INCOME TAX APPELLATE TRIBUNAL

SHRI KESHAV DUBEY, J, SHRI LAXMI PRASAD SAHU, ACJ

Buckeye Trust No.23 – Appellant

Versus

PCIT-2 – Respondent

ITA No.1051/Bang/2024

ORDER

PER KESHAV DUBEY, JUDICIAL MEMBER:

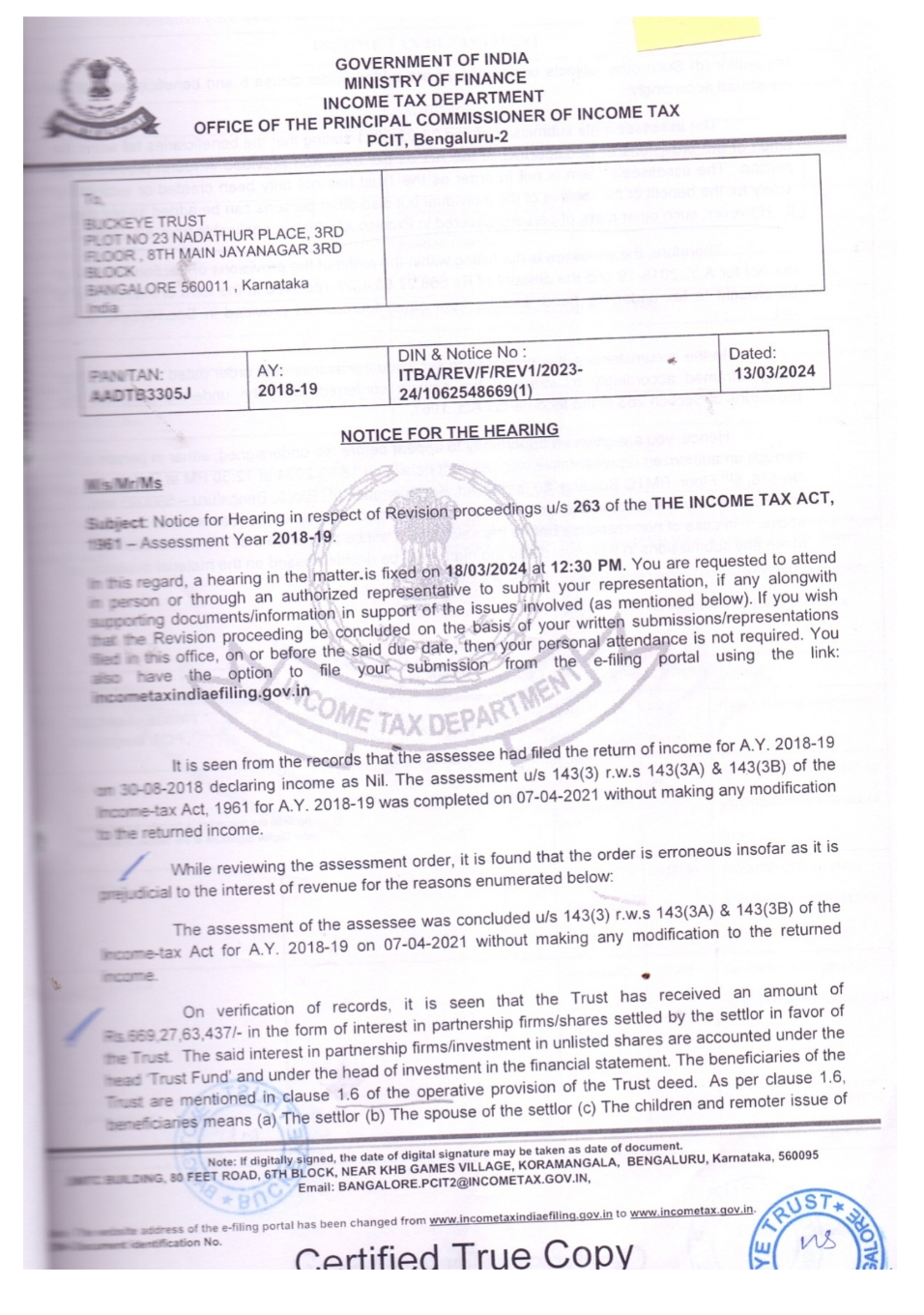

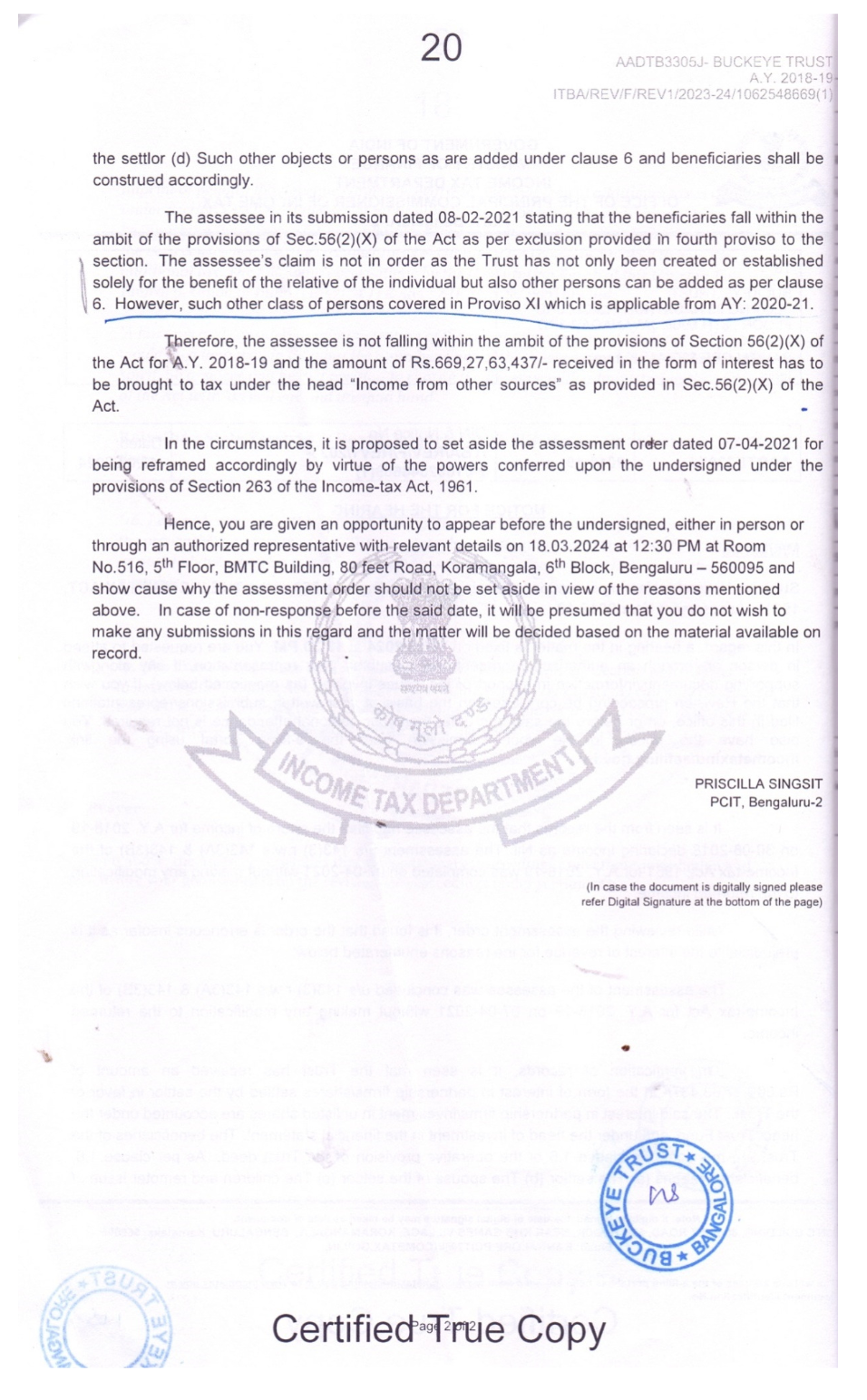

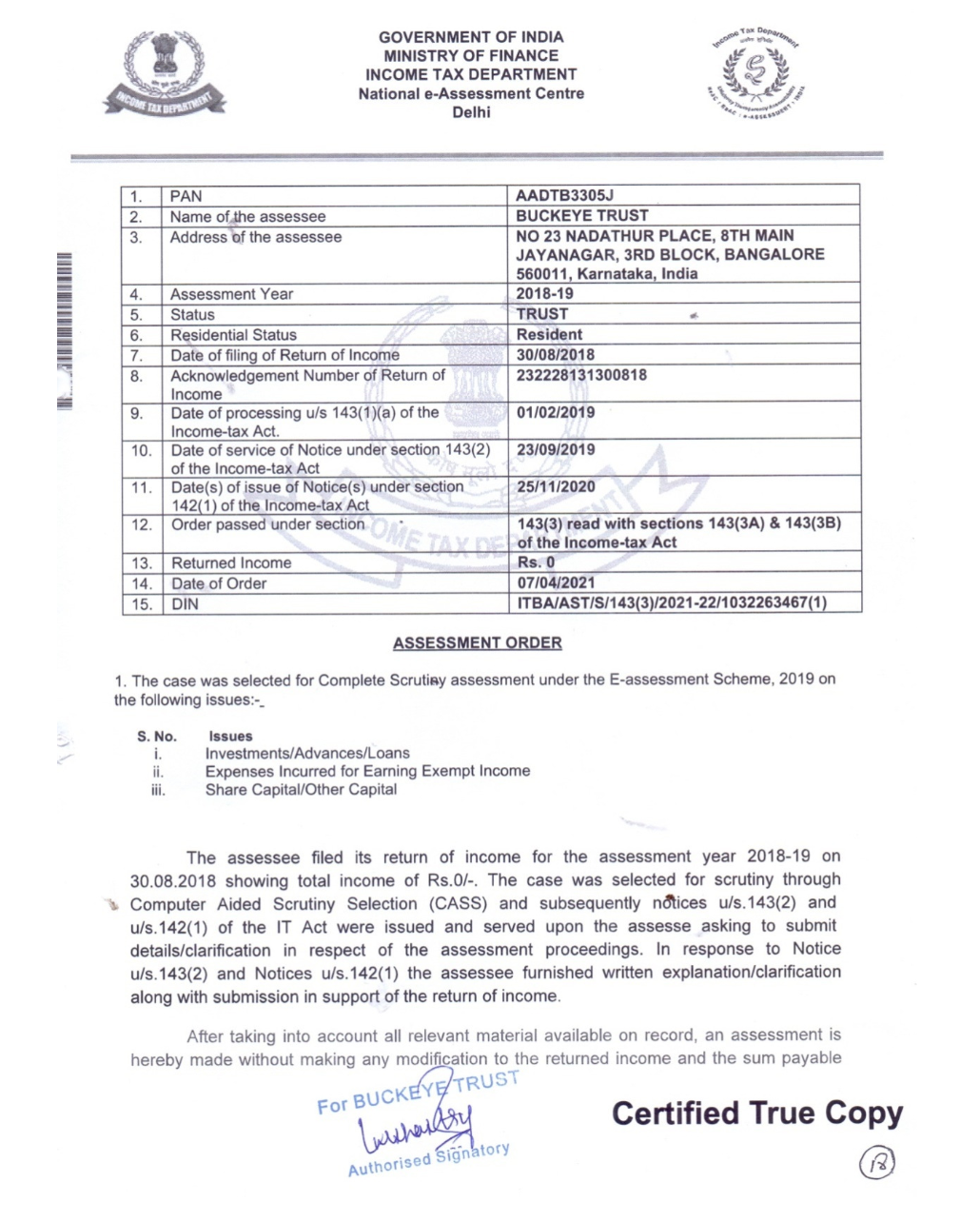

This appeal at the instance of the assessee is directed against the order of ld. PCIT, Bengaluru-2 dated 29/03/2024 vide DIN & Order No. ITBA/REV/F/REV5/2023-24/1063614851(1) passed u/s. 263 of the Income Tax Act, 1961 (in short “the Act”) for the AY 2018-19.

2. The assessee has raised the following grounds of appeal:-

The grounds mentioned herein by the Appellant are independent and without prejudice to one another:

Grounds of appeal

A. General Ground

1. The Learned Principal Commissioner of Income Tax, Bengaluru - 2 ('Ld. PCIT') has erred in passing an order of revision under section 263 of the Income-tax Act, 1961 (the Act') which suffers from legal defects such as being passed in violation of the provisions of the Act and is devoid of merits and is contrary to the facts on record and applicable law and as such liable to be quashed.

2. The Ld. PCIT has finalized the impugned order with improper conclusion without considering the information, arguments and evidence provided by the Appellant.

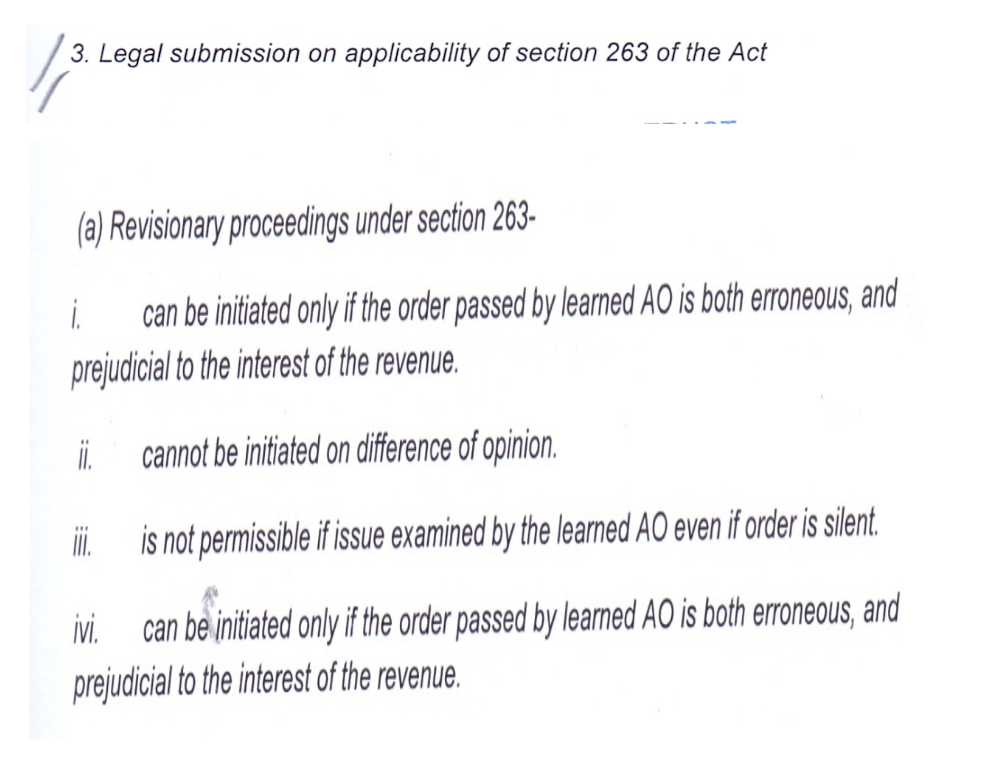

B. Validity of revisionary proceedings under section 263 of the Act

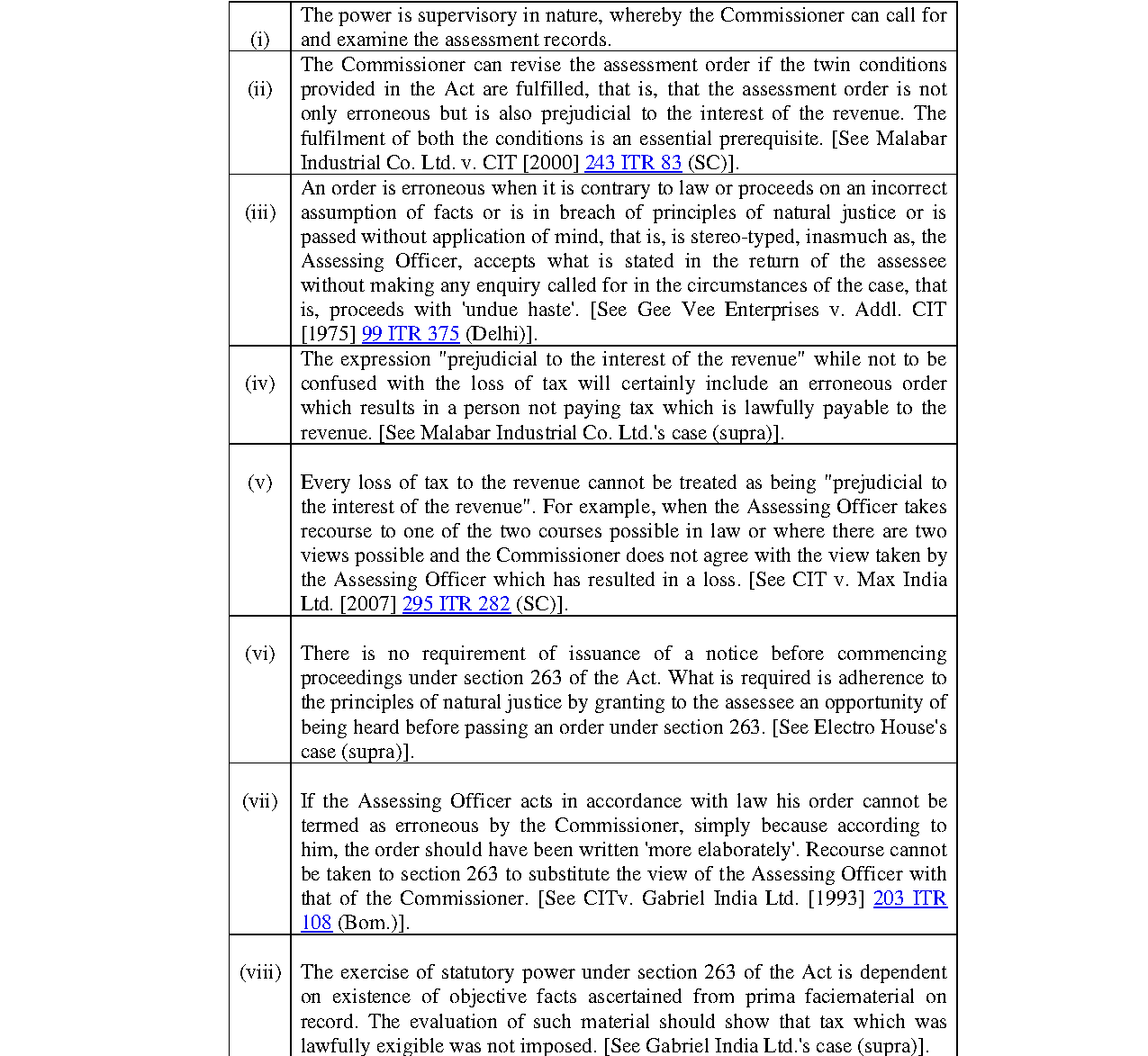

1. The Impugned order passed by the Ld. PCIT is without jurisdiction as the twin conditions prescribed under section 263 of the Act i.e., the order of the Ld. AO shall be 'erroneous' and 'prejudicial to the interest of revenue', are not satisfied.

2. The Ld. PCIT erred in concluding that the assessment order passed under section 143(3) r.w.s 143(3A) and 143(3B) of the Act for impugned AY is erroneous and prejudicial to the interest of revenue, without appreciating the material on record and submissions made by the Appellant.

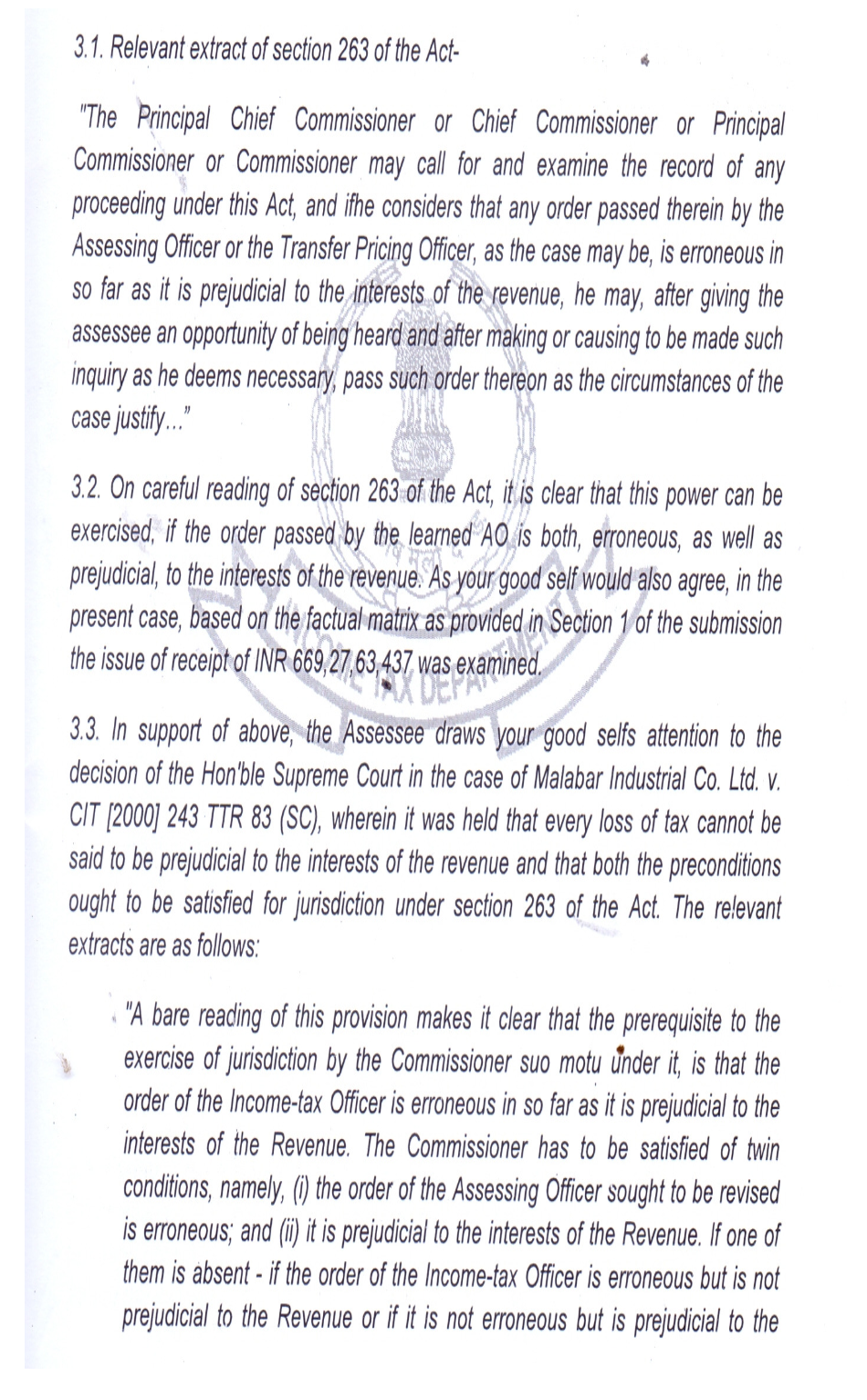

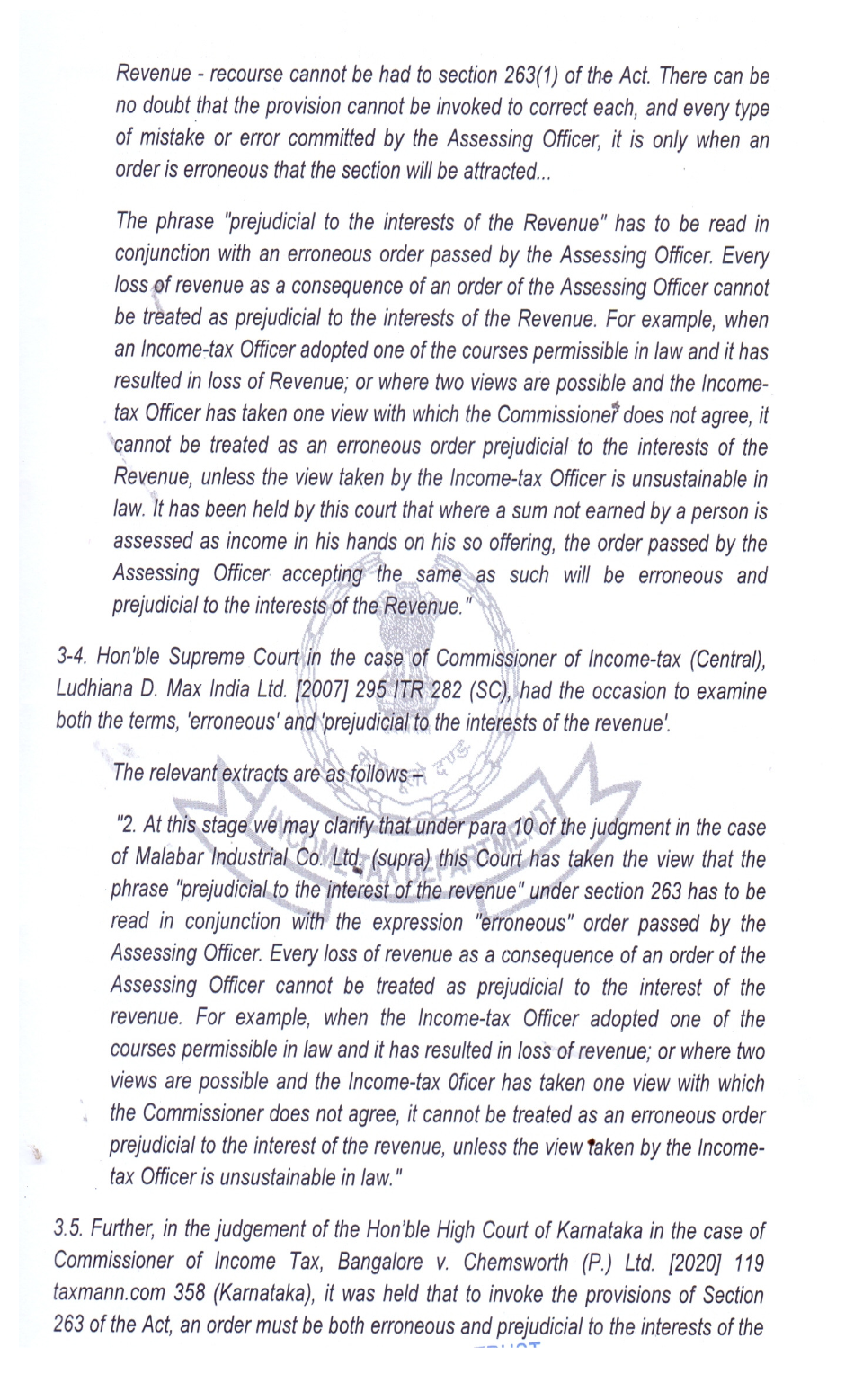

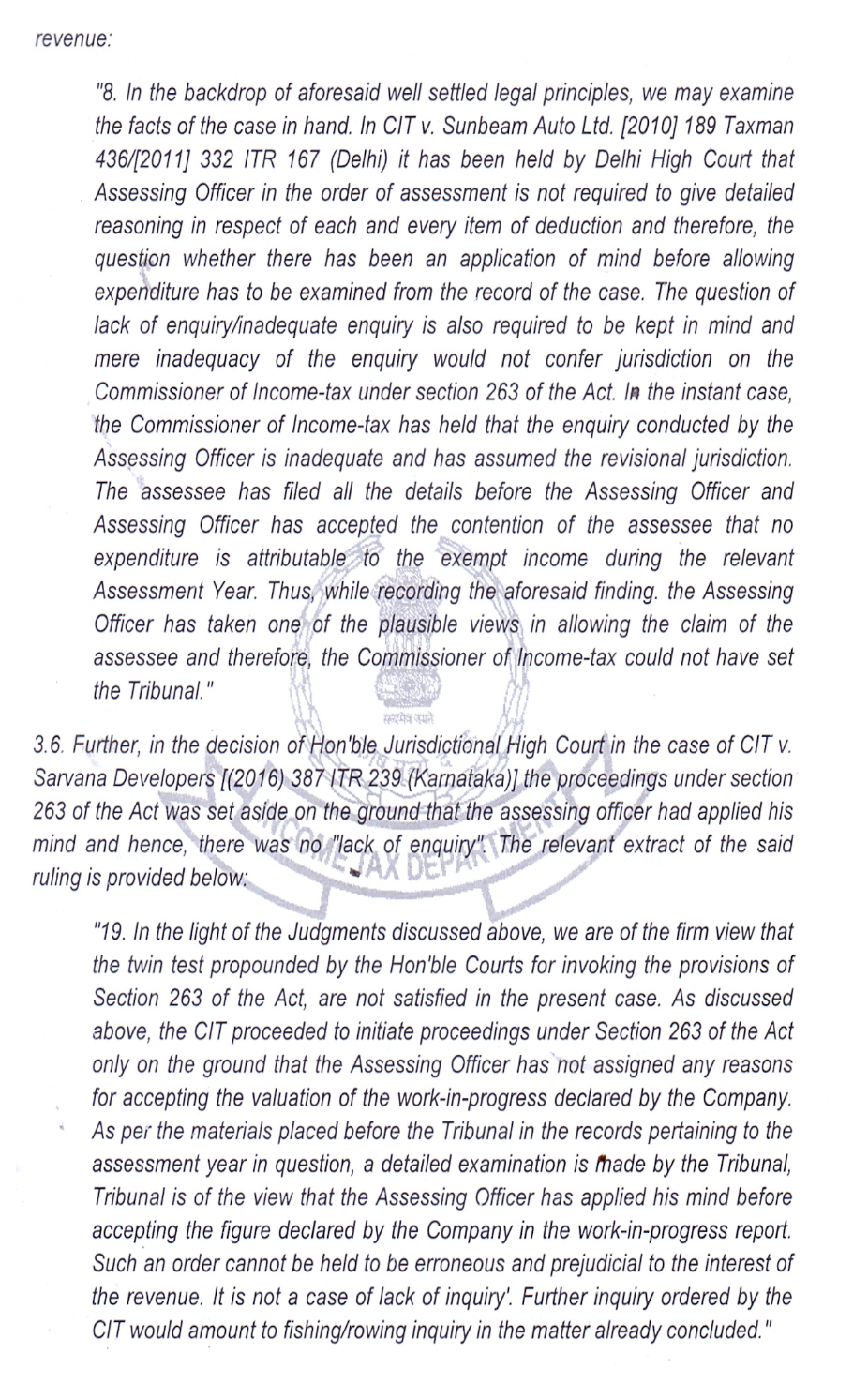

3. The Ld. PCIT erred in passing the impugned order, on the allegation that the Ld. AO has completed the assessment without making necessary enquiries or verifying the taxability of receipt of INR 669,27,63,437, without appreciating that the Ld. AO had duly conducted enquiries and verification on the issue.

C. Taxability of receipt of INR 669,27,63,437

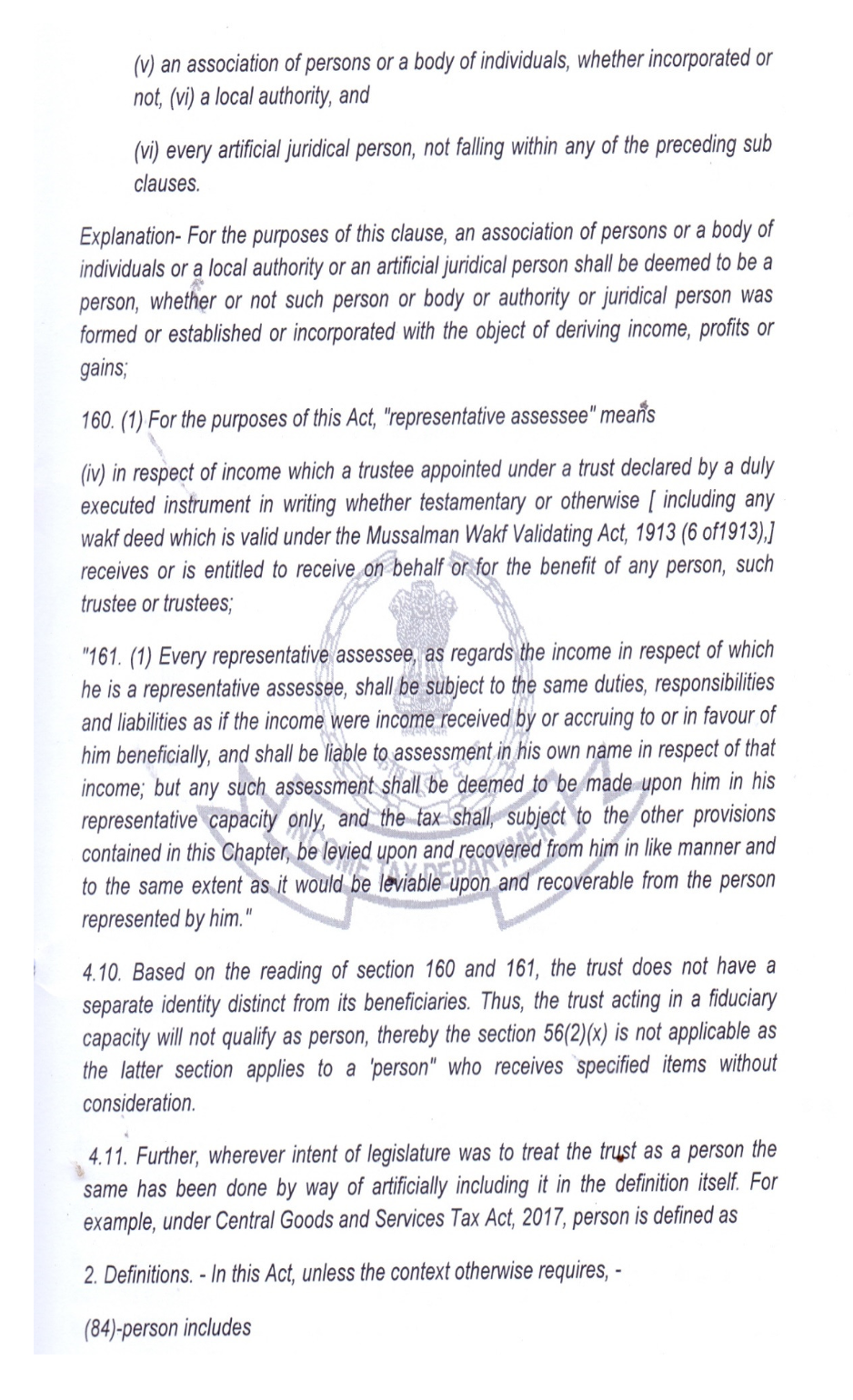

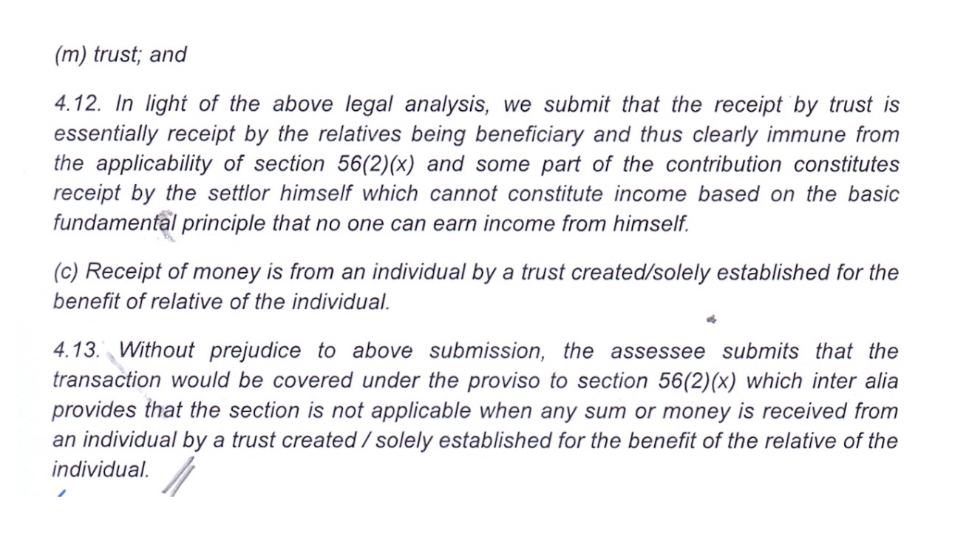

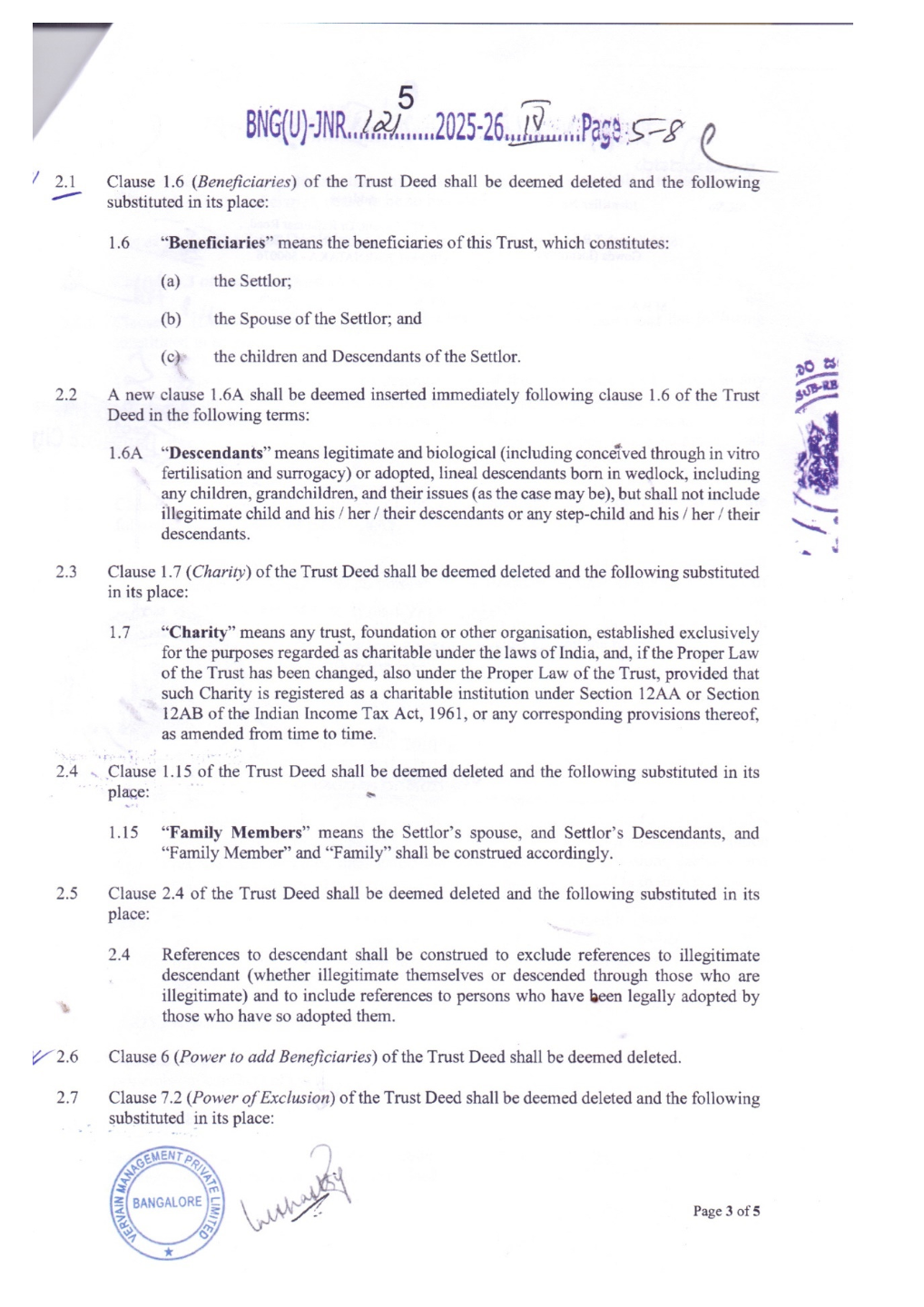

1. The Ld. PCIT has, in the facts and circumstances of the case and in law, erred in disregarding the fact that the receipts of INR 667,47,38,930 out of INR 669,27,63,437 is in form of interest in partnership firms and does not qualify as property as per section 56 of the Act.

2. The Ld. PCIT has, in the facts and circumstances of the case and in law, erred in disregarding the fact that (a) the receipts of INR 669,27,63,437 is not without consideration (b) trust is not a person under section 2(31) of the Act and (c) receipt of money is from individual by a trust created or established solely for the benefit of relative of individual, hence outside the purview of section 56(2)(x) of the Act.

That the Appellant craves leave to add to and/or to alter, amend, rescind, modify the grounds herein above or produce further documents before or at the time of hearing of this Appeal.

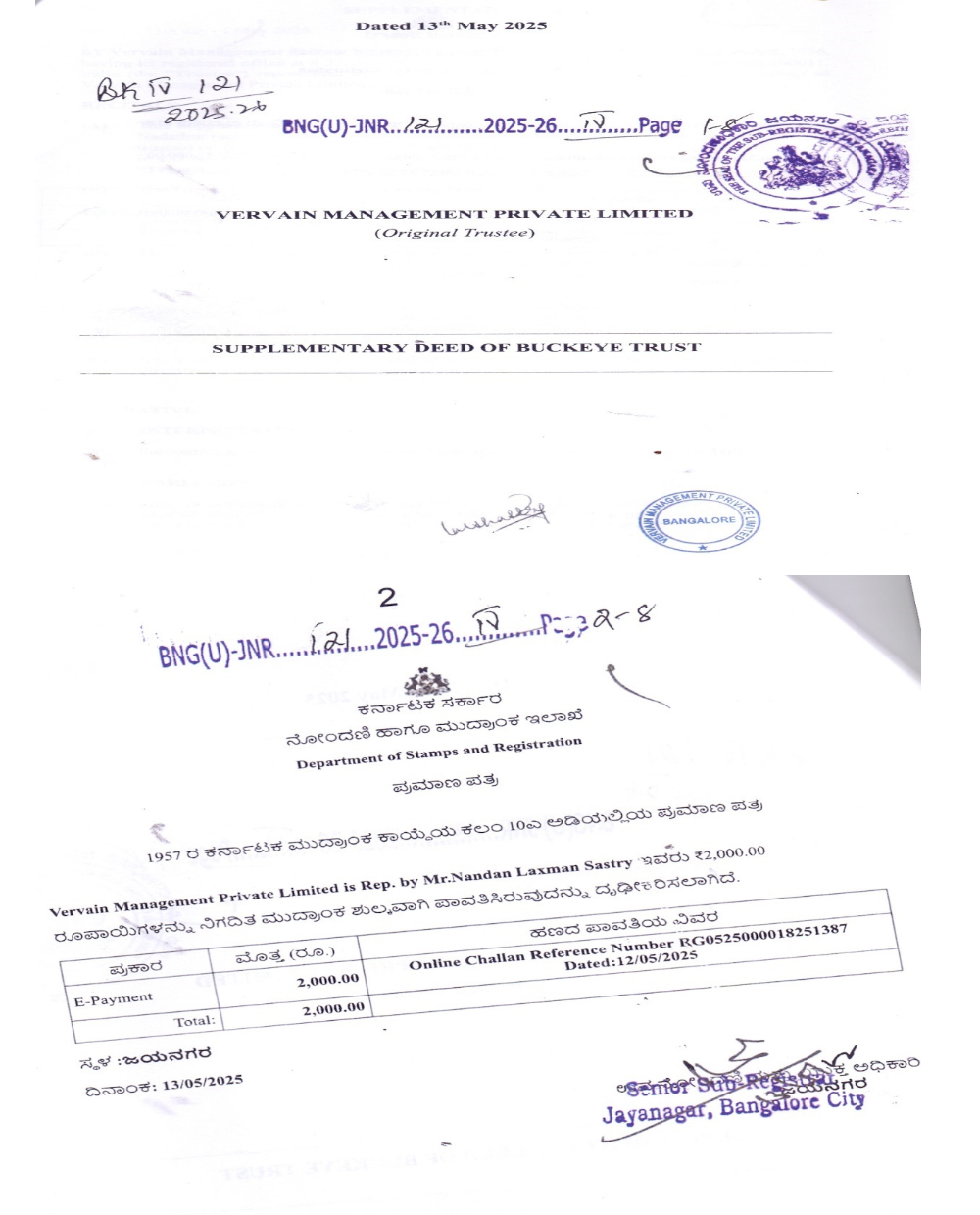

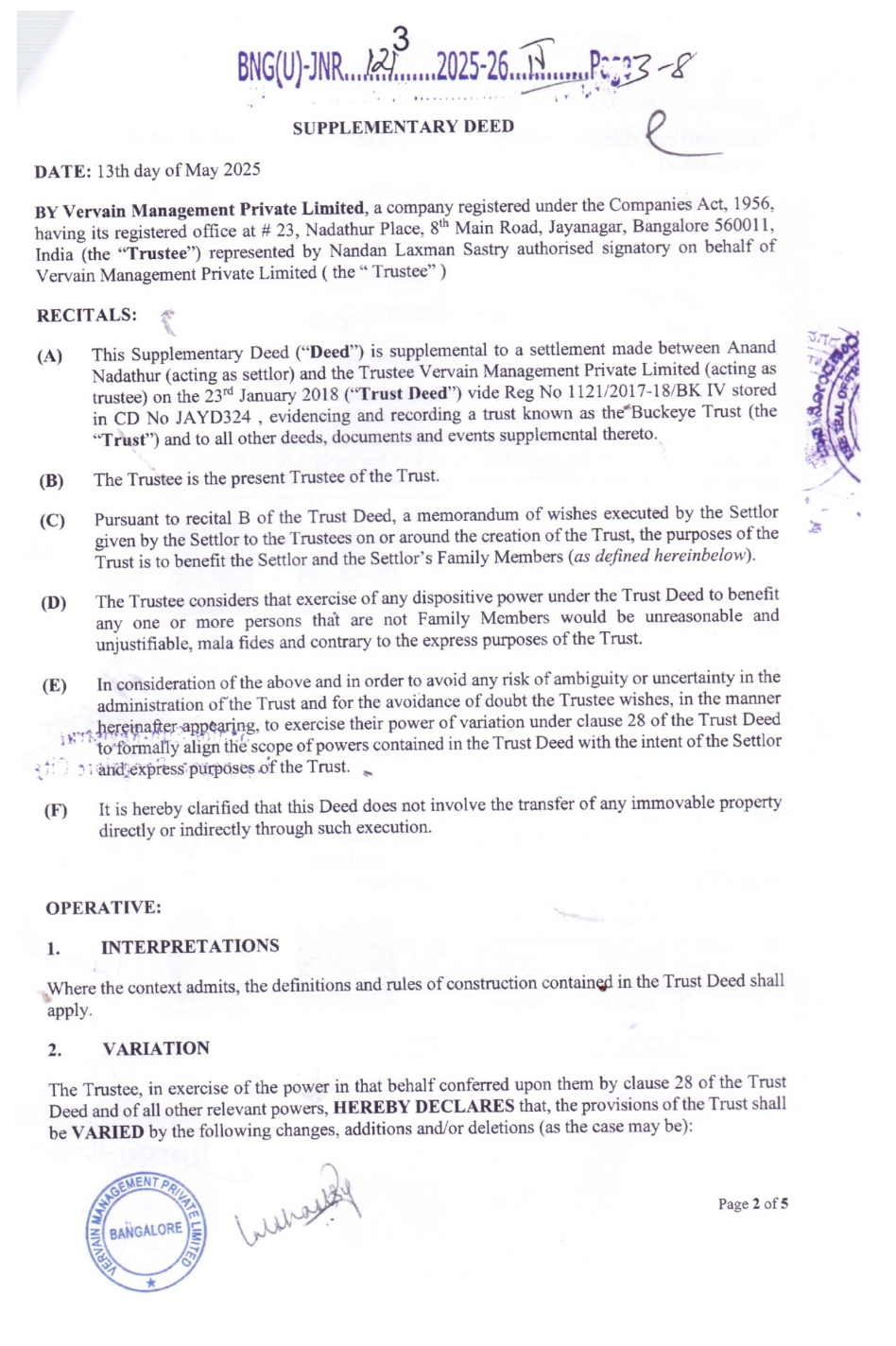

3. The brief facts of the case are that the assessee is a Private discretionary trust under the provisions of the Indian Trusts Act, 1882 created by virtue of a trust deed executed on 23.01.2018 between Mr. Anand Nadathur, being the Settlor, and Vervain Management Private Limited, being the Trustee. On 31.03.2018 the settlor, out of natural love and affection for the beneficiaries, settled assets amounting to Rs.669,27,63,437/- into the assessee trust pursuant to a duly executed settlement deed. The assessee trust filed its return of income for the assessment year 2018-19 on 30.08.2018 declaring total income of Rs. NIL. Thereafter, the case of the assessee trust was selected for complete scrutiny through CASS on the following issues: -

i) Investments/Advances/Loans

ii) Expenses incurred for earning exempt income

iii) Share Capital/Other Capital

Subsequently, the notices u/s 143(2) and 142(1) of the Act were issued calling upon to furnish the details/clarification in respect of the assessment proceedings. The AO after considering the written explanation/clarification along with the submission in support of the retur

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :