IN THE HIGH COURT OF JUDICATURE AT BOMBAY

M.S. SONAK, ADVAIT M. SETHNA, JJ.

The Commissioner Of Sales Tax Maharashtra State, Mumbai - Applicant

Versus

M-s Nestle India Ltd. – Respondent

Sales Tax Reference No. 24 of 2010

Decided On : 27-11-2025

JUDGMENT :

M.S. Sonak, J.

1. Heard learned counsel for the parties.

2. This is a reference arising under Section 61 of the Bombay Sales Tax Act, 1959 (“said Act”) made to this Court by the Maharashtra Sales Tax Tribunal (“Tribunal”) to determine the following question:-

“Whether on a true and proper interpretation of entry 18(2) of the Schedule ‘C’ Part II of the Bombay Sales Tax Act, 1959 the Tribunal was correct in holding that the product “Coffee and Instant Drinks Nescafe Premix” sold vide Invoice No. M 81- 32778 dated February 7, 1998 is not covered by the Scope of entry 18(2) of Schedule ‘C’ Part II, but is covered by the Entry 3 of Schedule ‘C’ Part II?”

3. The Statement of Facts accompanying the reference order encapsulates the facts and circumstances in which the above question came to be referred for determination of this Court. The same is transcribed below for the convenience of reference: -

“M/s. Nestle India Ltd is dealing in diverse consumer produce. One of them is Nescafe prepared Mix for vender machines the dealer is registered under Bombay Sales Tax Act, 1959. The dealer had filed a petition before the Commissioner of Sales Tax for seeing determination on the rate of tax on "Coffee and Instant Drinks 'Nescafe Premix' sold vide invoice No. M 81-32779 dated 7.2.1998. It was argued before the Commissioner that in common parlance, the impugned product is known as "Instant Coffee". The product was nothing but instant coffee. Since Instant Coffee could be prepared by making the impugned product in hot water. The dealer argued that the impugned products to be covered under the Schedule Entry C-II-3 which specifically includes "Instant Coffee subject to 8% sales Tax.

The Commissioner of Sales Tax observed that the impugned product is not instant coffee. The product contains ingredients like.

| i | Soluble Coffee Powder | 8.5% |

| ii | Sucrose | 54.0% |

| iii | Partially Skimmed Milk Powder | 37.0% |

| iv | Maltodextrine | 0.5% |

From the aforesaid description, he came to the conclusion that impugned product is in form from which coffee a beverage is prepared. Therefore, the Commissioner held that the "coffee and Instant Drinks Nescafe Premix" would be powder from which no alcoholic beverages are prepared and covered by Schedule Entry C-II-18(2) liable for sales tax at the rate of thirteen paise in a rupee.

Being aggrieved by the order passed by the Commissioner under section 52(1)(c) of the Bombay Sales Tax Act, 1959, the dealer filed appeal before the Maharashtra Sales Tax Tribunal. The Tribunal relied on the Supreme Court Judgment in the case of M/s. Forage & Co. Vs. Municipal Council of Greater Bombay, JT 1999 (9) SC 57. In which, Supreme Court held that the concept of quantity was not at all decisive of the matter.

The Tribunal set aside the D.D.Q. Order passed by the Commissioner and held that the Coffee and Instant Drinks Nescafe Premix is covered by the Schedule Entry C-II-3 of the B.S.T. Act liable for sales tax at the rate of eight paise in a rupee.”

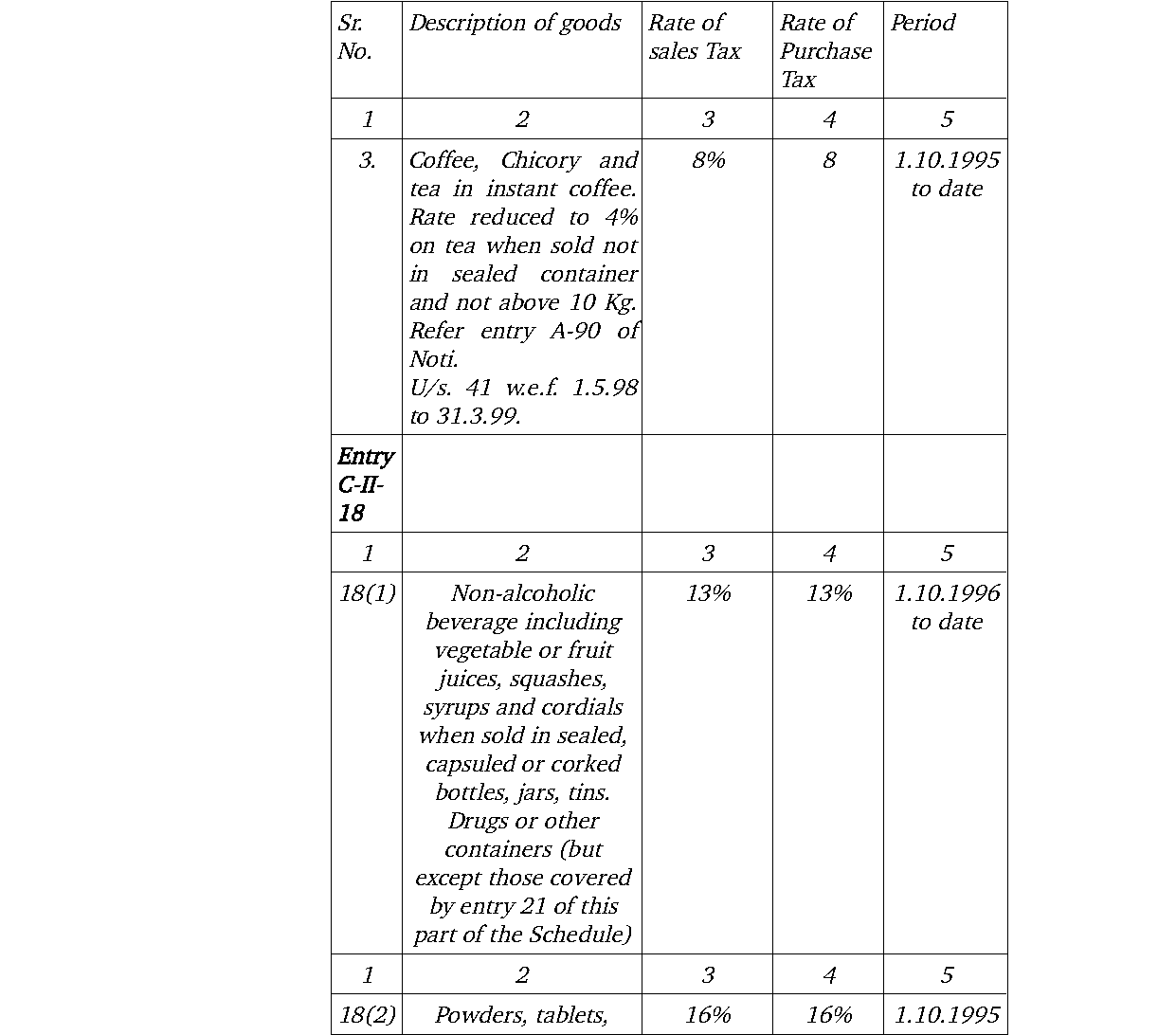

4. To determine the above question, we must refer to Entries C-II-3 and C-II-18 in the Schedule to the Bombay Sales Tax Act. The two competing entries read thus :-

“Entry C-II-3

5. In this case, we are concerned with the classification and consequently the determination of tax rate for the respondent’s product “Nescafe premix”. There is no dispute that this product is used for preparing Nescafe through a vending machine by simply pouring hot water into the premix. There is also no dispute about the contents of the premix i.e. Soluble Coffee Powder 8.5%, Sucrose 54.0%, Partially skimmed milk powder 37%, Maltodextrin 0.5%.

6. Therefore, the question which arises for our determination is whether the above product could be classified under Entry C-II-3 thereby attracting tax of 8% or the same was classifiable under Entry C-II-18 (2), thereby attracting a tax of 16 %.

7. By judgment and order dated 8 December 1998, the Commissioner of Sales Tax determined that the product would be governed by Entry C-II-18(2). On an ap

Classification for sales tax purposes must adhere to the common parlance standard, prioritizing consumer understanding over strict technical definitions.

The classification of beverages under VAT must align with common understanding; 'Sharbat Rooh Afza' qualifies as a fruit drink under Entry 103 based on its essential character.

Classification of imported goods under customs law must adhere to statutory definitions and general rules, emphasizing product characteristics over intended use, especially when 'use' is not explicit....

The court established that the common parlance test is the appropriate standard for interpreting tax classifications in the absence of statutory definitions, reinforcing the principle that tax laws m....

The main legal point established in the judgment is the application of the 'common parlance test' and the commercial understanding of terms in tax provisions to determine the classification of goods ....

Processed goods such as pineapple slices and fruit cocktail do not qualify as 'fresh fruits' under the common parlance test for sales tax exemption.

The main legal point established in the judgment is that the specific entry overrides the general entry, and the burden of proof lies with the Revenue to establish the classification of goods under t....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :