IN THE HIGH COURT OF JUDICATURE AT BOMBAY

SHARMILA U. DESHMUKH, J.

Neepa Real Estates Pvt. Ltd. – Petitioner

Versus

State of Maharashtra and Ors. – Respondents

Writ Petition No. 1395 of 2023

Decided On : 23-12-2025

| Table of Content |

|---|

| 1. facts of mortgage and loan agreements. (Para 2 , 3 , 4 , 5 , 15) |

| 2. arguments regarding application of stamp act. (Para 6 , 7 , 8 , 9 , 12 , 17) |

| 3. court's analysis of section applicability. (Para 10 , 11 , 18 , 24 , 25 , 26) |

| 4. distinction between distinct transactions. (Para 28 , 31) |

| 5. final dismissal of the petition. (Para 35 , 36) |

JUDGMENT :

SHARMILA U. DESHMUKH, J.

1. Rule. Rule made returnable forthwith by consent and taken up for final disposal.

2. The Petition impugns the order dated 22nd December, 2021 passed by Respondent No.2-Revisional Authority in Revision Case No.134 of 2018 arising out of order of Collector of Stamps levying deficit stamp duty of Rs 40,00,000/- alongwith penalty of Rs.32,00,000/-.

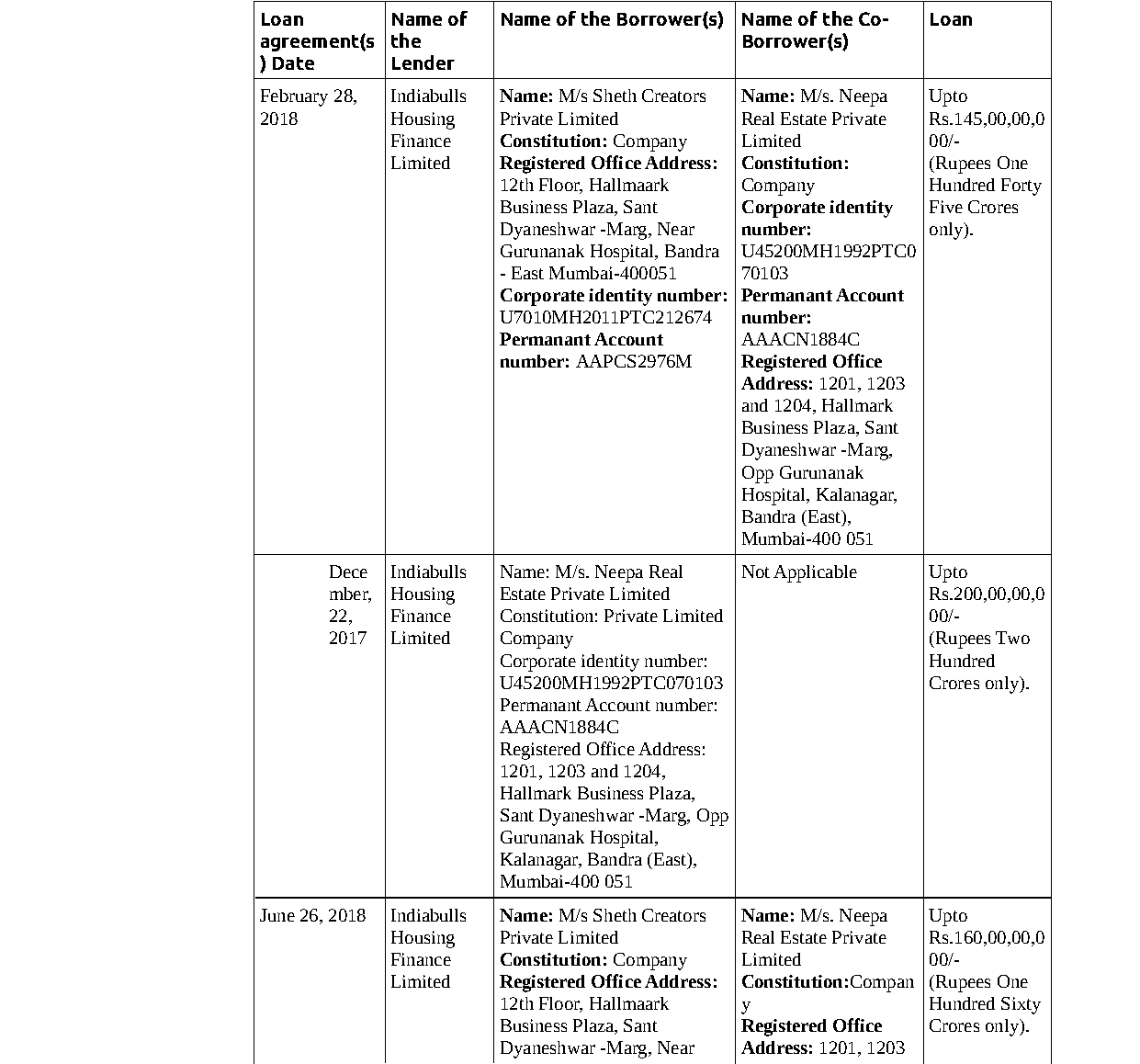

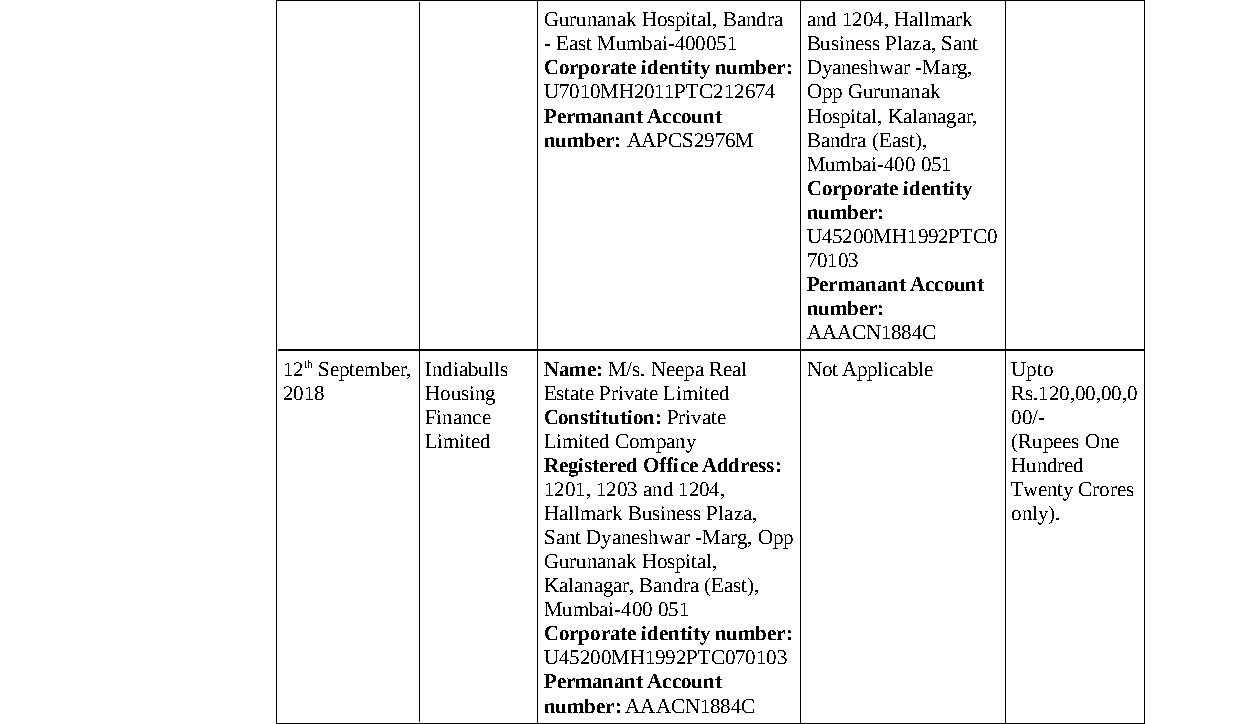

3. The facts required to be exposited as pleaded are that the Petitioner and its group company Sheth Creators Pvt Ltd are in the business of real estate and development and were in need of funds in the year 2017. For availing financial assistance, the Petitioner and Sheth Creaters Pvt Ltd approached Indiabulls Housing Finance Limited (Indiabulls). Four separate loan agreements were executed on 22nd December, 2017 for Rs.200 Crores, 28th February, 2018 for Rs.145 Crores, 26th June, 2018 for Rs.160 Crores and 12th September, 2018 for Rs.120 Crores aggregating to Rs 625,00,00,000/-.

4. The loan agreements mandated creation of mortgage to secure the fulfillment of the obligations including payment of the dues under the loan agreement. A draft of single mortgage deed was lodged for adjudication of stamp duty under Section 31 of the Maharashtra Stamp Act, 1958 (for short, “Stamp Act”). Vide interim order dated 6th October, 2018, the Collector of Stamps adjudicated the stamp duty of Rs.10,01,100/- as due and payable with respect to the mortgage deed, which order was confirmed by order dated 11th October, 2018. Pursuant thereto, the Petitioner paid the stamp duty of Rs.10,01,100/- on 12th October, 2018 and executed the deed of mortgage dated 12th October, 2018 in favour of Indiabulls.

5. Subsequently an audit objection was raised as regards de stamp duty leading to issuance of communication dated 27th October, 2020 by the Respondent No 3 calling upon the Petitioner to pay the deficit stamp duty. In response, the Petitioner addressed two holding letters dated 5th November, 2020 and filed a detailed reply on 4th December, 2020. After hearing the Petitioner, the impugned order dated 22nd December, 2021 was passed by the Respondent No 2 in revision filed under Section 5 3A of the Stamp Act directing the Petitioner to pay the deficit stamp duty and penalty. Hence the present Petition.

6. Mr. Dani, Learned Senior Advocate for the Petitioner submits that one mortgage deed was executed to secure the loans advanced by four loan agreements and the mortgage deed constituted the principal agreement for the purpose of Section 4 of the Stamp Act. He submits that the mortgage deed when lodged for adjudication was rightly adjudicated for payment of stamp duty of Rs 10,01,100/- under Article 40(b), 48(d), 5(h)B and 35 read with Section 6 of the Stamp Act, which stamp duty was duly paid. He submits that the principle agreement was the mortgage deed and the ancillary agreements being loan agreements formed part and parcel of one single transaction and could not be charged separately. He would point out Schedule III of the mortgage deed setting out details of the four loan agreements secured by the mortgage deed as principal document which indicates that all documents are part of the same transaction. He submits that authorities have considered the four loan agreements and the mortgage agreement as separate instruments and have assessed the stamp duty independently which is contrary to of the Stamp Act.

7. He submits that the mortgage deed and loan agreements do not constitute separate distinct matters or transactions and therefore Section 5 of Stamp Act is not applicable. He would further submit even if of the Stamp Act is applie

The mortgage deed securing multiple loan agreements constitutes distinct transactions requiring separate stamp duty assessments under Section 5 of the Stamp Act.

Unregistered agreement for sale with possession, stamped as conveyance under amnesty, is principal instrument under Section 4; subsequent registered sale deed is other instrument attracting fixed dut....

Determination of stamp duty – In matters of stamp duty, decisive factor is not nomenclature assigned to instrument, but substance of rights and obligations it embodies – Court is duty-bound to ascert....

Stamp duty under the Indian Stamp Act applies only to written instruments evidencing agreements; oral agreements do not create a taxable event.

In Court-ordered sales, stamp duty applies only to the sale consideration, not to market value, as established by the Transfer of Property Act.

Stamp duty leviable on single NCLT sanction order of composite amalgamation as instrument, not underlying transactions; Section 5 inapplicable even for multiple transferors.

Stamp duty is on instrument and not on transaction – For several documents to form part of a single transaction, there must be a transaction in furtherance of which several other documents are execut....

The court affirmed that all components of the sale, including outstanding mortgage obligations, must be considered for stamp duty valuation, adhering strictly to statutory definitions.

Allowance for spoiled stamps – As per tenor of instrument, hence there was no unjust enrichment of State because stamp duty paid to it was as per provisions of Stamp Act. No doubt, Stamp Act provides....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :