2024:DHC:10004

IN THE HIGH COURT OF DELHI AT NEW DELHI

SWARANA KANTA SHARMA, J.

SGS Infratech Ltd. – Appellant

Versus

Punjab and Sind Bank – Respondent

C.S. (OS) No. 2541 of 2014

Decided On : 24-12-2024

Advocates Appeared :

For the Appellants : Rajeev Mehra, Ekta Kalra Sikri, Ajay Pal Singh, Vikalp Mudgal, Dinesh Gandhi, Prakhar Khanna

For the Respondents : Sudhir Makkar, Girish Verma, Raghav Verma, Mehak Nagar, Umesh Jayant, Aadhya S.

JUDGMENT :

SWARANA KANTA SHARMA, J.

1. This is a suit for recovery instituted by the plaintiff SGS Infratech Limited [hereafter „plaintiff company‟], against the defendant Punjab and Sind Bank [hereafter „defendant bank‟], Digitally Signed seeking recovery of Rs. 2,24,89,361/- along with interest of Rs. 67,46,808/-, along with pendente lite and future interest at the rate of 18% per annum.

THE PLAINTIFF’S CASE

2. The plaintiff company is a public limited company incorporated under the Companies Act, 1956, engaged in the business of construction and similar activities. It is also involved in developing and acquiring commercial properties, earning income either through the sale or rental of such properties. In 2006, the plaintiff company decided to purchase a commercial mall namely Magnum Mall [hereafter „the Mall‟], a fully constructed property with certain shops being rented out, for a total sale consideration of Rs. 147 crores.

3. To finance this purchase, the plaintiff company approached Indian Overseas Bank [hereafter „IOB‟] for financial assistance of Rs. 130 crores. IOB agreed to provide Rs. 80 crores and advised the plaintiff company to seek the remaining Rs. 50 crores from other financial institutions or banks. Consequently, the plaintiff company sought assistance from the defendant bank and Punjab National Bank [hereafter „PNB‟] for Rs. 25 crores each. Both the banks agreed, and based on their confirmations, the plaintiff company re-approached IOB, which issued a sanction letter dated 05.09.2006, sanctioning Rs. 80 crores. The repayment was to be made in 115 installments starting November 2006. To secure this financial assistance, the plaintiff company created securities in favor of IOB.

4. Upon receiving the sanction letter from IOB, the plaintiff company approached the defendant bank and PNB for their respective sanction letters. After conducting due diligence, the defendant bank sanctioned financial assistance of Rs. 25 crores through a sanction letter dated 26.10.2006, while PNB issued its sanction letter on 15.11.2006. The terms of the sanction letter from the defendant bank mirrored those in the IOB‟s sanction letter. All three banks, being nationalized, were governed by the guidelines, circulars, and instructions of the Reserve Bank of India [hereafter „RBI‟].

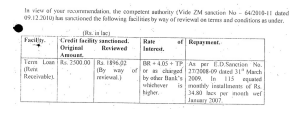

5. Clause 2 of the defendant bank‟s sanction letter specified that the Rs. 25 crore loan would be repaid in 115 equal monthly installments starting one month after the first installment, with interest to be serviced separately as charged. Clause 4(a) provided that the loan would be secured by an equitable mortgage of the Magnum Mall on a pari passu basis. Clause 8(b) stipulated that the loan would be released through IOB, and Clause 8(e) acknowledged that the title deeds of the Mall would be held in IOB‟s custody. Relevant clauses of the sanction letter dated 26.10.2006, cited in the plaint, are set out below:

“Clause 2:

“115 EMI of Rs. 21.75 Lacs to commence from one month after the first disbursement, interest to be serviced separately as and when charged."

Clause 4 (a):

“Commercial security of Magnum Mali CTS No. 231 Moledina Road, Bund Garden, 0pp. Dorabjee's Stores, Camp Pune to equitable mortgage on pari passu basis with Digitally Signed iOB/PNB. iOB for their term loan of Rs. 80 Crores/ PSB for their term loan of Rs. 25 Crores/ and PNB for their term loan of Rs. 25 Crores.”

Clause 8(b):

“Term loan is to be released through iOB only after full tie- up of lease rentals through tripatriate Agreement with IOB and full tie up of remaining amount of term loan from PNB.”

Clause 8(e):

“The title deeds of the property being purchased are received by IOB and mortgage is created on pari-passu basis after compliance of ail statutory requirements /obtaining of Government clearances/NOC etc.”

6. The plaintiff company also created several additional securities in favor of the defendant bank. Further, clause 3 of the sanction letter dated 26.10.2006 outlined the terms under which

Banks must adhere to the terms of sanction letters and cannot unilaterally alter interest rates without borrower consent, constituting a breach of contract.

Provision of Section 24A of 1986 Act mandate observance of limitation period unless sufficient cause with a reasonable explanation is available for condoning delay to be recorded with reasons by Comm....

The Banking Ombudsman must adhere to principles of natural justice, providing a fair hearing before resolving complaints, especially regarding unilateral changes in loan terms by banks.

Banks must adhere to RBI guidelines regarding interest rates and cannot charge excessive rates without borrower consent, ensuring transparency and fairness in lending practices.

A bank cannot unilaterally revise credit facility terms without a breach by the borrower; any appropriation of funds without valid terms is unlawful.

A bank can revise interest rates based on internal ratings without prior notice if contractually permitted, but parties may contest such revisions in appropriate proceedings.

Lenders must adhere to RBI guidelines regarding loan terms disclosure and communication to borrowers; changes without notice violate borrowers' rights.

The court upheld the enforceability of the Loan Agreement, affirming that contractual terms, including default interest, were lawful and agreed upon, dismissing claims of unfair treatment and public ....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :