IN THE HIGH COURT OF JUDICATURE AT ALLAHABAD

SARAL SRIVASTAVA, J.

M/s Young Style Overseas – Appellants

Versus

State Of U.P. And 2 Others – Respondents

Writ C No. - 26449 of 2022

Decided on : 17-10-2024

Indian Stamp Act, 1899 - Section 47-A - SARFAESI Act, 2002 - Deficiency in stamp duty - Petitioner challenged orders determining deficiency in stamp duty on property sold by public tender - Court held that the sale by tender does not equate to public auction under Article 18 of Schedule 1-B, and the Collector retains authority to assess market value under Section 47-A. (Paras 1, 2, 21, 86, 107)

Facts of the case:

The petitioner, a partnership firm, contested orders regarding stamp duty deficiency on property sold by Canara Bank following default by M/s. Wasan Shoes Limited. The property was sold via tender, but the Collector found undervaluation and imposed additional duties.

Findings of Court:

The court determined that the sale by tender does not constitute a public auction, allowing the Collector to reassess the market value and stamp duty.

Issues: Whether the sale by tender qualifies as a public sale under Article 18 of Schedule 1-B, and the Collector's authority to reassess stamp duty.

Ratio Decidendi: The court ruled that the Collector's powers under Section 47-A are independent and applicable even in cases of public sales by tender, emphasizing the need for accurate property valuation.

Result: Orders set aside; matter remanded for fresh determination. (Paras 106, 107)

JUDGMENT :

Hon'ble Saral Srivastava, J.

1. Heard Sri Shashi Nandan, learned Senior Counsel assisted by Sri Sanjay Goswami and Sri Shreyas Srivastava, learned counsel for the petitioner and Sri M.C. Chaturvedi, learned Additional Advocate General assisted by Sri Chandan Kumar, learned counsel for the respondents.

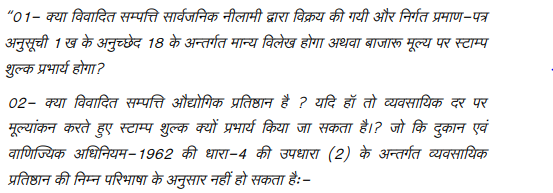

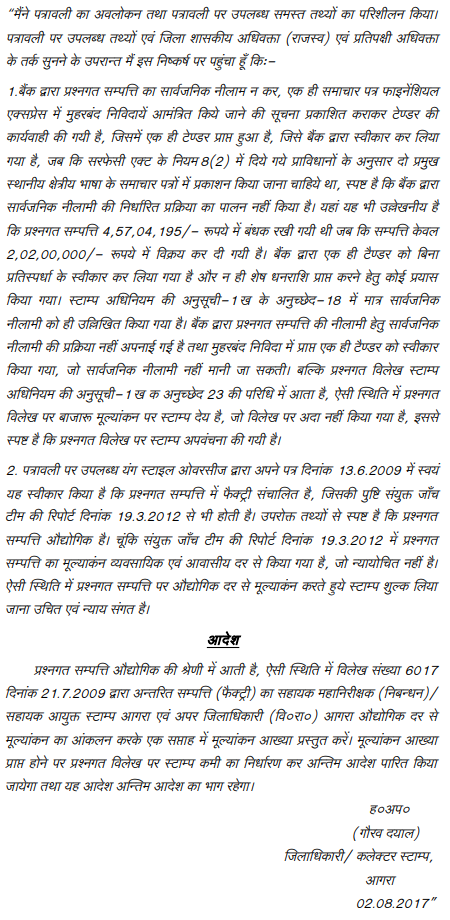

2. The petitioner in the instant writ petition has assailed two orders dated 17.08.2022 and 02.08.2017 passed by the District Magistrate/Collector (Stamp), Agra (hereinafter referred to as ‘respondent no.2’) in Stamp Case No.94 of 2013-14. Respondent no.2 by order dated 02.08.2017 decided the issue no.1 formulated by the Chief Controlling Revenue Authority vide order dated 16.12.2011, and by order dated 17.08.2022, he determined the deficiency in stamp duty to the tune of Rs.1,45,35,270/-

3. The brief facts of the case are that the petitioner is a partnership firm having its registered office in Agra and is primarily dealing in the export of shoes.

4. As per the petition, one M/s. Wasan Shoes Limited was the owner of Khasra No.191 (old) having an area of 2 Bigha, 5 Biswa, and 16 Biswansi, and Khasra No.192 (old) having an area of 3 Bigha, 11 Biswa, and 8 Biswansi situated at Mauja Mangtai, Bodhla, Bichpuri Road, Tehsil and District Agra (hereinafter referred to as 'property').

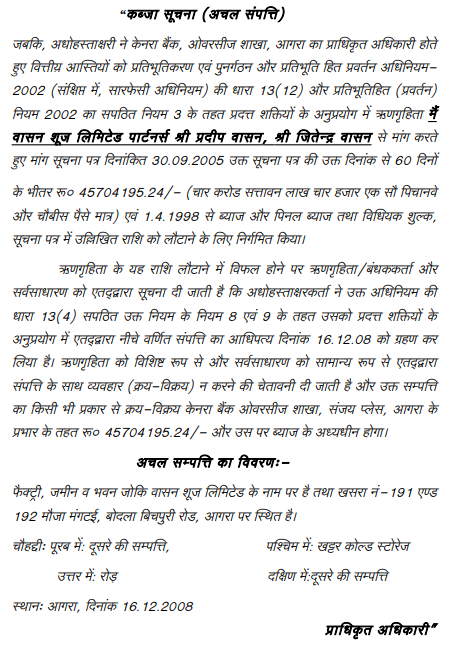

5. The aforesaid properties are bounded on the North by Nala/Bichpuri Road, and on the South, East, and West by agricultural land. M/s Wasan Shoes Limited was running a factory over the aforesaid properties. It had taken financial assistance from the Canara Bank, Overseas Branch Sanjay Place, Agra to run the factory. The aforesaid property and one other property had been mortgaged by M/s. Wasan Shoes Limited with the Canara Bank as a security for the financial assistance. M/s. Wasan Shoes Limited defaulted in repayment of the loan amount of Rs.4,57,04,195.24/-. Consequently, a proceeding under Section 13 and Rules 8 and 9 of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (hereinafter referred to as 'SARFAESI Act, 2002') and the SARFAESI Security Interest (Enforcement) Rules, 2002 (hereinafter referred to as 'Rules, 2002') was drawn against M/s. Wasan Shoes Limited by the Canara Bank (hereinafter referred to as ‘Bank’) for the default in repayment of the loan amount. Accordingly, the Bank took possession of the aforesaid property. The Bank published a notice of possession in two daily newspapers namely, Dainik Jagran and I-Next on 21-12-2008.

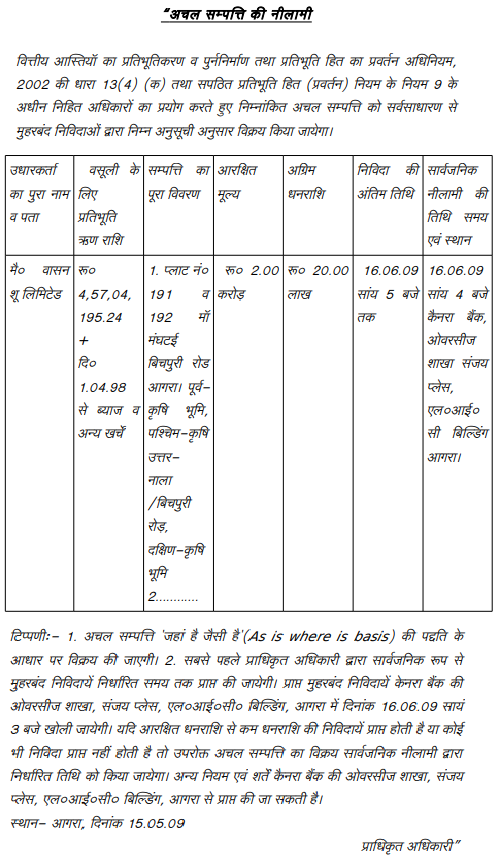

6. Before proceeding with the auction of the property, the Bank had obtained a valuation report from a Government Approved Valuer as mandated under Rule 8(5) of the Rules, 2002. Further case of the petitioner is that as per the report of the valuer, the realisable value of the property was ascertained at Rs.1,95,00,000/-. Accordingly, the Bank kept the reserved price of the mortgaged property at Rs.2,00,00,000/-(Rupees Two Crores) in the auction notice.

7. The Bank, thereafter, invited tenders for the sale of the property by publishing notice in two newspapers notifying the date of the auction of the property. It transpires from the record that there was only a single bid by the petitioner. According to the petitioner, the petitioner offered a bid of Rs.2,02,00,000/- which was accepted by the Bank, and after depositing the aforesaid amount, the sale was confirmed in favour of the petitioner. Consequently, a sale certificate was issued to the petitioner by the Bank in the exercise of power under Rule 9 (6) of the Rules, 2002.

8. It appears that an inspection of the property was conducted by the Additional District Magistrate (Finance & Revenue), Agra on 04.08.2009. On inspection, it was found that a factory is being run over the property, and construction over 4000 square meters has been raised on the property. The report further stated that the aforesaid property has been sold out for Rs.2,02,00,000/-, and the stamp duty has been paid as per Article 18 of Sched

The sale by tender does not constitute a public auction under Article 18 of the Indian Stamp Act, allowing the Collector to reassess market value and stamp duty under Section 47-A.

The Collector of Stamps must adhere to previous valuations and cannot apply new ASR for determining market value in cases remanded for fresh adjudication.

Court auctions dictate the valid market value of properties, precluding stamp authorities from imposing differing assessments of duty.

Stamp duty – In case of a public auction monitored by court, discretion would not be available to Registering Authority under Section 47A of Indian Stamp Act, 1899.

Sale certificates issued by operation of law under SARFAESI do not fall under Section 47-A of the Indian Stamp Act for undervaluation, distinguishing them from conveyance instruments.

Point of Law : Person presenting the instrument is required to disclose the nature of economic activity, industrial development, if any, prevailing in the locality where the property is situated and ....

Registration Authorities cannot question court-determined property valuations under Section 47-A of the Indian Stamp Act, as it undermines judicial authority.

The valuation of property fixed by a court is final and cannot be challenged by registration authorities under Section 47-A of the Indian Stamp Act, as it undermines judicial authority.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :