IN THE HIGH COURT OF JUDICATURE AT MADRAS

S.M.SUBRAMANIAM, MOHAMMED SHAFFIQ, JJ.

The Inspector General of Registration, Chennai – Appellant

Versus

The National Missionary Society of India, Rep. by its General Secretary – Respondent

W.A. No.125 of 2015, M.P. No. 1 of 2015, C.M.P. Nos. 11247, 11248 of 2025

Decided On : 12-01-2026

| Table of Content |

|---|

| 1. case introduction and background. (Para 1 , 2) |

| 2. details of the subject deed and its implications. (Para 3 , 4) |

| 3. consequences of deficit stamp duty demands. (Para 5 , 6) |

| 4. court's observations on parties' positions. (Para 7 , 9) |

| 5. arguments from the appellants and respondents. (Para 10 , 11) |

| 6. legal standards pertaining to stamp duty. (Para 12 , 13) |

| 7. interpretation of disposition and settlements. (Para 19) |

| 8. analysis of subject deed's purpose and implications. (Para 20 , 22 , 23 , 24) |

| 9. findings and justifications on stamp duty applicability. (Para 25 , 26 , 27 , 28 , 29) |

| 10. final decision and outcome. (Para 30 , 31) |

JUDGMENT :

MOHAMMED SHAFFIQ, J.

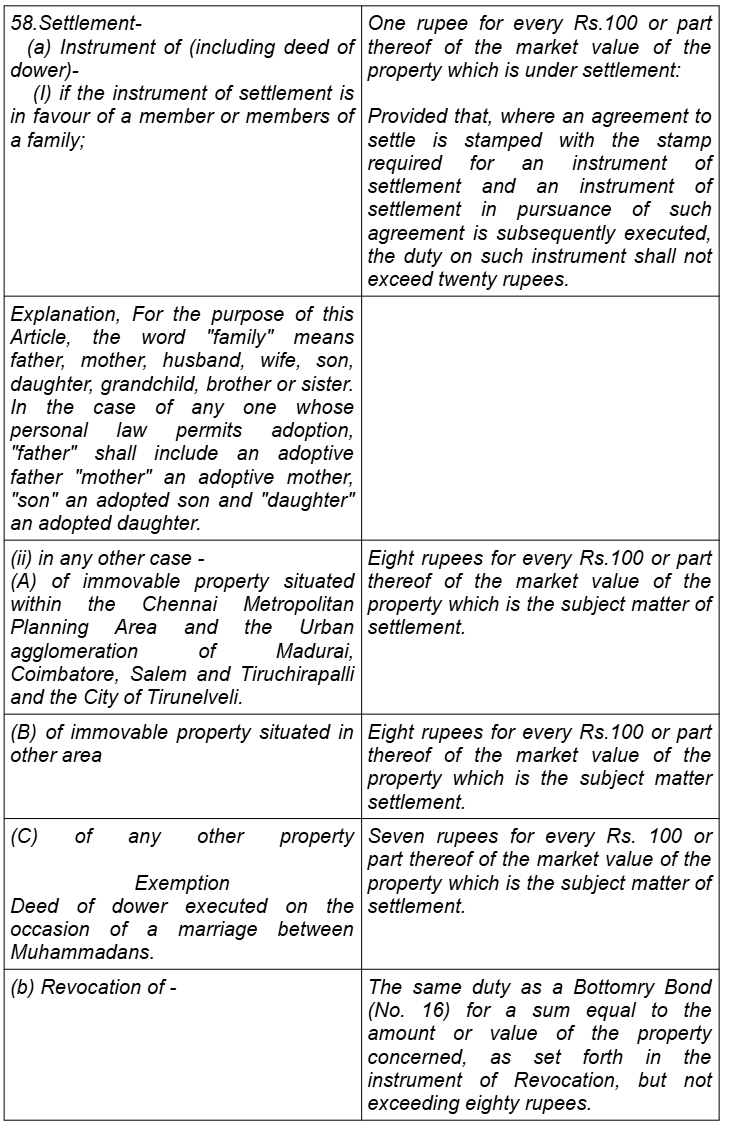

1. Writ Appeal is filed by the State challenging the order of the learned Single Judge dated 04.03.2011 insofar as it set aside the order dated 22.02.2010 and treating/finding Document dated 01.03.1999 bearing No.4240 of 2002 titled as “Transfer of Trusteeship Declaration” dated 26.07.2002 as covered under Article 62(e) of the Stamp Act while rejecting the contention of the State, i.e., appellant herein that the document/Deed of “Transfer of Trusteeship Declaration”, (hereinafter referred to as “Subject Deed”) would be covered under Article 58(a)(ii) of the Indian Stamp Act (hereinafter referred to as 'Stamp Act').

2. Brief facts:-

2.1. For sake of convenience, the parties are referred to as per their rank set out in the writ petition.

2.2. Petitioner is a religious and charitable institution registered under the Societies Registration Act. Petitioner is primarily engaged in charitable works. Christu Kula Charitable Trust a registered Trust (hereinafter referred to as 'Trust'), an Ashram, ran an orphanage to help destitute and deserted children. The purpose of the Trust is to render selfless service to sick and poor, especially, villagers. Trust also had as its object, establishment of Educational Institution. Trust properties / money was, held by trustees who were to be appointed by Sevaks. Trust was to have five trustees, three from Ashram's Sevaks and two from outside the Ashram. Trust Deed provided that if Ashram Sevaks find themselves unable to run one or both of these institutions, i.e., hospital (or) school, they may discontinue either one or both, for such time as may be required. If at any time, Trust is dissolved or discontinued, Trust Deed provides that Rs.3,00,000/-, reserved for the Hospital and Rs.50,000/- for the school, shall be handed over to National Missionary Society of India, i.e., petitioner, to be used for the purposes set out in Appendix 'A' Rule X of Trust Deed.

2.3. Trustees faced difficulties in discharging their obligation primarily due to their old age. It was thus decided to handover the Management or Trusteeship of the Trust in the manner provided under the Trust Deed. Pursuant thereto, a resolution dated 26.02.1999 was passed and “Subject Deed” was executed by the Christu Kula Ashram Trust represented by its Trustees in favour of the petitioner Society, which was referred as Transferee Trustees and represented by its Governing body.

3. The above “Subject Deed” dated 01.03.1999 inter alia provided for the following:

a) Christu Kula Ashram Trust resolved to merge with the National Missionary Society of India.

b) Properties of the above Trust mentioned in the Schedule to the above Deed was to be vested with the Transferee Trust (or) Trustee i.e., the petitioner herein, who shall hold the same for the purposes and objectives of the Trust for which the transferor trustees were holding the same until the date of execution of the said Deed.

4. The Subject Deed was presented for registration by paying duty of Rupees 300/- (Rs.90+210). However, Registering Authority demanded a sum of Rs.70,000/- as deficit stamp duty vide letter dated 26.04.2001. Thereafter, notice dated 04.06.2004 was issued and a further sum of Rs.21,16,779/-, comprising of Rs.19,16,779/- towards duty and Rs.1,53,000/- towards penalty, was demanded. It is stated that the Accountant

The transfer of trusteeship is deemed a 'settlement' under Article 58(ii) of the Indian Stamp Act, affirming that no conveyance occurred, but rather a handing over of management for charitable purpos....

In Court-ordered sales, stamp duty applies only to the sale consideration, not to market value, as established by the Transfer of Property Act.

A scheme of arrangement involving amalgamation or demerger qualifies as an instrument under the Indian Stamp Act, subject to applicable stamp duties.

The court affirmed that all components of the sale, including outstanding mortgage obligations, must be considered for stamp duty valuation, adhering strictly to statutory definitions.

The central legal point established in the judgment is the entitlement of a Charitable Trust for exemption from payment of stamp duty, based on the fulfillment of conditions and the interpretation of....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :