax laws, making the contractor liable for commercial and entry taxes.

The court established that the turnover of sub-contractors does not add to the main contractor's turnover, affirming the single deemed sale principle and preventing double taxation under the Andhra P....

BOT contracts qualify as works contracts under tax law, with deferred toll payments constituting a sale, thus validating tax assessments during construction prior to toll collection.

Assessment orders issued beyond the three-year limit under Section 24(5) of the PVAT Act, 2007 are invalid; powder coating activities constitute a works contract subject to taxation.

The beneficial provision of zero rated sales is mandatorily required to be a sale 'simpliciter' falling within the five categories enumerated in the definition of 'sale' as defined under Section 2(39....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :