IN THE HIGH COURT OF JUDICATURE AT MADRAS

C. SARAVANAN, J.

M/s Shri Mahalakshmi Metal Mart – Appellant

Versus

The Joint Commissioner of (Appeals) GST and Central Excise, Coimbatore – Respondent

W.P. No. 26417 of 2022, W.M.P. No. 25498 of 2022

Decided On : 11-03-2026

ORDER :

1. The petitioner is before this Court against the impugned order passed by the first respondent in Order No.20/2022-GST (SLM) dated 19.04.2022 in Form GST APL-04.

2. I have considered the argument advanced by the learned counsel for the petitioner and the learned counsel for the respondent.

3. It is noticed that the petitioner has filed this writ petition on 26.09.2022.The petitioner had an alternate remedy to file an Appeal before the GST Appellate Tribunal under Section 112 of the GST enactment. However, the GST Appellate Tribunal was not a reality and it had not been notified. Even as on date, though it has been notified, it has not been fully constituted. Considering the same I shall take up to proceed the writ petition and dispose the same on merits.

4. By the impugned order the petitioners Appeal No.155/2021 dated 30.12.2021 against the Order in Original No.06/2020-2021 dated 24.12.2020 passed by the office of the second respondent has been rejected. The said order in Original No.06/2020-2021 dated 24.12.2020 itself came to be passed in the background of the Show Cause notice issued to the petitioner in serial No. 1/2019/3499 dated 15.11.2019. By the aforesaid order in Original dated 24.12.2020, the following demand was confirmed:

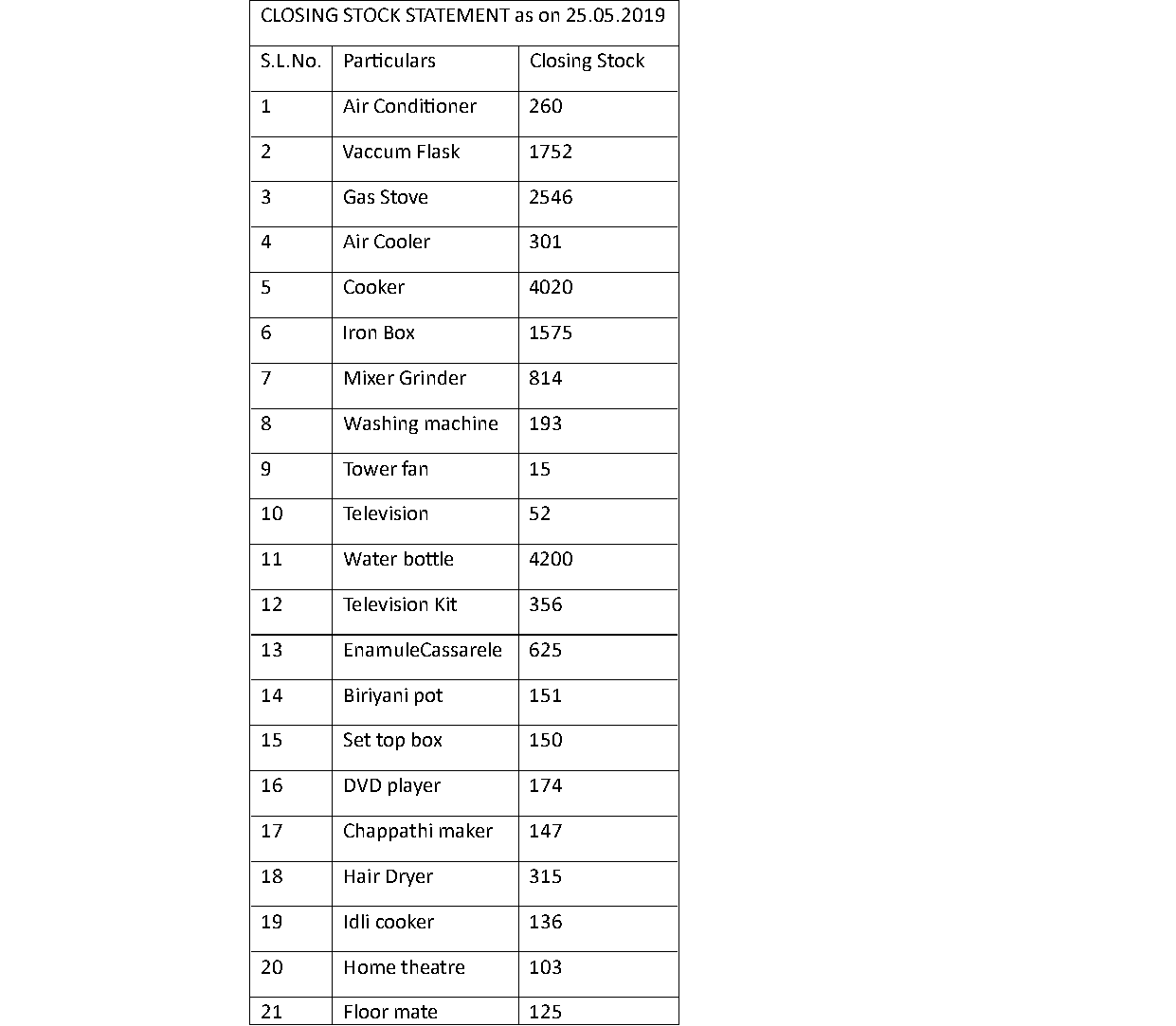

(i) I order to confiscate the goods seized vide Mahazar dated 25.05.2019 at the premised at Shop No.1, Krishnagiri Main Road, Bargur 635 104 Valued Rs.58,28,248/- in terms of Section 130(1)(ii) of CGST Act, 2017;

(ii) I impose a fine of Rs.46,84,730/- (Rupees Forty-Sixlakhseight four thousand seven hundred and thirty) on the tax payer in lieu of confiscation under the first provisio to Section 130(2) of CGST Act, 2017;

(iii) I confirm the demand of Rs.11,43,418/- - (Rs.5,71,709/- CGST and Rs.5,71,709/- SGST) ( Rupees eleven lakhs forty-three thousand four hundred and eighteen only) along with (i) appropriate interest in terms of Section 50 of the CGST Act, 2017 and (ii) a penalty of RS.1,14,342/- (Rupees one lakh fourteen thousand three hundred and forty-two only) under Section 73(9) of CGST,2017; I order the tax payer to pay the same forthwith.

(iv) I impose a penalty of Rs.11,43,418/-) (Rupees eleven lakhs forty- three thousand four hundred and eighteen only) on the tax payer under Section 122(xi) and (xvi) of CGST Act, 2017.

5. The reasons for coming to the above conclusion has been captured in the aforesaid order and the same is extracted hereunder:

19. On a careful reading of the submission dated23.03.2020 furnished by the taxpayer, I find that the seized goods were purchased under proper invoices. The taxpayer defends that he did not register the additional place of business due to ignorant of law and declares that he has not cleared any good from the additional place of business to the customers. However, the taxpayer could not place genuine evidence in this regard. As the goods are stored in the godown ( additional place of business, it is a general practise that the customers are allowed to visit the godown to choose the product as per their will and wish taking into consideration of the brand, quality, model, color etc., of their own choice. Once the customer chooses a particular product as per his choice, it is cleared from the godown to supply the same to the customer. The tax payer contends that the billing is done, in their principle place of business. Presuming that it is happening so also, as per the law, he has to maintain proper accounts in the additional place of business, which he has not done so as required under the provisions of Section 35 of the CGST Act, 2017. At this juncture, the possibility of clearance without proper accounting and evasion of tax cannot be ruled out. In this regard, I find that the taxpayer has not submitted any evidence that such evasion of tax was not happened. Had the taxpayer had not intention to evade the payment of tax, he would have registered the additional place of business. Similarly had the taxpayer registered the additional place of busin

The main legal point established in the judgment is the independence of proceedings for detention of goods under Section 129 and confiscation of goods under Section 130 of the CGST/APGST Act, as expl....

Natural justice requirements necessitate notice to affected parties; however, notice to the driver suffices, supporting reliance on alternative statutory remedies for contesting orders.

Point of law: The extraordinary powers under Article 226 of the Constitution, directing for release of the vehicles or goods, during the pendency of the confiscation, can only be sparingly exercised ....

The court established that confiscation under Section 130 requires prior action under Section 129, and adherence to natural justice is essential in such proceedings.

The court emphasized the need for a thorough inquiry into the petitioner's misuse of the provisions of the GST Act and directed the respondent authority to take proper action in accordance with the l....

Point of Law - Section 68 of the GST Act which empowers the authority concerned to intercept the vehicle and the goods. The said provision of Section 68 is required to be reproduced.

Minor documentation discrepancies do not imply intent to evade tax, and valid transport documents render penalty imposition inappropriate.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :