IN THE HIGH COURT OF KARNATAKA AT BENGALURU

S.R. KRISHNA KUMAR, J.

M/s. Dodla Dairy Limited – Petitioner

Versus

The Union Of India – Respondent

WRIT PETITION NO. 21566 OF 2025 (T-RES)

Decided On : 11-12-2025

| Table of Content |

|---|

| 1. relief sought by petitioner in writ petition. (Para 1 , 2) |

| 2. adjudication process against petitioner initiated. (Para 3 , 4 , 5) |

| 3. classification of flavoured milk analyzed. (Para 6) |

ORDER :

S.R.KRISHNA KUMAR, J.

In this petition petitioner seeks the following reliefs:

(a) Issue a writ of Certiorari, or such other Writ, Order or direction in the nature of a writ of certiorari, quashing the order of Respondent No.2 in Order in Appeal No. MYS-SPP-ADC/JC(A)-037-2022-23-GST dt.25.7.22 (Annexure P), as being arbitrary, illegal, against judicial discipline, as being opposed to orders of Honourable Supreme Court and Honourable High Courts;

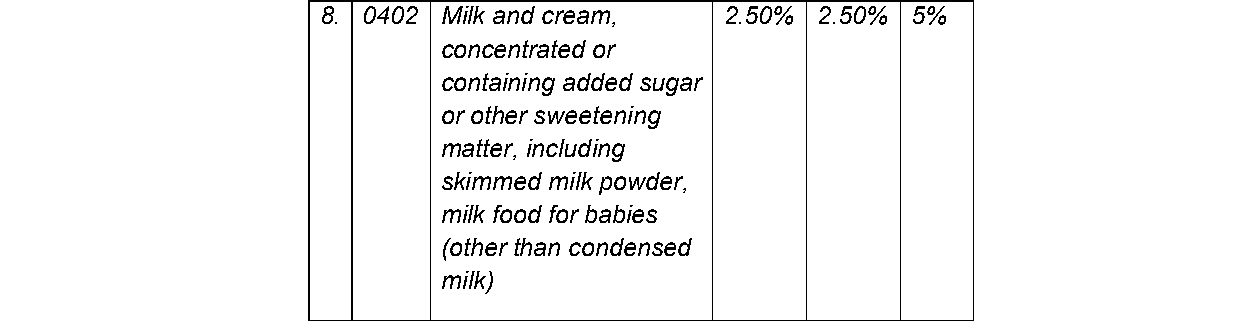

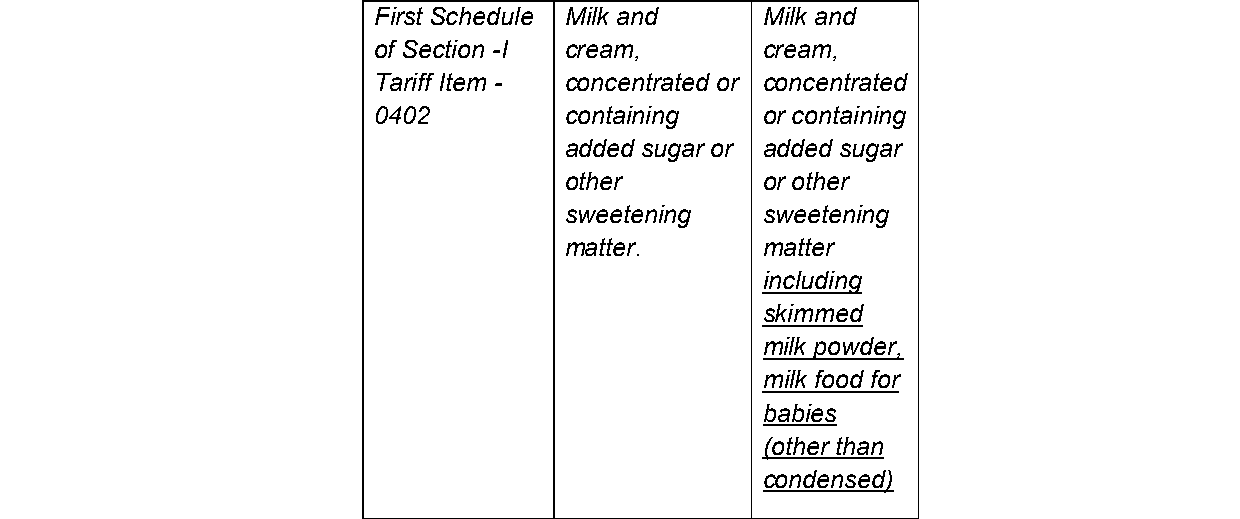

(b) Issue a writ of Mandamus to declare that flavoured milk merits classification under GST Tariff Heading 0402 and accordingly be subject to GST @ 5% (2.5% CGST and 2.5% SGST)

(c) Issue a writ of Mandamus or such other Writ, Order or direction, as this Honourable Court may deem fit, consequently, directing Respondent No.3 to refund Rs.72,95,235/-, paid by the Petitioner vide DRC 03 Challans dt.21.12.21 (Annexure M1, M2 and M3), against illegal demand made by Respondent No.3 and confirmed by Respondent No.2;

(d) To pass such other orders, directions and writs as this Honourable High Court may deem fit in the facts and circumstances of the case, and in the interests of justice, including the costs of this writ petition.

For which Act of kindness, the petitioner shall as in duty bound, ever pray."

2. Heard learned counsel for the petitioner, learned counsel for the respondents No.1 to 4 and learned HCGP for respondent No.5 and perused the material on record.

3. A perusal of the material on record will indicate that pursuant to proceedings conducted by the respondents, show cause notice dated 17.09.2020 was issued by respondent No.4 to the petitioner under Section 74 of the CGST Act to which, the petitioner submitted a reply dated 17.10.2020 and the same having been culminated in the adjudication order dated 22.09.2021. Subsequently, the petitioner deposited the GST amount of Rs.72,95,235/- on 21.12.2021 under protest and filed an appeal, which was also dismissed by the first appellate Authority. Aggrieved by the impugned adjudication orders of the adjudicating Authority and the first appellate Authority, petitioner is before this Court by way of the present petition.

4. Per contra, learned counsel for the respondents submits that there is no merit in the petition and the same is liable to be dismissed.

5. A perusal of the material on record would indicate that in the petitioner's own case, i.e. in Writ Petition No.5699/2025, the Division Bench of the Andhra Pradesh High Court ruled in favour of the petitioner vide 'Annexures - Q1, Q2 and Q3' dated 19.03.2025 as hereunder.

“Annexure-Q1:

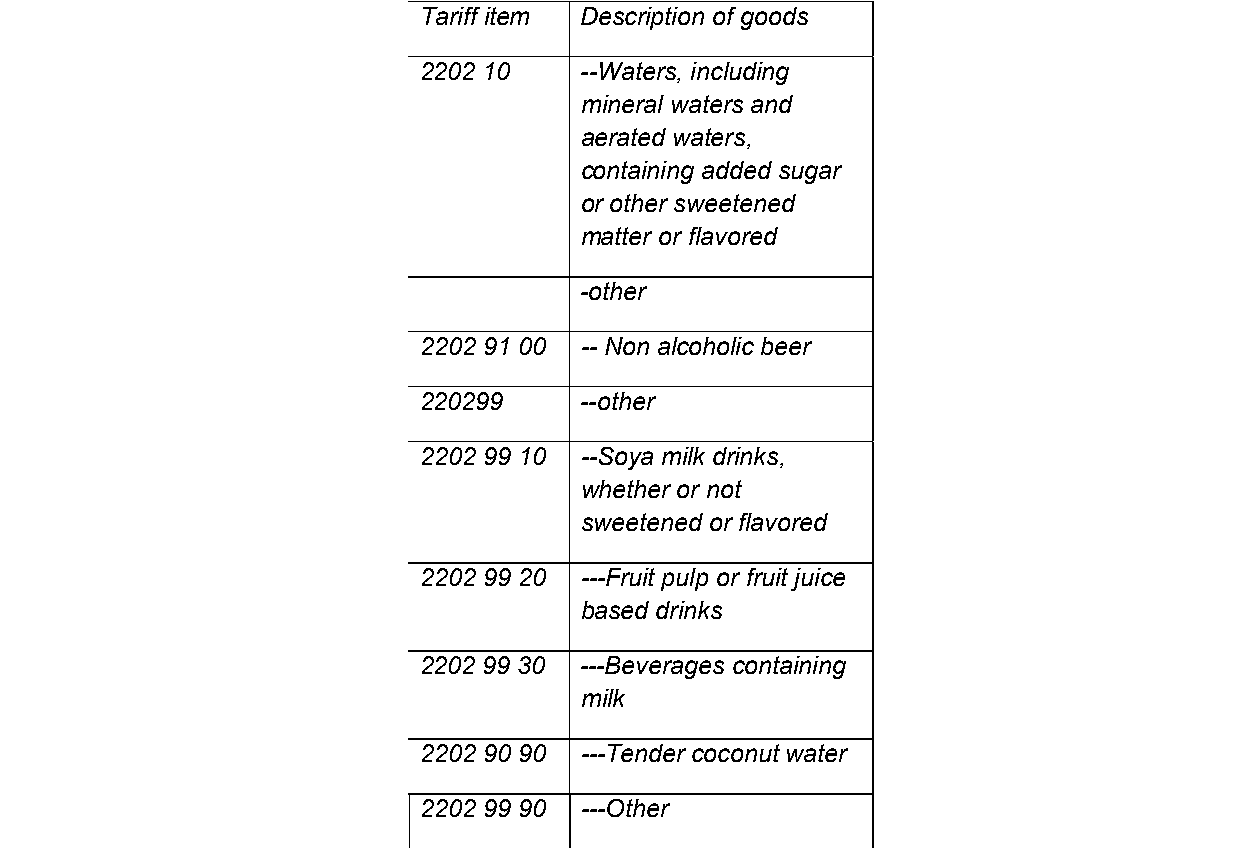

The petitioner is a registered dealer, under the GST Act, dealing with milk and milk products. The assessment of the petitioner, for the period 2017-18, was completed and an assessment order has been passed by the 2nd respondent, on 09.03.2021. The petitioner was aggrieved by two components of the assessment order. The Assessing Officer had held that the flavoured milk sold by the petitioner would fall within the tariff heading CH 2202 instead of 0402. The Assessing Officer had also held that the conversion of milk into milk powder and the charges collected on such conversion was chargeable at the rate of 18%.

2. The petitioner being aggrieved by the two components of the assessment order had filed an appeal before the 1st respondent which came to be dismissed on 16.12.2024.

3. Aggrieved by these two orders, the petitioner has approached Court, by way of the present Writ Petition on the ground that the second appeal, which would normally be filed before the Tribunal, could not be filed as the GST Tribunal has not come into existence.

4. The learned counsel for the petitioner would now rely upon the Judgment of a Division Bench of this Court, dated 10.12.2024, in W.P.No.254 of 2024 wherein this Court had held that f

Flavoured milk is classified under GST Tariff Heading 0402, not 2202, confirming lower tax rates and quashing previous higher tax assessment.

The classification of carbonated fruit drinks under Tariff Item 2202 99 20 is upheld, affirming that products with significant fruit juice content cannot be classified merely as aerated waters.

The classification of beverages under VAT must align with common understanding; 'Sharbat Rooh Afza' qualifies as a fruit drink under Entry 103 based on its essential character.

The main legal point established in the judgment is the requirement for reasonable classification in taxation laws, as mandated by Article 14 of the Constitution of India. The court emphasized the ne....

Point of Law : Question of manufacture is not relevant for the purposes of the 2003 Act.

The court established that the classification of tobacco products relies on the presence of manufacturing activity; absence of such activity necessitates classification as unmanufactured tobacco unde....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :