THE GAUHATI HIGH COURT (HIGH COURT OF ASSAM, NAGALAND, MIZORAM AND ARUNACHAL PRADESH) KOHIMA BENCH

Devashis Baruah, J.

M/s ITI Ltd. – Petitioner

Versus

The Union Of India Represented By The Secretary To The Govt. Of India, Ministry Of Finance Dept. Of Revenue, New Block, New Delhi And Ors . - Respondents

WP(C) 150 of 2024

Decided On : 20-03-2026

| Table of Content |

|---|

| 1. summary of facts, background, and nature of the challenge against cgst orders. (Para 1 , 2 , 3 , 4 , 5 , 6 , 7 , 10) |

| 2. summary of parties' arguments regarding rectification of errors and statutory interpretation. (Para 8 , 9 , 11 , 12) |

| 3. right to rectify bona fide tax reporting errors and due process requirements. (Para 13 , 14 , 15 , 16 , 17 , 18 , 19 , 20 , 21 , 22 , 23 , 24 , 25 , 26 , 27 , 28) |

| 4. retrospective application of section 16(5) of the cgst act regarding input tax credit eligibility. (Para 29 , 30 , 31 , 32) |

| 5. the operative final order setting aside the impugned notice and providing procedural directions. (Para 33) |

JUDGMENT :

Devashis Baruah, J.

Heard Mr. P. Agarwal, the learned counsel appearing on behalf of the Petitioner and Mr. Z. Kulnu, the learned Standing counsel appearing on behalf of the Respondent Nos. 1, 2, 4, 6 and 7.

2. The present writ petition has been filed by the Petitioner seeking various reliefs. The reliefs at Clauses (i) to (ix) being the main reliefs are reproduced herein under:

“(i) An appropriate writ/order/direction including writ of declaration may not be issued declaring the impugned Notification No.49/2019-Central Tax dated 09.10.2019 (Annexure-19) as unconstitutional and unreasonable being violative of Articles 14 and 19(1)(g) of the Constitution of India; and/or

(ii) An appropriate writ/order/direction may not be issued directing the Respondents to act as per para 2 of the Notification No.72/2017-Central Tax dated 29.12.2017, etc. (Annexure-17); and/or

(iii) An appropriate writ/order/direction may not be issued directing the Respondents to accept the GSTR-3B returns without any issue of delay till the time the system is not rectified to enable filing of returns without payment of output tax, and to prohibit the Respondents from proceeding further in such like cases; and/or

(iv) An appropriate writ/order/direction may not be issued declaring the impugned Notification No.23/2017-CT dated 17.08.2017, etc. (Annexure- 12) as unconstitutional and ultra vires to the parent Act; and/or

(v) An appropriate writ/order/direction may not be issued for quashing and setting aside Notification No.09/2023-Central Tax dated 31.03.2023 (Annexure-23); and/or

(vi) An appropriate writ/order/direction may not be issued for quashing and setting aside the impugned Notification No.56/2023-Central Tax dated 28.12.2023 (Annexure-26); and/or

(vii) An appropriate writ/order/direction may not be issued for quashing and setting aside impugned order dated 30.04.2024 (Annexure-30); and/or

(viii) An appropriate writ/order/direction including a writ of prohibition, may not be issued prohibiting the Respondents from proceeding further to deny ITC and to recover tax/ITC in pursuance of the illegal impugned inactions/illegal actions /notifications of the Respondents; and/or (ix) An appropriate writ/order/direction including a writ of prohibition, may not be issued prohibiting the Respondents from treating these as delayed returns and prohibit them from recovering tax by denying ITC on account of delayed filing of returns; and/or

Upon being satisfied and after going through the records of the case Your Lordship’s may be please to make the Rule absolute and/or may pass such other or further Order(s) as Your Lordship’s may deem fit and proper in the facts and circumstance of the present case.”

3. It is relevant to take note of that though various notifications have been put to challenge but the primary challenge is to the order dated 30.04.2024 passed by the Assistant Commissioner, Central Goods and Services Tax, Dimapur Division i.e. the Respondent No.7 under Section 73 of the Central Goods and Services Tax Act, 2017 (for short ‘the CGST Act’).

4. Let this Court take into consideration why the Petitioner is aggrieved by the order dated 30.04.2024 passed by the Respondent No.7.

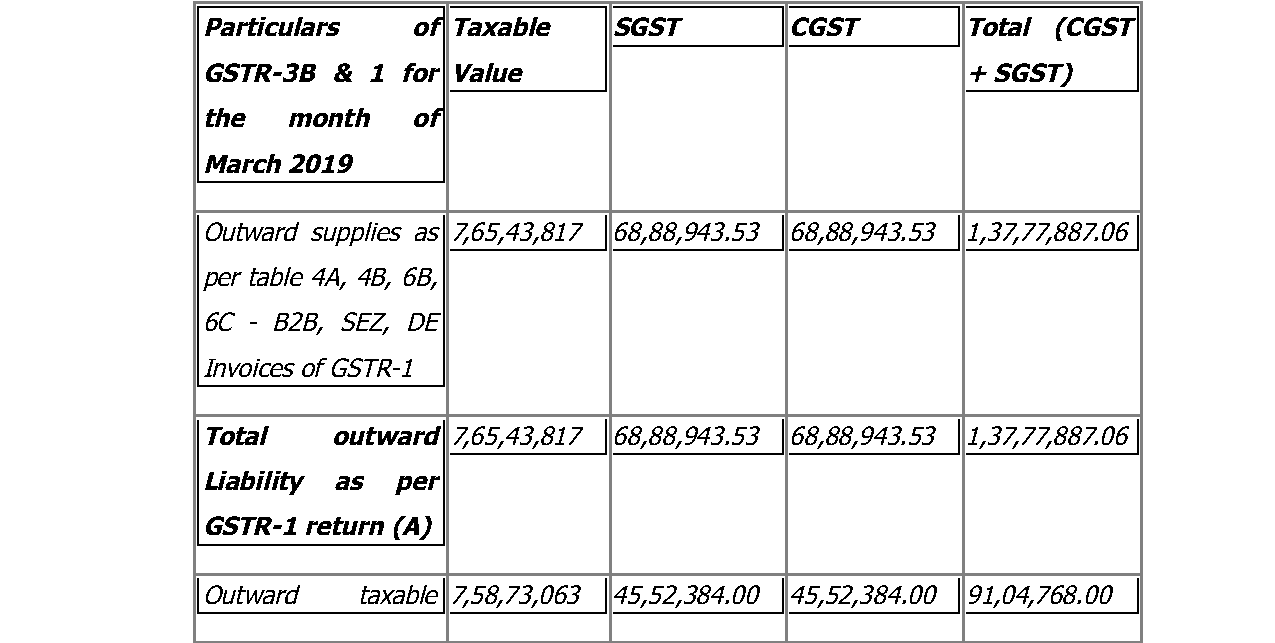

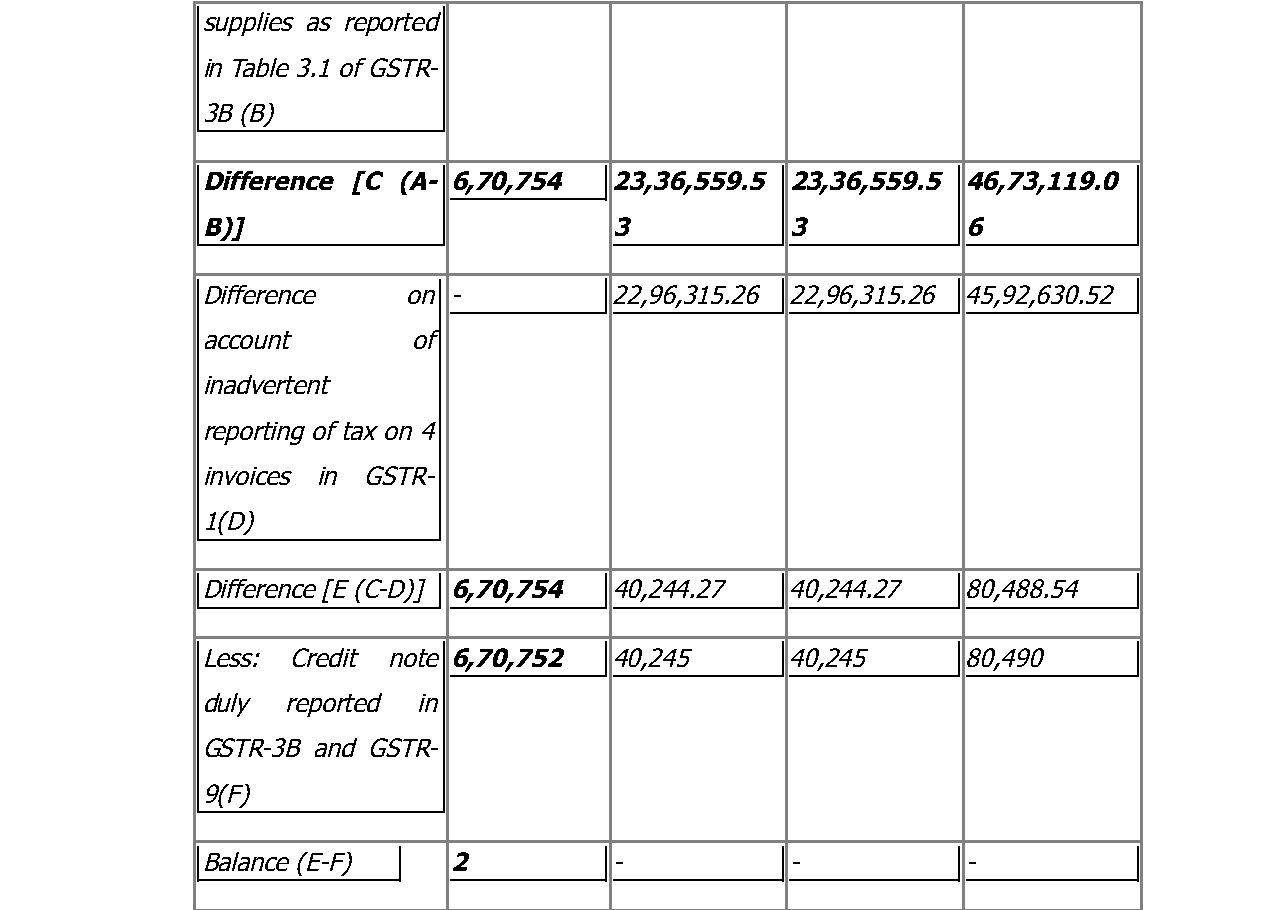

5. The order dated 30.04.2024 relates to the Financial Year 2018-19. The order dated 30.04.2024 was passed for two reasons. First, on account of mi

Bonafide errors in GST returns should not obstruct rectification where no revenue loss occurs, promoting accuracy and fairness under GST provisions.

[The judgment establishes that while Input Tax Credit (ITC) should not be denied solely based on procedural errors, strict compliance with the statutory provisions of the CGST Act is essential for av....

Court ruled that bona fide mistakes in GST returns, especially during early implementation, warrant rectification to prevent undue revenue loss.

The court ruled that system delays in transitioning Input Tax Credit should not prevent a taxpayer from obtaining a refund, emphasizing the need for operational efficiency in tax administration.

Clarifications/circulars issued by the Central Government and of the State Government are concerned they represent merely their understanding of the statutory provisions. They are not binding upon th....

The court ruled that inadvertent misclassification of IGST as CGST and SGST does not constitute excess credit utilization, especially when no revenue loss occurs.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :