IN THE HIGH COURT OF JUDICATURE AT BOMBAY

M.S. SONAK, ADVAIT M. SETHNA, JJ.

The Commissioner of Sales Tax, Mumbai - Applicant

Versus

Sudha Instant Soft Drinks and Essences, Nagpur – Respondent

Sales Tax Reference No. 3 of 2010 In Reference Application No.68 of 2004

Decided On : 04-12-2025

JUDGMENT:

M.S. SONAK, J.

1. Heard M. Mishra for the Applicant.

2. This Reference under Section 61 of the Bombay Sales Tax Act, 1959 (said Act) refers the following question of law to this Court for its determination:

“Whether on the facts and circumstances of the case, is the Tribunal justified in holding that the goods like pineapple slices, pineapple tidbits, fruit cocktail preserved in sugar syrup and canned in vacuum sealed tin containers are fresh fruits and are covered by the scope of the entry A-23 of the Bombay Sales Tax Act and hence not liable to tax?”

3. The facts and circumstances which give rise to this Reference have been set out in the statement of facts accompanying the Reference. (See pages 10 to 13). Accordingly, we do not reproduce those facts and circumstances in detail in this judgment and order.

4. The Assessee is engaged in the manufacture and sale of juices, instant soft drinks, compounds, powders, essences, etc., and is duly registered under the provisions of the said Act. The Assessee also manufactures various processed food items such as orange juice, tomato juice, mixed fruit jam, pineapple juice, mango juice, pineapple tidbits, tomato purée, pineapple slices, sweetcorn, etc.

5. The record shows that the Asseessee had been granted exemption under the 1979 Scheme of Incentives in relation to the payment of sales tax for the manufacture of certain products. However, in the assessment for the period 1991- 1992, exemption benefits were disallowed in the context of items like tomato juice, mixed fruit jam, pineapple slices, sweet corns, etc., because these products were not explicitly mentioned in the eligibility certificate as the class of goods/products manufactured by the unit eligible for exemption benefits. In the above regard, a dispute arose whether the goods like pineapple slices, pineapple tidbits, fruit cocktail preserved in sugar syrup and canned in vacuum sealed tin containers could be classified as ‘fresh fruits’ covered by the scope of Entry A-23 (as it then stood) of the Bombay Sales Tax Act for levy of nil tax or claim of exemption.

6. The Maharashtra Sales Tax Tribunal (Tribunal), by relying upon the decision of the Hon’ble Supreme Court in the case of Deputy Commissioner, Sales Tax (Law) Board of Revenue (Taxes) Ernakulam Vs. Pio Food Packers, [1980] 3 S.C.R. 1271 has held that the case in question could be classified as ‘fresh fruit’ for Entry A-23 and accordingly, held in favour of the Assessee. It is from this order that the present Reference arises.

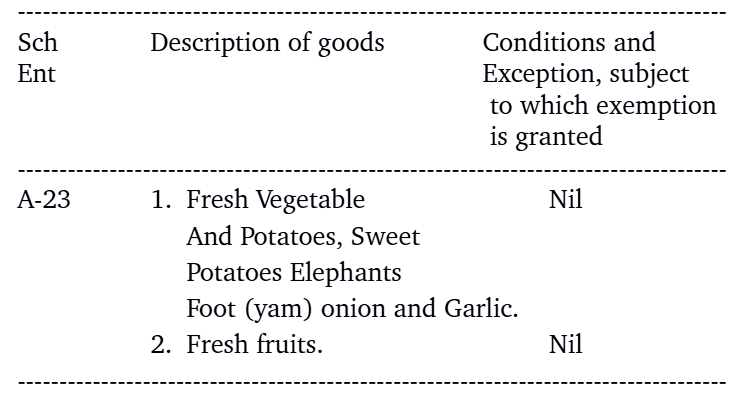

7. Entry A-23, as it then stood, read as follows:

8. For determining whether the goods like pineapple slices, pineapple tidbits, fruit cocktail preserved in sugar syrup and canned in vacuum sealed tin containers are ‘fresh fruits’ covered by the scope of Entry A-23, we are required to apply the common parlance test as was held by this Court in the case of The Commissioner of Sales Tax, Maharashtra State, Mumbai Vs. M/s. Nestle India Ltd., Decided by this Court on 27 November 2025 in STR No.24/2010.

9. In M/s. Nestle India Ltd. (supra), this Court observed as follows: “The Hon’ble Supreme Court referred to several precedents on the subject and explained the importance of the common parlance test in interpreting taxing statutes, particularly relating to the classification of products. The Court also explained that in the absence of any statutory definition in precise terms, the words, entries and items in taxing statutes must be construed in terms of their commercial or trade understanding, or according to their popular meaning. In other words, they must be construed in the sense that the people conversant with the subject-matter of the statute would attribute to it. Resorting to rigid interpretation in terms of scientific and technical meanings should be avoided in such circumstances. Above such instances, unless, of course, the legislature has expressed a contrary intention.”

10. In the context of whether a coconut (neither tender nor dried but a r

Processed goods such as pineapple slices and fruit cocktail do not qualify as 'fresh fruits' under the common parlance test for sales tax exemption.

The classification of beverages under VAT must align with common understanding; 'Sharbat Rooh Afza' qualifies as a fruit drink under Entry 103 based on its essential character.

Classification for sales tax purposes must adhere to the common parlance standard, prioritizing consumer understanding over strict technical definitions.

The classification of carbonated fruit drinks under Tariff Item 2202 99 20 is upheld, affirming that products with significant fruit juice content cannot be classified merely as aerated waters.

The main legal point established in the judgment is the requirement for reasonable classification in taxation laws, as mandated by Article 14 of the Constitution of India. The court emphasized the ne....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :