IN THE HIGH COURT OF JUDICATURE AT BOMBAY

Sandeep V. Marne, J.

Sangita Sandip Jadhav and ors. - Petitioners

Versus

The State of Maharashtra Through its Secretary Department of Registration & Stamps and ors. - Respondents

Writ Petition No. 4681 of 2024

Decided On : 02-04-2025

(A) Maharashtra Stamps Act, 1958 - Sections 47 and 48 - Refund of stamp duty - Petitioners challenged rejection of refund application for stamp duty paid on Agreement for Sale due to non-handing over of possession - Collector of Stamps and CCRA erred in inferring possession was handed over - Petitioners entitled to refund under both Section 48(1) and Proviso to Section 48(1) - Unjust enrichment if state retains stamp duty. (Paras 1-31)

(B) Legal principles - The court emphasized that the failure of a transaction allows for a refund of stamp duty under Section 47(c)(5) and that the application for refund must be made within the prescribed period. (Paras 19-30)

(C) The court clarified that the Proviso to Section 48(1) creates a sub-category for Agreements for Sale, allowing for an extended period for refund applications if specific conditions are met. (Paras 21-27)

Facts of the case:

Petitioners intended to purchase a flat, paid part consideration, but possession was not handed over, leading to a cancellation of the Agreement for Sale and a subsequent application for refund of stamp duty.

Findings of Court:

The court found that the Petitioners were not handed over possession and thus were entitled to a refund of stamp duty.

Issues: The main issues were whether possession was handed over and the applicability of the refund provisions under the Stamp Act.

Ratio Decidendi: The court ruled that the Petitioners were entitled to a refund of stamp duty based on the failure of the transaction and the specific provisions of the Stamp Act.

Result: The order rejecting the refund was set aside, and the state was directed to refund the stamp duty.

JUDGMENT :

1) Petitioners have filed this petition challenging the order dated 24 June 2021 passed by the Chief Controlling Revenue Authority, Maharashtra State, Pune rejecting Appeal No.133/2020 preferred by them challenging the order dated 23 September 2020 passed by the Collector of Stamps, Satara rejecting their application for refund of stamp duty.

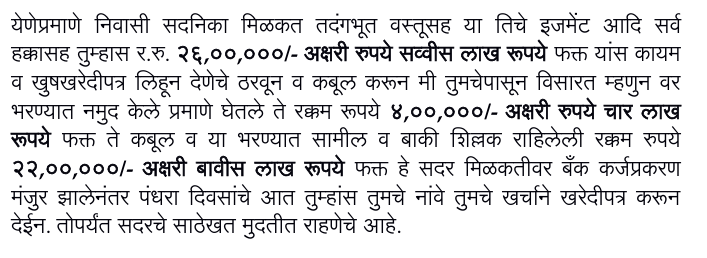

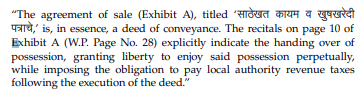

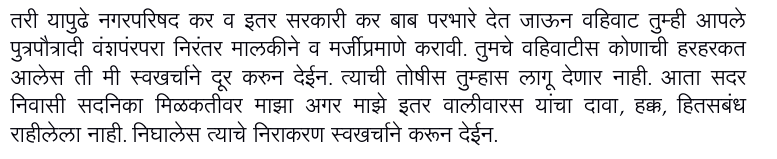

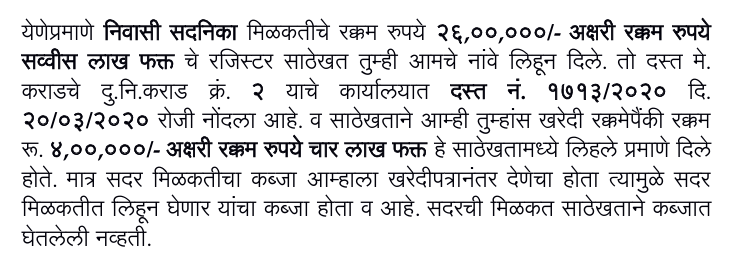

2) Brief facts of the case are that Petitioners intended to purchase Flat Unit No. 7 admeasuring 975 sq. foot (built-up area) in building Rukmini Heights, Kasbe-Karad, Satara. Initially Agreement for Sale was executed between the parties on 19 March 2020, under which the Petitioners paid part consideration of Rs. 4,00,000/- out of the agreed consideration of Rs. 26,00,000/-. The balance was agreed to be paid on sanction of loan. The Agreement came to be registered on 20 March 2020. Petitioners paid stamp duty of Rs. 1,56,000/- and registration fees of Rs.26,000/-, total amount of Rs.1,82,000/-. It is the case of the Petitioners that possession of the flat was not handed over to them. They applied for loan to various financial institutions, which was not sanctioned. Petitioners also faced same difficulties and decided not to go ahead with the transaction and communicated to the vendor that they were not in a position to purchase the flat. Accordingly, Deed of Cancellation came to be executed and registered on 10 September 2020. On 15 September 2020, Petitioners filed application for refund of stamp duty with the Collector of Stamps. The Collector of Stamps however rejected the application by order dated 23 September 2020 referring to a covenant in the Agreement for Sale by inferring that possession of the flat was handed over to the Petitioners. The Collector of Stamps referred to Proviso to sub-section (1) of Section 48 of the Maharashtra Stamps Act, 1958 (Stamp Act) and held that refund was impermissible on account of handing over of possession of the flat in pursuance of the Agreement for Sale.

3) Petitioners preferred Appeal before the Second Respondent under the provisions of Section 53(A) of the Stamp Act. The Appeal is however rejected by order dated 24 June 2021. The Petitioner has accordingly filed the present petition challenging the orders passed by the Collector of Stamps on 23 September 2020 and by the Inspector General of Registration and Controller of Stamps and Chief Controlling Revenue Authority (CCRA) dated 24 June 2021.

4) Mr. Nargolkar, the learned counsel appearing for the Petitioner would submit that Respondent No.3 has grossly erred in rejecting the application for refund by erroneously inferring that possession of the flat was handed over to the Petitioners in pursuance of the Agreement for Sale. That flat’s possession was not handed over with execution of the Agreement for Sale. That the Deed of Cancellation specifically records so. That it is otherwise inconceivable that Flat’s possession would be handed over on payment of just 15% of agreed consideration.

5) Alternatively, Mr. Nargolkar would submit that even if possession of the flat is treated to have been handed over to the Petitioners, the application for refund of stamp duty was made under sub-section (1) of Section 48. That the application was made within the time limit of six months prescribed under sub-section (1) of Section 48. That the Proviso makes a special exception in case of Agreement for Sale by providing for extended period for making an application for refund of stamp duty. That in the present case, the application for refund was made within a period of six months from the date of execution of Agreement for Sale and that therefore the case would be governed by sub-section (1) of Section 48 and not by Proviso thereto. He would therefore submit that in either of the cases, the Petitioner is entitled to refund of stamp duty,

Refund of stamp duty is permissible under the Maharashtra Stamps Act when the transaction fails, and the application for refund must be made within the prescribed period.

The right to claim a refund of stamp duty is governed by statutory provisions, and failure to comply with the prescribed limitation period without sufficient justification precludes the possibility o....

The application for refund of stamp duty was timely under both the original and amended provisions of Section 48(1) of the Bombay Stamp Act, 1958.

Refund of Stamp Duty – Denying a legitimate refund solely on technical grounds of limitation, fails to strike equitable balance ordinarily expected in fiscal or quasi-judicial determinations.

The court established that the right to claim a refund of stamp duty is not extinguished by the expiration of the statutory limitation period, emphasizing the need for a merits-based evaluation.

The court clarified that Section 47 of the Maharashtra Stamp Act governs refund claims for spoiled stamps, while Section 48 only sets the limitation period, necessitating an inquiry into the claim.

Failure to comply with registration provisions negates entitlement to refund of stamp duty, as execution of the document fulfills the payment's purpose under the Indian Stamp Act, 1899.

The court may exercise extraordinary jurisdiction to grant refunds of stamp duty on unexecuted instruments, prioritizing equitable outcomes over procedural strictures.

Refund of stamp duty is not permissible when the duty has been utilized for a document that was executed but refused registration due to non-compliance with legal provisions.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :