IN THE HIGH COURT OF DELHI AT NEW DELHI

PRATHIBA M. SINGH, SHAIL JAIN, JJ.

Shri Sugan Traders Through It Proprietor Prop. Abhishek Bindal – Petitioner

Versus

Commissioner Of Central Goods And Services Tax And Ors. – Respondents

W.P.(C) 11091 of 2025 & CM APPL. 45639 of 2025

Decided On : 11-08-2025

| Table of Content |

|---|

| 1. petitioner challenges the demands raised against them. (Para 4 , 5) |

JUDGMENT :

Prathiba M. Singh, J.

1. This hearing has been done through hybrid mode.

2. The present petition has been filed by the Petitioner challenging the order dated

3. On behalf of the Petitioner, two submissions have been made by the ld. Counsel. Firstly, the reply dated 30th August, 2024, which has been filed by the Petitioner to the two Show Cause Notices dated 5th August, 2024 which led to the passing of the impugned orders has not been considered by the Departments.

4. Secondly, it is submitted that the personal hearing was also attended by the Petitioner, but the same does not find a mention in the impugned orders. In addition, the plea of limitation has also been raised by the Petitioner.

5. Coming to the plea of limitation, it is seen that both the impugned orders are dated 1st February, 2025, however, but it appears that the DRC-07 was uploaded on 9th February, 2025 on the GST Portal of the Petitioner.

6. Mr. Harpreet Singh, ld. Sr. Standing Counsel submits that the impugned orders were issued by the GST Department within the prescribed limitation period, however, due to a technical glitch, they may have been uploaded on the GST Portal on a later date.

7. Be that as it may,insofar as the reply dated 30th August, 2024,which has been filed by the Petitioner to the two Show Cause Notices dated 5th August, 2024 is concerned, the impugned order dated 9th February, 2025 itself records as under:

“4. SUBMISSIONS OF THE NOTICEES AND RECORDS OF PERSONAL HEARING:

Following the principle of natural justice, the noticees were granted personal hearings (PH) on 21.11.2024, 16.12.2024 & 26.12.2024. However, replies from Noticee No. 14, 70 and 86 were received whereas for rest of the noticees neither the noticees nor any of their authorized representatives appeared before the Adjudicating Authority for personal hearing on the said dates. Thus, on the basis of available facts and records, I proceed to examine the instant case.

5. DISCUSSION & FINDINGS:-

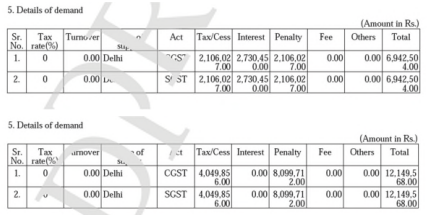

5.1 I have carefully gone through the facts of the case, available case records and the allegations as per the subject SCN. It is seen that the Noticees had not submitted any written submission and also did not appear for personal hearing. Personal Hearings were granted on 21.11.2024, 16.12.2024 & 26.12.2024. However, replies from Noticee No. 14, 70 and 86 were received which have been duly considered. As per reply of Noticee No. 70 & 86 the amount mentioned below has been deposited:

| Noticee No. | Name of the taxpayer | Tax (in Rs.) | Interest (in Rs.) | Penalty (in Rs.) | DRC-03 ARN no. |

| 70 | CREATIVE INDUSTRIES | 2,94,658/ - | 1,59,114/ - | 44,198/ - | AD070221011382 T |

| 86 | AAR BEE ENGINEERING WORKS | 1,31,406/ - | 70,960/- | 19,710/ - | ADO70221011376 N |

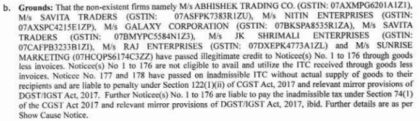

For Noticee No. 86, I find that vide their reply dated 03/01/2025 received on 06/01/2025 to the DRC-01 in the matter, the taxpayer submitted various points i.e. that Section 74 was not applicable in case of records of the taxpayer as there was no suppression of facts, fraud, mis-statement of malafide intention to evade the tax by the taxpayer; that the taxpayer submitted various case laws in support of their above mentioned claims. Further, I find that the taxpayer submitted point-wise reply to the observations on merit. However, on going thoroughly through the reply/points submitted; case laws quoted by the noticee. In this regard I find that on going through the case laws/submissions made by the party, the provided case laws do not squarely cover all the four corners of this issue as each and every case has different facts and circumstances. In other words, I note that the decision is to be made on case to case basis and the reliance can be placed only when the case facts tally

The existence of alternate remedies under statutory provisions limits the maintainability of writ petitions in tax matters.

The existence of an alternative remedy under statutory provisions limits the maintainability of writ petitions unless exceptional circumstances exist.

The High Court affirmed that the issuance of a consolidated SCN for multiple financial years under the CGST Act is permissible, emphasizing the requirement of statutory compliance and the importance ....

Service of notices via registered email under Section 169(1)(c) is adequate under the Central Goods and Service Tax Act, affirming no jurisdictional error or breach of natural justice occurred.

The issuance of the Show Cause Notice was timely under Section 73 of the CGST Act, and the petitioner was afforded adequate opportunity for a hearing, thereby validating the demand order.

Procedural fairness requires that parties receive adequate notice and opportunity to respond before demands or penalties are enforced by administrative authorities.

Notifications under the GST Act must adhere to procedural requirements, ensuring parties receive fair opportunity to respond to demands initiated by show cause notices.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :