IN THE HIGH COURT FOR THE STATE OF TELANGANA AT HYDERABAD

P.SAM KOSHY, SUDDALA CHALAPATHI RAO

Anupama Chand – Appellant

Versus

Deputy Commissioner of Income Tax, Central Circle-4, Hyderabad – Respondent

| Table of Content |

|---|

| 1. assessment appeals related to undeclared income. (Para 1 , 2 , 3 , 4 , 5 , 6) |

| 2. contentions relating to jurisdiction of cit(a) and procedural lapses. (Para 7 , 8) |

| 3. arguments regarding service and issuance of notices. (Para 12 , 17 , 24) |

| 4. judicial precedents asserting mandatory service of notice. (Para 13 , 14 , 15 , 18 , 19 , 20 , 21) |

| 5. court analysis of statutory requirements and consequences of non-compliance. (Para 30 , 31 , 32 , 33 , 39 , 40) |

| 6. final judgment on setting aside assessment orders. (Para 41 , 42 , 43 , 44) |

JUDGMENT:

Suddala Chalapathi Rao, J.

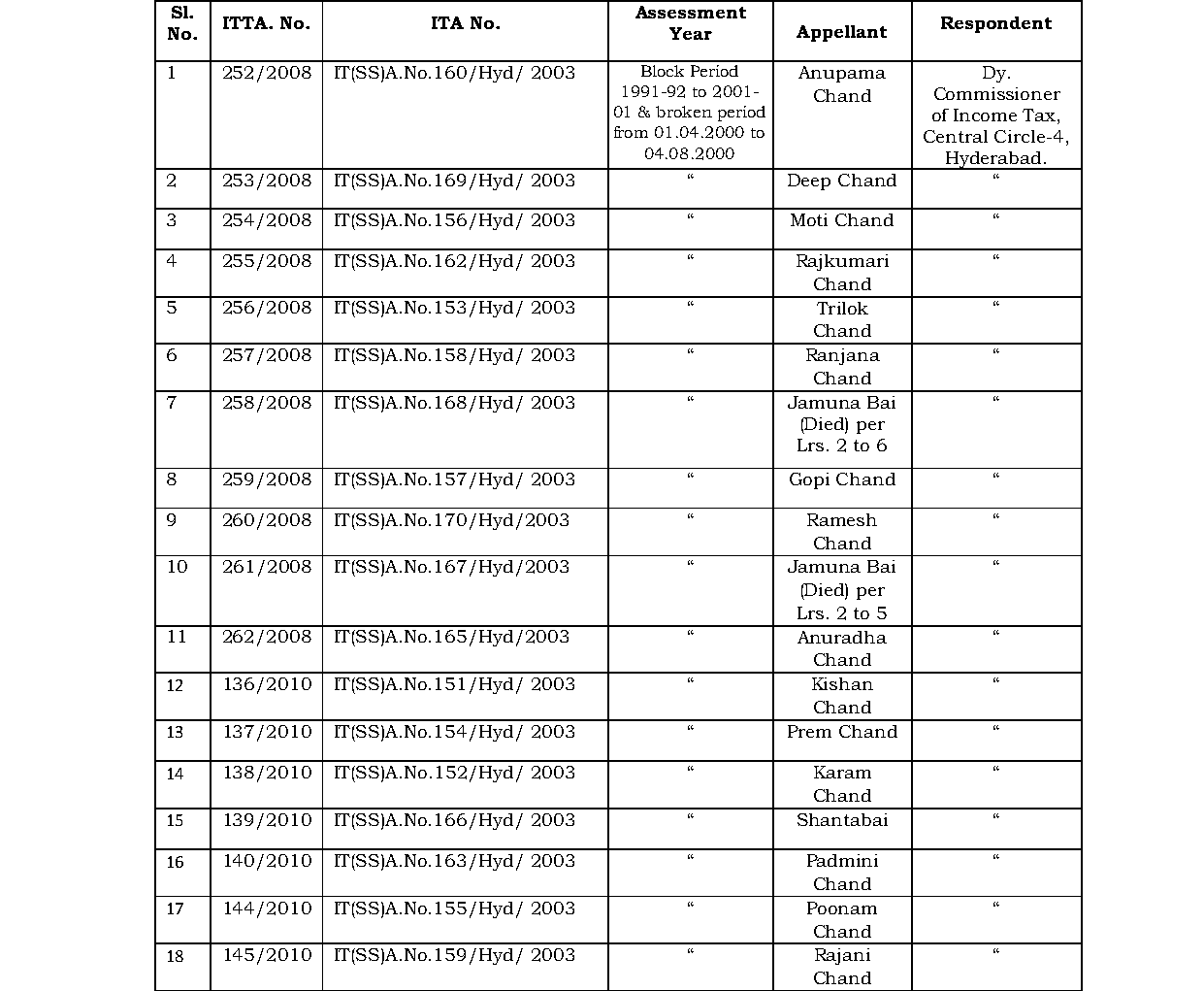

1. The present batch of (18) appeals is filed against the common order dt.15.02.2008 passed by the Income Tax Appellate Tribunal (hereinafter referred to as “the ITAT”) in respective appeals.

2. The details of the eighteen (18) appeals, the orders impugned, the assessment years involved, names of the appellants and the respondents, for convenience, are reproduced hereunder:

3. As all these eighteen appeals are similar in nature, arising out of identical factual circumstances and involving common questions of law emanating from eighteen separate assessment orders, which were carried in appeal before the Commissi

Actual service of notice under Section 143(2) must occur within the statutory timeframe; mere issuance is insufficient for legal compliance, thus invalidating assessment proceedings.

Authorised officer may, during the course of the search or seizure or within a period of sixty days from the date on which the last of the authorisations for search was executed, make a reference to ....

Failure to issue notice u/s 143(2) after valid return (filed within COVID extensions) in reassessment proceedings renders assessment invalid and a nullity, as it is a mandatory jurisdictional require....

Issuance of notice u/s.143(2) is mandatory and sine qua non for valid reassessment u/s.143(3) r.w.s.147; its absence renders assessment void ab initio.

Failure to issue notice under Section 143(2) invalidates the assessment order, as it is a mandatory procedure under the Income Tax Act.

The court held that in cases of search under Section 132, the provisions of Section 153A apply mandatorily, overriding Section 147 and 148, unless incriminating material is found.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :