IN THE HIGH COURT OF KARNATAKA AT BENGALURU

S.R.KRISHNA KUMAR, J.

Mangalore Steamer Agents Association, Through Its Authorized Signatory, Mr. Praveen Kumar Bangera – Appellant

Versus

Union Of India, Through The Secretary – Respondent

Writ Petition No. 32835 Of 2017 (T-RES)

Decided On : 28-11-2025

ORDER :

S. R. KRISHNA KUMAR, J.

1. In this petition, petitioner seeks the following reliefs:

" a. Issue any writ, order or direction more particularly in the nature of a Writ of Declaration to declare Section 66C (2) of Chapter V of the Finance Act, 1994 (as amended) as null, void and ultra vires Article 14, 19, 246, 248, 265, 268A and 302 read with Entry 41 and 83 of List I of VII Schedule of the Constitution of India and as also being beyond the legislative competence of Parliament under Articles 246 and 248 of the Constitution of India and pass such further or other orders as this Hon'ble Court may deem fit and necessary in the facts and circumstance of the case and thus render justice;

b. Issue any writ, order or direction more particularly in the nature of a Writ of Declaration to declare Rule 10 of Notification No. 28 of 2012-ST dated 20.06.2012, (The Place of Provisions of Service Rules, 2012), as null, void and ultra vires Article 14, 19, 246, 248, 265, 268A and 302 read with Entry 41 and 83 of List 1 of VII Schedule of the Constitution of India and as also being beyond the legislative competence of Parliament under Articles 246 and 248 of the Constitution of India and pass such further or other orders as this Hon'ble Court may deem fit and necessary in the facts and circumstance of the case and thus render justice.

c. Issue any writ, order or direction more particularly in the nature of a Writ of Declaration to declare Notification No. 1 of 2017 dated 12.01.2017 vide F. No. 354/42/2016-TRU issued by the 1" Respondent, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-Section (1), as per Annexure - A, as ultra vires Article 14, 19, 265, 268A and 302 read with Entry 41 and 83 of List 1 of VII Schedule of the Constitution of India and pass such further or other orders as this Hon'ble Court may deem fit and necessary in the facts and circumstance of the case and thus render justice;

d. Issue any writ, order or direction more particularly in the nature of a Writ of Declaration to declare Notification No. 2 of 2017 dated 12.01.2017 vide F No. 354/42/2016-TRU issued by the 1 Respondent, published in the Gazette of India, Extraordinary, Part II, Section 3. Sub-Section (i), as per Annexure - A as ultra vires Article 14, 19, 265, 268A and 302 read with Entry 41 and 83 of List 1 of VII Schedule of the Constitution of India and contrary to Section 14 of the Customs Act, 1962 read with the provisions of Rule 10(2) of the Customs Valuation (Determination of Price of Imported Goods) Rules, 2007 and pass such further or other orders as this Hon'ble Court may deem fit and necessary in the facts and circumstance of the case and thus render justice;

e Issue any writ, order or direction more particularly in the nature of a Writ of Declaration to declare Notification No. 3 of 2017 dated 12.01.2017 vide F. No. 354/42/2016-TRU issued by the 1st Respondent, published in the Gazette of India, Extraordinary, Part II, Section 3. Sub-Section (i), as per Annexure A2 as ultra Vires Article 14, 19, 265, 2684 and 302 read with Entry 41 and 83 of List I of VII Schedule of the Constitution of India and contrary to Section 14 of the Customs Act. 1962 read with the provisions of Rule 10(2) of the Customs Valuation (Determination of Price of Imported Goods) Rules, 2007 and pass such further or other orders as this Hon'ble Court may deem fit and necessary in the facts and circumstance of the case and thus render justice;

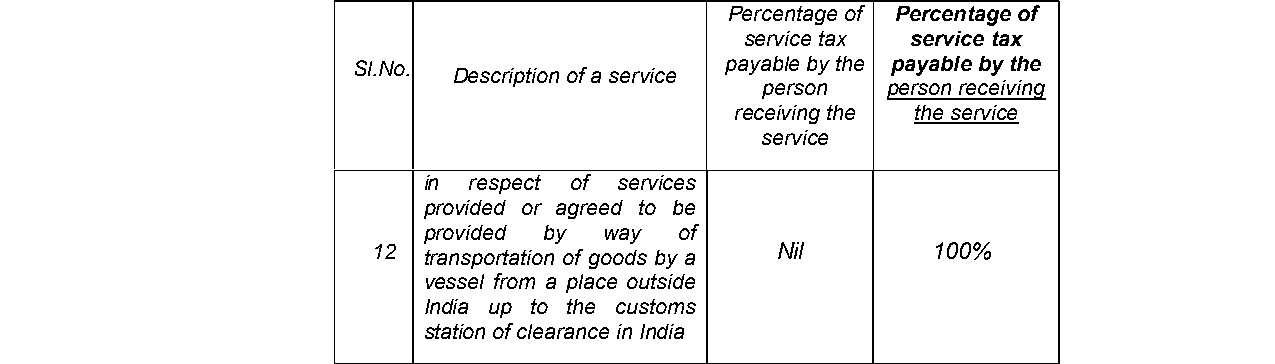

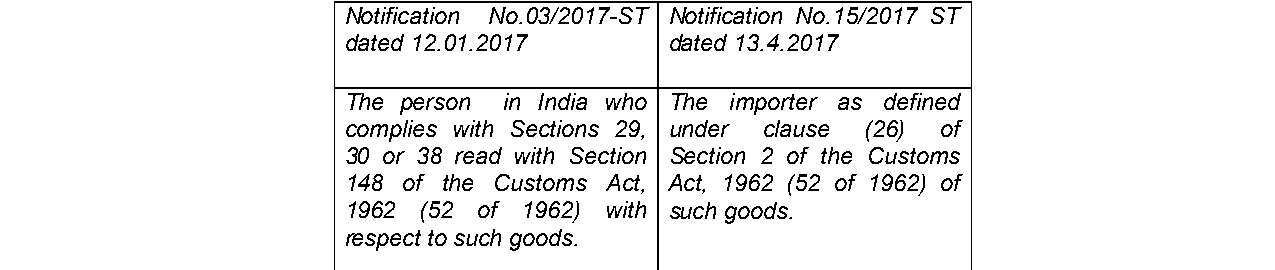

f. Issue any writ, order or direction more particularly in the nature of a Writ of Declaration to declare Notification No. 15/2017-Service Tax dated 13.04.2017 issued by the 1st Respondent, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-Section (i), as per Annexure A3, as applicable on and from 22nd January, 2017 and pass such further or other orders as this Hon'ble Court may deem fit and necessary in the facts and circumstance of the case and thus render justice;

g. Issue a Writ of Certiorari or

Steamer agents and importers cannot be held liable for service tax under challenged notifications as they are not the recipients of service, establishing the necessity for clear recipient-service pro....

The constitutionality of service tax rules imposing levies on overseas transportation services is deemed ultra vires, mandating refunds of service tax.

Service tax valuation must strictly adhere to the gross amount charged for services rendered, excluding any additional costs or expenses not directly related to the service.

The court emphasized that claimants must substantiate their exemption claims with credible documentation, and the existence of an effective alternative remedy limits the exercise of writ jurisdiction....

Court held that proper grounds for invoking extended limitation for tax demands must demonstrate intent to evade payment, and procedural fairness must be maintained in tax assessments.

Tax liability must be established based on actual statutory provisions, not presumptions; authorities cannot invoke extended limitation without finding willful non-disclosure.

SEZ Act Section 26 exemption for services to SEZ units overrides service tax levy under Finance Act; procedural non-compliance in notifications does not defeat substantive statutory exemption due to ....

The court upheld the validity of show cause notices issued under the Central Goods and Services Tax Act, affirming the authority of the officers and the necessity for the petitioner to respond to the....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :