IN THE HIGH COURT OF KARNATAKA AT BENGALURU

S.R.KRISHNA KUMAR, J.

South Indian Oil Corporation – Appellant

Versus

The Assistant Commissioner Central Tax, Bengaluru – Respondent

Writ Petition No. 22068 of 2024

Decided On : 12-12-2025

| Table of Content |

|---|

| 1. overview of the case and petitioner details. (Para 1 , 2) |

| 2. court's examination of procedural compliance and authority. (Para 3) |

| 3. arguments on the basis of section 54(3) of cgst act. (Para 4) |

ORDER :

1. In this petition petitioner seeks the following reliefs:

a) Issue a writ in the nature of mandamus or any other Appeal NO.34-37/2022 and 232-233/2022 GST AC AI DIN-202305570000000056F ORDER-IN-ORIGINAL No. 247-252/ADC-AI/GSTS/2023 dated 23.05.2023 (Annx-A) passed by Respondent as being void, arbitrary, illegal, without jurisdiction, apart from being violative of Articles 265 of the Constitution of India, and to consequently set aside the same and/or pass such further or other order(s) as this Hon'ble Court may deem fit and proper in the circumstances of the case.

b) Grant such other consequential relief as this Hon'ble High Court may think fit."

2. A perusal of the material on record will indicate that the petitioner submitted refund applications for various tax periods pursuant to which show cause notices were issued by the respondent proposing to reject the refund request of the petitioner who submitted replies and the proceedings culminated in the impugned orders rejecting the refund claim of the petitioner whose appeals were also dismissed by the appellate authority. It is an undisputed fact as borne out from the material on record that the petitioner is engaged in the business of procuring various edible oils such as Sunflower oil, Rice bran oil, Cottonseed oil, Palm oil etc., falling under HSN Code 15 on payment of tax at 5%. It is also to be stated that the said edible oils are purchased in bulk in tankers and then packed into various containers bearing the net weight of 250 ml, 500 ml, 1 litre or 5 litre at their premises for selling by way of both business to business and also business to customers at the tax rate of 5% under the same HSN Code 15. Under these circumstances, the petitioner accumulated ITC and sought for refund of the accumulated and unutilised ITC on account of rate of tax on certain inputs being higher than the rate of tax charged on packed edible oil which is the output supply and sought for refund in this regard as per the refund applications filed by the petitioner. The issue as to whether the petitioner would be entitled to refund under identical circumstances came up for consideration before this Court in the case of Indian Oil Corporation Ltd. vs. The Assistant Commissioner of Central Tax in W.P. No. 14414 of 2024 dated 20.08.2024, wherein it was held as under:

“1. In this petition, petitioner seeks for the following reliefs:-

“(A) Issue a writ of certiorari or any other writ or direction or order to quash impugned Order in Appeal bearing No.100-101/2024/ADC-A1/GST issued by Additional Commissioner of GST, Appeals-I, Bengaluru dated: 28.02.2024, enclosed as Annexure-A for the reasons state in the grounds.

(B) Grant such other consequential reliefs as this Honourable High Court may think fit including refund of amounts paid, if any and the cost of this writ petition.”

2. Briefly stated, the facts giving rise to the present petition are as under:

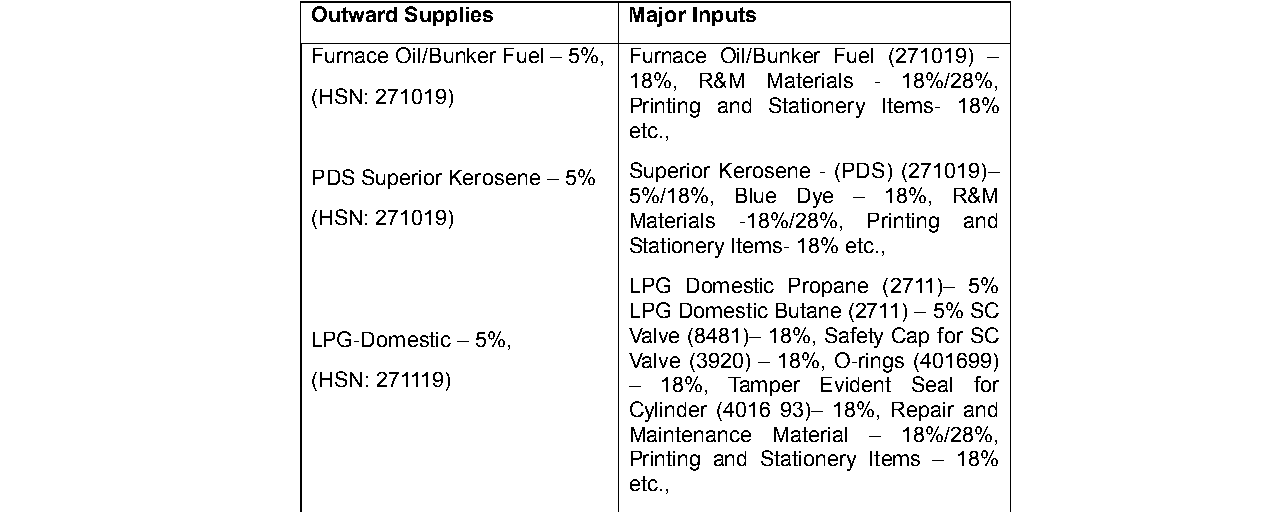

The petitioner - M/s Indian Oil Corporation Ltd., is a Public Sector Undertaking engaged in storage and supply of various petroleum products like petrol, diesel, LPG-Domestic and LPG (Non-Domestic), Furnace Oil, Lubes, Superior Kerosene Oil (SKO) - PDS and petrochemicals. Petitioner maintains terminals/depots for SKO, Bunker fuel and bottling plants for LPG products from where it is stored and then supplied to respective customers. It is stated that LPG consists of various hydrocarbons such as Butane and Propane, which are imported. LPG is transported in bulk through road and pipelines to the petitioner's bottling plant. It is unloaded and bottled in cylinders. The cylinders are thereafter sealed and safety valves are fixed. The said cylinders are then distributed to customers.

2.1 It is contended that the goods supplied by the petitioner attract

Taxpayers are eligible for refunds of accumulated input tax credit even when input and output supplies are identical, as clarified through legislative amendments.

The main legal point established is that the statutory scheme of refund under Section 54(3) of the CGST Act, 2017 applies to cases of accumulation of unutilised input tax credit due to an inverted du....

Input tax credits accrued before the effective date of a notification can be claimed despite subsequent restrictions, as clarified by the court.

Refund of unutilized input tax credit is a strictly statutory right confined to specific situations prescribed by law. It cannot be granted upon business closure unless explicitly enumerated by the l....

The eligibility of a merged entity for ITC refund is recognized under GST, allowing inclusion of export proceeds from previous tax regimes.

The court established that transitional CENVAT credit can be carried forward into the GST regime and utilized for claiming refunds under the CGST Act, rejecting hyper-technical interpretations by aut....

Petitioners entitled to refund of unutilized input tax credit as exporters, while Circular No. 172/04/2022 restricting such claims based on deemed exports deemed inapplicable.

Input Tax Credit cannot be compelled to be reversed without due process, and restoration is required if reversal occurs under duress.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :