IN THE HIGH COURT OF KARNATAKA AT BENGALURU

S.R.KRISHNA KUMAR, J.

Sri. Sachin Narayan, S/o. Sri. H. G. Narayan – Appellant

Versus

The Assistant Commissioner Of Income Tax – Respondent

Writ Petition No. 52423 Of 2019 (T-IT)

Decided On : 13-11-2025

ORDER :

S.R.KRISHNA KUMAR, J.

1. In this petition, petitioner seeks quashing of the impugned Notices issued by the respondent to the petitioner for the assessment years 2012-13, 2013-14, 2014-15, 2015-16, 2016-17 and 2017-18 under Section 153C of the Income Act, 1961 (for short ‘the I.T. Act’) and for other reliefs.

2. Heard learned counsel for the petitioner and learned counsel for the respondents – Revenue and perused the material on record.

3. A perusal of the material on record will indicate that, the respondents obtained a warrant of authorization dated 01.08.2017 under Section 132 of the I.T. Act and Rule 112 of the I.T. Rules in relation to one Sri D.K.ShivaKumar and in respect of residential premises of the petitioner at No. 902, 9th ‘A’ Cross, 6th Main, 2nd Stage, West of Chord Road, Rajaji Nagar, Bangalore. In pursuance of the same, the respondents conducted search in the aforesaid premises of the petitioner during the period from 02.08.2017 to 05.08.2017 and recorded the statement of the petitioner, pursuant to which, the 1st respondent prepared a satisfaction note recording reasons for initiating action against the petitioner under Section 153C of the I.T. Act, in pursuance of which, the 1st respondent issued the impugned notice under Section 153C of the I.T. Act to the petitioner. Subsequently, the 1st respondent issued Section 142 (1) as well as Section 143 (2) notices for the aforesaid assessment years. Subsequently, on 18.11.2019, the petitioner filed his objections to the aforesaid notices under Section 153C of the I.T. Act issued by the respondents. Thereafter, the 2nd respondent passed an order dated 28.11.2019 disposing of the petitioner’s objections to the notice under Section 153C of the I.T. Act. Aggrieved by the aforesaid notices and order, the petitioner is before this Court by way of the present petition.

4. In addition to reiterating the various contentions urged in the petition and referring to the material on record, learned counsel for the petitioner submits the issue in controversy is directly and squarely covered by a judgment of this court in the case of C.R. Ram Mohan Raju vs. The Deputy Commissioner of Income Tax in W.P. No.33057 of 2024 dated 27.10.2025.

5. Per contra, learned counsel for the respondents – revenue would reiterate the various contentions urged in the statement of objections and submit that the search warrant was issued to search one Sri. D.K.Shivakumar, who was the searched person and merely because search was conducted in the premises of the petitioner, he cannot be construed or treated as a searched person but had to be considered as a non-searched person / such other person as contemplated under Section 153C of the I.T. Act. and as such, there is no merit in the petition and the same is liable to be dismissed.

6. I have given my anxious consideration to the rival submissions and perused the material on record. The counsel for the petitioner is right in contending that the issue in controversy is directly and squarely covered by a judgment of this Court in the case of C.R. Ram Mohan Raju’ s case supra, which reads as under:

“7. Before adverting to the rival submissions, it would be apposite to extract the satisfaction note prepared by the 1st respondent for initiating action against the petitioner under Section 153C of the I.T.Act, which is as under:-

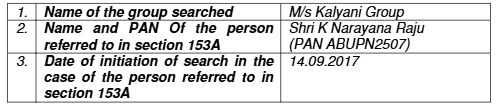

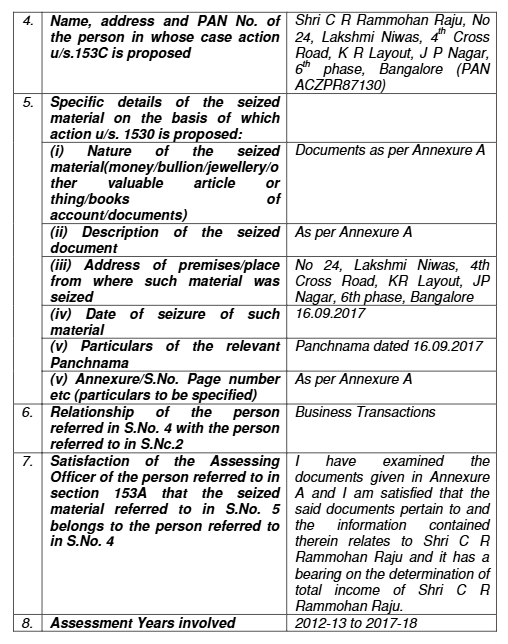

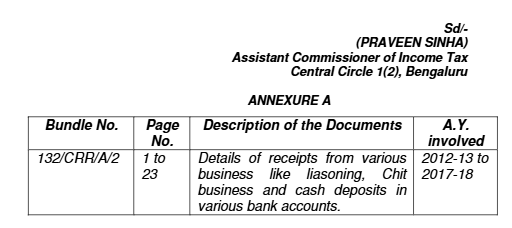

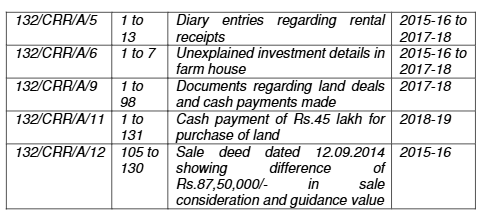

“Reasons for initiating action u/s. 153C of Income Tax Act, 1961 in the case of Shri CR Rammohan Raju

Search & seizure action u/s 132 of the Income Tax Act, 1961 was carried out in the case of Shri K Narayan Raju on 14.09.2017. The residence of Shri C R Rammohan Raju at No 24, Lakshmi Niwas, 4th Cross Road, KR Layout, J Nagar, 6th phase, Bangalore was also searched in this regard and various documents as per Panchanama dated 16.09.2017 were seized and statement u/s 132(4) of IT Act of Shri C R Rammohan Raju was recorded on 14.09.2017. In the statement, he was confronted with the documents seized during the course of the search. Furth

For invoking Section 153C, the petitioner must not be treated as a non-searched person; proper jurisdiction requires a satisfaction note linking seized documents to undisclosed income of another part....

A person may only be assessed under Section 153C of the Income Tax Act if they are not the 'searched person'; procedural safeguards must precede assessment actions.

The court held that a petitioner searched under Section 132 of the Income Tax Act cannot be treated as a non-searched person for proceedings under Section 153C, and thus impugned notices issued again....

The court ruled that assessment orders under Section 153C of the Income Tax Act are void if the petitioner was a searched person and no incriminating evidence was found linking them to potential undi....

The court held that in cases of search under Section 132, the provisions of Section 153A apply mandatorily, overriding Section 147 and 148, unless incriminating material is found.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :