IN THE HIGH COURT OF ORISSA AT CUTTACK

HARISH TANDON, CJ, MURAHARI SRI RAMAN, J.

M/s. Tansam Engineering and Construction Company – Appellant

Versus

The Commissioner, CGST and Central Excise, Rourkela – Respondent

W.P. (C) No. 15935 of 2025

Decided On : 14-10-2025

| Table of Content |

|---|

| 1. writ petition jurisdictional issue and initial facts. (Para 1 , 2) |

| 2. hearing procedures for the subject matter. (Para 3) |

| 3. arguments concerning legality of dual proceedings. (Para 4) |

| 4. state and central authority roles and jurisdiction. (Para 5 , 6) |

| 5. judicial review of jurisdiction over gst. (Para 7) |

| 6. detailed analysis of judicial standings and precedents. (Para 8) |

| 7. verdict and rationale for the outcome. (Para 9) |

JUDGMENT :

MURAHARI SRI RAMAN, J.

1. Craving to invoke extraordinary jurisdiction under the provisions of Articles 226 and 227 of the Constitution of India, the instant writ application has been filed questioning propriety, legality and tenability of Order-in- Original dated 30.01.2025 passed by the Assistant Commissioner, Rourkela-I Division having jurisdiction of Rourkela-II Circle, Sundargarh exercising power under Section 74 of the Central Goods and Services Tax Act, 2017/the Odisha Goods and Services Tax Act, 2017 (Annexure-1) raising demands vide Summary of Order dated 31.01.2025 in Form GST DRC-07 pertaining to tax period from December, 2017 to March, 2018 (Annexure- 2) and Summary of Order dated 31.01.2025 relating to tax period August, 2018 (Annexure-3).

Facts adumbrated in the writ petition:

2. Relevant facts outlined by the petitioner leading to filing of the writ petition are culled out infra.

2.1. Being assigned to the jurisdiction under the State Tax Authorities having Registration No. GSTIN: 21AAIFT7741F2Z8 under the Odisha Goods and Services Tax Act, 2017/the Central Goods and Services Tax Act, 2017 (collectively be called hereinafter, "GST Act"), the petitioner, a partnership firm carrying on business of supply of service by way of execution of works contract, was adjudicated with liability comprising tax, interest and penalty qua tax period(s) from July, 2017 to March, 2018 under Section 74 of the GST Act pursuant to Show Cause Notice in Form GST DRC-01A dated 02.07.2021 issued by Additional State Tax Officer, Rourkela-II Circle, Sundargarh (be called, "State Proper Officer") vide Order dated 12.04.2023. Assailing said order of adjudication, an appeal bearing No.AD210723002736F under Section 107 ended with dismissal by the Joint Commissioner of State Tax (Appeal), Sundargarh Territorial Range, Rourkela by Order dated 30.01.2024.

2.2. Since the Goods and Services Tax Appellate Tribunal has yet not been constituted, the petitioner approached this Court challenging said order of dismissal of appeal by way of writ petition, registered as W.P.(C) No.13235 of 2024, wherein the following order is passed on 19.06.2024:

"2. It is agreed by learned counsel for the parties that the issue involved in this writ petition has already been decided by a Coordinate Bench of this Court vide Order dated 16.02.2024 passed in W.P.(C) No. 42015 of 2023 (M/s. Maa Tarini Traders v. State of Odisha and others) and batch of writ petitions.

3. In view of the above, this writ petition stands disposed of in terms of the observation and directions issued in M/s. Maa Tarini Traders (supra)."

2.3. In Maa Tarini Traders Vs. State of Odisha and Others , W.P. (C) No. 42015 of 2023 and batch, this Court passed the following Order on 16.02.2024:

"3. It is not at all in dispute that the orders impugned in these writ applications, which have been passed by the Authorities under the Central Goods and Services Tax Act, 2017 (CGST Act)/Odisha Goods and Services Tax Act, 2017 (OGST Act) are appellable under section 112 of the CGST/OGST Act, 2017. It is also not in dispute that because of non- constitution of the Appellate Tribunal as required under Section 109 of the said Acts, the Petitioners are deprived of their statutory remedy of Appeal and the corresponding benefit of sub-sections-8 & 9 of Section 112 of the said Acts.

The Petitioners are desirous of availing the statutory remedy of Appeal under the said provisions. Apparently, acknowledging the absence of constitution of Appellate Tribunal, in exercise of the power confer

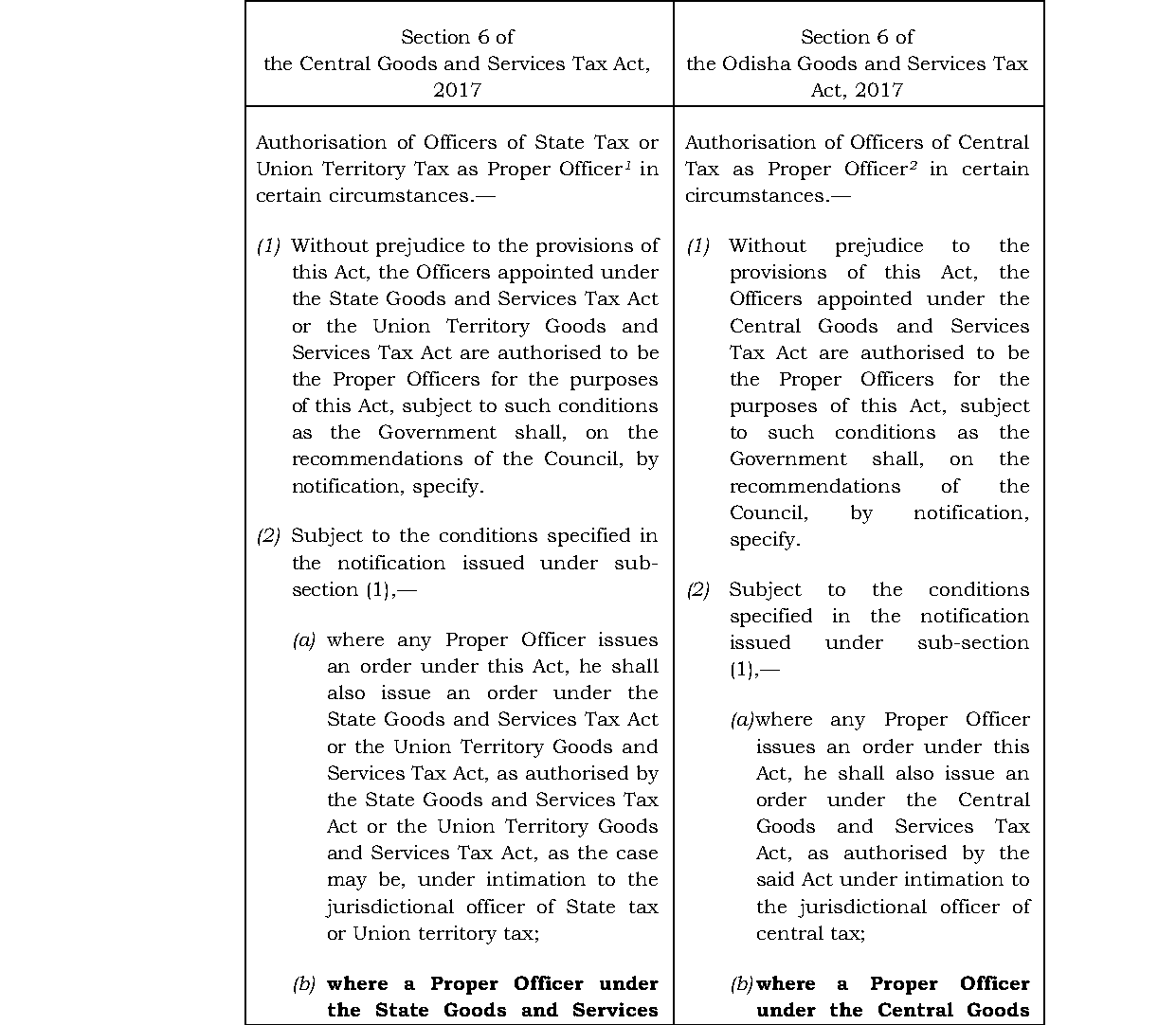

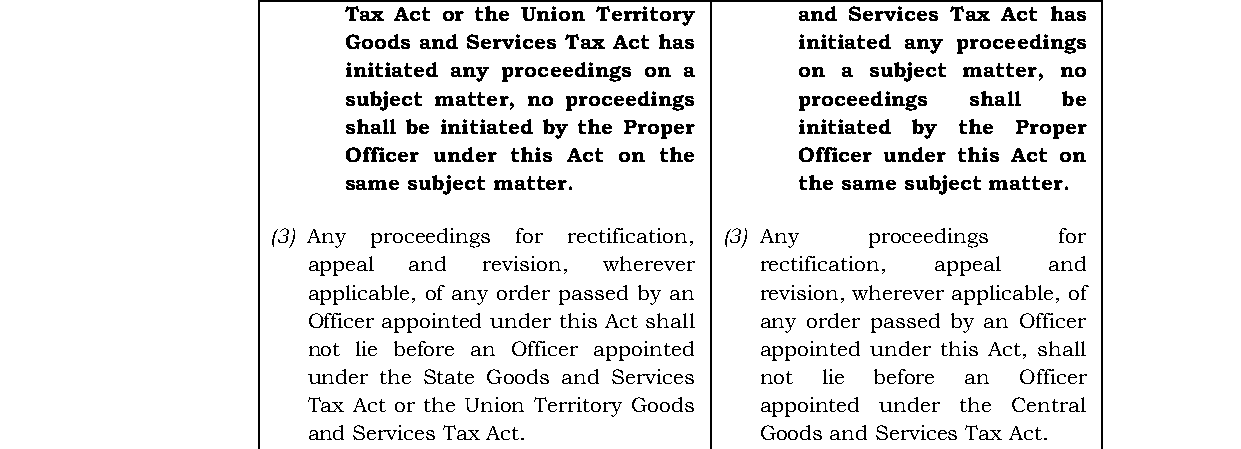

Taxpayer cannot face dual proceedings by Central and State authorities on the same subject-matter under Section 6(2)(b) of the GST Act, establishing a safeguard against double taxation.

Section 6(2)(b) of the CGST Act and the Circular dated 05.10.2018 have limited application and are not a bar to multiple search operations and summons issued by multiple agencies in certain circumsta....

The court ruled that the Circular and Section 6(2)(b) of the CGST Act do not prevent multiple jurisdictions from conducting unified investigations when necessary, reaffirming the court's discretion t....

Proceedings initiated by one authority under the CGST Act must be concluded by that authority; inquiries do not equate to the initiation of proceedings.

The court established that the authority that initiates tax enforcement proceedings retains jurisdiction to complete the investigation, reinforcing the principle of cross empowerment between Central ....

Dual proceedings concerning the same subject matter initiated by State GST authorities after Central GST proceedings are barred under Section 6(2)(b) of the CGST Act.

The jurisdiction under the Central Goods and Services Tax Act prohibits State GST authorities from initiating parallel proceedings once Central GST proceedings have commenced on the same subject matt....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :