IN THE HIGH COURT OF KARNATAKA DHARWAD BENCH

M. Nagaprasanna, J.

M/S. Shree Renuka Sugars Limited - Petitioner

Versus

The Assistant Commissioner Of Income Tax – Respondent

Writ Petition No.101678 OF 2024 (T – IT)

Decided On : 15-12-2025

| Table of Content |

|---|

| 1. details of the refund process and delays. (Para 1 , 2) |

| 2. petitioner's claim for interest on delayed refund. (Para 4) |

| 3. respondent's argument against interest claim. (Para 5) |

| 4. court's analysis on interest entitlement. (Para 6 , 8 , 9) |

| 5. precedents supporting petitioner's claim for interest. (Para 10 , 11) |

| 6. court's final order granting interest. (Para 12) |

ORDER :

M.NAGAPRASANNA, J.

The petitioner is before this Court seeking the following prayer:

“A) Issue an appropriate writ or order in the nature of Mandamus or otherwise, directing the Respondents to grant interest on delayed refund of Rs. 2,60,92,283/-at the rate of 6% from 25.05.2021 (being 90 days from 24.02.2021, i.e. date of issue of Form 5 by the designated authority) up to 10.01.2024 [being date of payment of refund] or alternatively at the rate of 6% for the period of delay from 31.07.2021 [i.e. the due date for passing of consequential order to Form 5 as per the Central Action Plan for FY 2021-22 formulated by the CBDT] to 10.01.2024 [being date of payment of refund];

(B) Issue an appropriate writ or order in the nature of Mandamus or otherwise, directing the Respondents to grant further interest on such interest as prayed in (A) above, from 10.01.2024 [being date of payment of refund without interest] upto the date of actual payment of interest;

(C) Grant such other relief’s as this honourable High Court may think fit including the costs of this writ petition.”

2. Facts in brief, germane, are as follows:

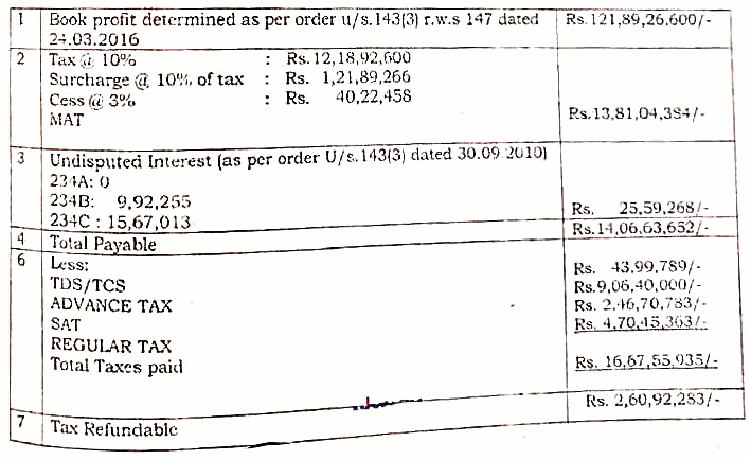

2.1. The petitioner is a Company incorporated under the provisions of the Companies Act, 1956 and is engaged in the business of manufacturing, trading and supply of sugar and its allied products. It transpires that the Assistant Commissioner of Income Tax, Circle-2(1), Belagavi, passes an order of assessment under Section 143 (3) read with Section 147 of the Income Tax Act, 1961 (hereinafter referred to as the ‘Act’ for short) for the assessment year 2008-2009, determining the tax payable at Rs.4,36,47,080/- as obtaining on 24-03-2016. The petitioner, aggrieved by the said determination, files an appeal before the Commissioner of Income Tax (Appeals) on 27-04-2016. The petitioner then files a declaration in Form No.1 and undertaking in Form No.2, in accordance with the provisions of the Direct Tax Vivad Se Vishwas Act, 2020 (hereinafter referred to as the ‘Act, 2020’ for short) for the impugned assessment year 2008-2009 on 11-07-2020.

2.2. The Principal Commissioner of Income Tax is said to have issued a certificate under Section 5 (1) of the Act, 2020 in Form No.3 determining the amount refundable to the petitioner in terms of the scheme at Rs.2,60,092,283/- for the said assessment year 2008-2009 and the determination is made on 19-01-2021. The petitioner then files an intimation of payment under (2) of the Act, 2020 in Form No.4 for the assessment year 2008-2009. It transpires that the order is passed declaring full and final settlement of tax arrears under (2) r/w Section 6 of the said Act, 2020. Giving effect to the order so passed on 24-02-2021 of full and final settlement and determining the tax refundable of Rs.2,60,92,283/-, a communication comes to be issued to the petitioner on 11-04-2022.

2.3. An intimation letter is further issued on 08-07-2022 proposing to adjust the refund due of the aforesaid amount against the demand for the assessment year 2018-2019 raised under Section 270A of the Act. The petitioner then is said to have communicated on 11-07-2022 objecting to the proposed adjustment of refund against the demand for the assessment year 2018-2019 arising under Section 270A, on the ground that the demand for assessment year 2018-2019 had been stayed by this Court in a writ petition filed by the present petitioner and an interim order to that effect was operating as granted on 29-06-2022. The petitioner then communicates to the 1st respondent on 05-09-2022 seeking issue of refund of Rs.2,60,92,283/- as was determined. An intimation wa

In tax matters, entitlement to interest on delayed refunds, including on interest accrued, is affirmed, highlighting the principle that overdue amounts accrue additional interest.

The court held that the Revenue is accountable for delayed refunds and must pay interest despite the exclusion in the Direct Tax Vivad se Vishwas Act, 2020.

The court ruled that interest on delayed refund is due despite provisions of the VSV Act denying such interest, emphasizing accountability for wrongful retention of funds.

Petitioner entitled to interest on delayed refund from the date of entitlement, despite provisions of VSV Act prohibiting interest prior to refund determination.

The main legal point established in the judgment is that the petitioner is entitled to interest as calculated by the petitioner and confirmed by the respondent, and is also entitled to interest durin....

The main legal point established in the judgment is that interest on delayed refunds is a statutory liability under Section 11BB of the Central Excise Act, 1944, and becomes payable if the duty order....

The interest would be payable in terms of the provisions of the statute and any delay in paying the compensation or the amounts due would attract award of interest at a reasonable rate on equitable g....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :