IN THE HIGH COURT OF ALLAHABAD

PIYUSH AGRAWAL, J.

M/S Jaya Traders Through Its Proprietor Mr. Vishwanath Tiwari – Appellant

Versus

Additional Commissioner Grade-2 And Another – Respondent

WRIT TAX No. - 1022, 1019, 1020, 1021, 1023 of 2021

Decided on : 03-03-2025

(A) IGST/CGST Act - Section 129(3) - Writ petition challenging seizure of goods on grounds of undervaluation and non-genuine documents - Petitioner failed to prove actual movement of goods from West Bengal/Assam to Delhi, leading to justified seizure - Burden of proof lies with the petitioner to establish genuineness of documents and movement of goods. (Paras 4, 20, 22, 23, 29, 46)

(B) Taxation - Seizure of goods - Seizure can be made on grounds of undervaluation if deliberate to avoid tax payment - Petitioner’s reliance on prior judgments was found unpersuasive as they did not address the current case's specifics. (Paras 46, 48)

Facts of the case:

The petitioner, a proprietorship firm, challenged the seizure of goods transported without an e-way bill, claiming the goods were undervalued and that the authorities misinterpreted facts. (Paras 4, 5)

Findings of Court:

The petitioner failed to provide evidence of the actual movement of goods, and the seizure was justified under the Act. (Paras 22, 29)

Issues: Whether the seizure of goods was justified based on undervaluation and the burden of proof regarding the movement of goods. (Paras 20, 22)

Ratio Decidendi: The court emphasized that the burden of proof lies with the petitioner to establish the genuineness of the transaction and the actual movement of goods, which was not fulfilled. (Paras 23, 24)

Result: Writ petitions dismissed.

| Table of Content |

|---|

| 1. petitioner challenges seizure of goods (Para 3) |

| 2. petitioner argues against seizure (Para 4 , 5 , 6 , 7 , 10 , 11 , 12) |

| 3. respondent supports seizure (Para 8 , 9) |

| 4. court reviews evidence (Para 13) |

| 5. court notes lack of evidence (Para 14 , 15 , 16 , 17 , 18 , 19 , 20 , 22 , 23 , 24 , 25 , 26 , 27 , 28 , 29 , 30 , 31 , 32 , 33 , 34 , 35 , 36 , 37 , 38 , 39 , 40 , 41) |

| 6. burden of proof on petitioner (Para 21) |

JUDGMENT :

Piyush Agrawal, J.

1. Heard Mr. Aditya Pandey, learned counsel for the petitioner and Mr. Ravi Shanker Pandey, learned Additional Chief Standing Counsel for the State-respondents.

2. Similar controversy is involved in all the writ petitions, therefore, with the consent of the parties, all the aforesaid writ petitions are being decided by a common judgement treating Writ Tax No. 1022 of 2021, as leading case.

Writ Tax No. 1022 of 2021

3. By means of this writ petition, the petitioner is assailing the order dated 25.10.2021 passed by respondent no. 1 in Appeal No. GST/110/2020-21 (A.Y. 2021-22) under Section129 (3) of IGST/CGST Act .

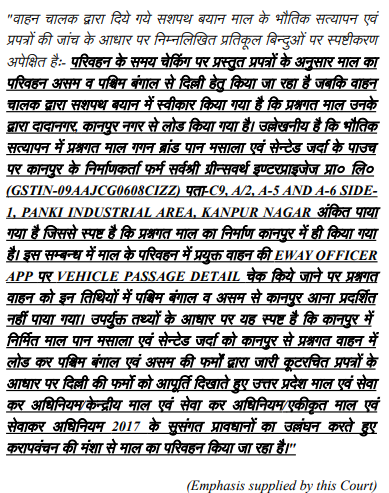

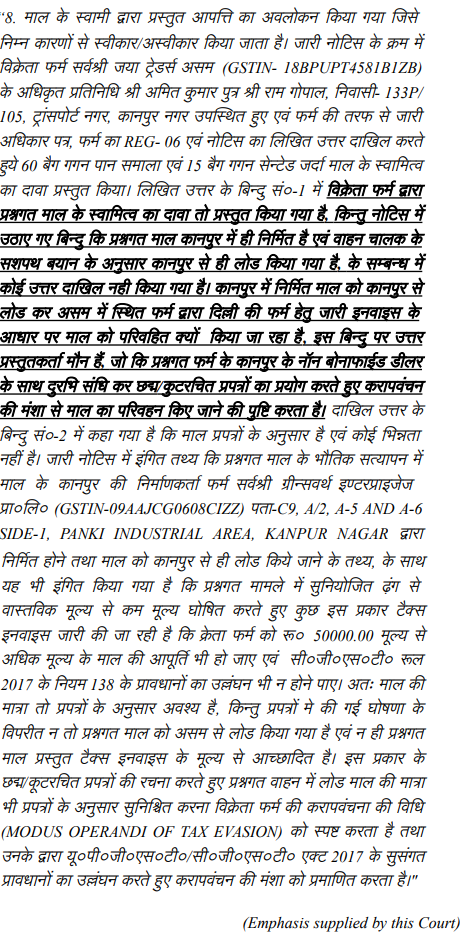

4. Learned counsel for the petitioner submits that petitioner is a proprietorship firm having GSTIN No. 18BPUPT4581B1ZB and is engaged in the business of trading of pan masala and scented tobacco. He submits that in the normal course of business, the petitioner has received an order for supply of pan masala and scented tobacco from various registered dealers situated at Delhi and in pursuance of the aforesaid order tax invoice dated 15.9.2021 was raised on which IGST, cess was charged. Since the value of the goods was less than the prescribed limit, therefore, e-way bill was not generated and through tax invoice nos. 41 to 45 dated 15.9.2021, the goods were transported from West Bengal/ Assam to New Delhi and during its onward journey the same was transshipped at Kanpur where the same was intercepted. The statement of the truck driver was recorded wherein he stated that the goods were loaded from Kanpur and on the said premise, show cause notice was issued to which the petitioner submitted its reply that crossing challan prescribed under the Act was accompanying the goods showing that the goods were transshipped at Kanpur during its onward journey to Delhi and since the value of the goods was less than Rs. 50,000/- e-way bill was not required to accompany the goods, hence the proceedings cannot be initiated. He submits that the goods were seized on the ground of under valuation, which is beyond the power of the detaining / seizing authority. He submits that against the penalty order, an appeal was filed, which has been dismissed without considering the material on record.

5. He submits that the authorities have misperceived certain facts, which are beyond the record. In the seizure proceeding under Section 129 of the Act, the authority cannot seize the goods on the ground of under valuation.

6. In support of his contention, he relied upon the judgements of this Court in the following cases :-

(i) S/s S.K. Trading Co. and another Vs. Additional Commissioner Grade -2 (Appeal) and another ( Writ Tax No. 1464 of 2022 ) decided on 16.3.2023, (ii) M/s Maa Aabe Vs. State of UP , Neutral Citation No. 2024: AHC: 158372 -DB (iii) M/s Shamhu Saran Agarwal and company Vs. Additional Commissioner Grade -2 , Neutral Citation No. 2024:AHC:15975 .

7. He further relied upon the judgements of other High Court :-

(i) Chhattisgarh High Court in the case of K.P. Sugandh Ltd. Vs. State of Chhattisgarh , 2020 NTN (Vol. 74) 372 (ii) Kerala High Court in Best Sellers (Cochin) Private Ltd. Vs. Assistant State Tax Officer, 2021 NTN (Vol 75) -360 and Sameer Mat Industries and another Vs. State of Kerala and others, 2018 NTN (vol 66) -69.

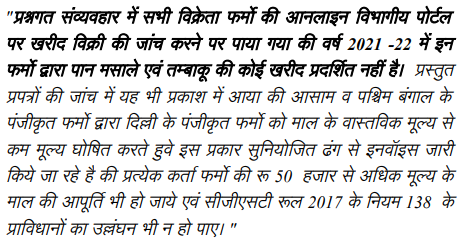

8. Per contra, learned Additional Chief Standing Counsel supports the impugned order and submits that it is simply a case of tax evasion. He submits that goods were detained and seized not only on the ground of under valuation but also on the ground of non-genuine document

The burden of proof lies with the petitioner to establish the genuineness of documents and actual movement of goods; failure to do so justifies seizure under the IGST/CGST Act.

E-way bill is mandatory for transporting goods; failure to carry it raises a presumption of tax evasion, which must be rebutted by the transporter.

Minor errors in e-way bills do not justify detention under Section 129 of the CGST Act if the goods are otherwise properly documented.

Detention and seizure of goods in transit under GST requires clear evidence of contravention; mere discrepancies in documentation cannot justify such actions.

Procedural compliance in tax documentation is mandatory; failure to fill an e-way bill's section warrants penalty under tax law.

For proceedings under section 129 of the UPGST Act, there must be intent to evade tax established; a mere technical breach does not warrant penalties.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :